Tech Keeps Driving Equity Rally as Broader Market Lags

Financial markets remain in a risk-on regime, driven primarily by the technology sector in what is becoming an anomaly worth monitoring closely (only three sectors within the S&P 500 have a Health Score above 50, while the overall average remains below the neutral threshold). It remains to be seen whether developments in the increasingly complex situation in the Gulf and the U.S. labor market report (due tomorrow) will broaden or narrow the scope of this equity rally.

Meanwhile, the recovery in fixed income markets has paused and the U.S. dollar remains strong, both signals that inflation expectations continue to play a significant role in investors’ decision-making. Futures point to a negative opening in Europe and a slightly weaker start for U.S. markets.

Market Weather Map

June 4, 2026

US Equities

Eu Equities

Asia Equities

Commodities

Bonds

Dollar Index

Technology

Gold

Oil

Crypto

Market Summary

Do you want to see the score details for all assets monitored by KBMeter?

Try free for 14 days →Financial markets sentiment

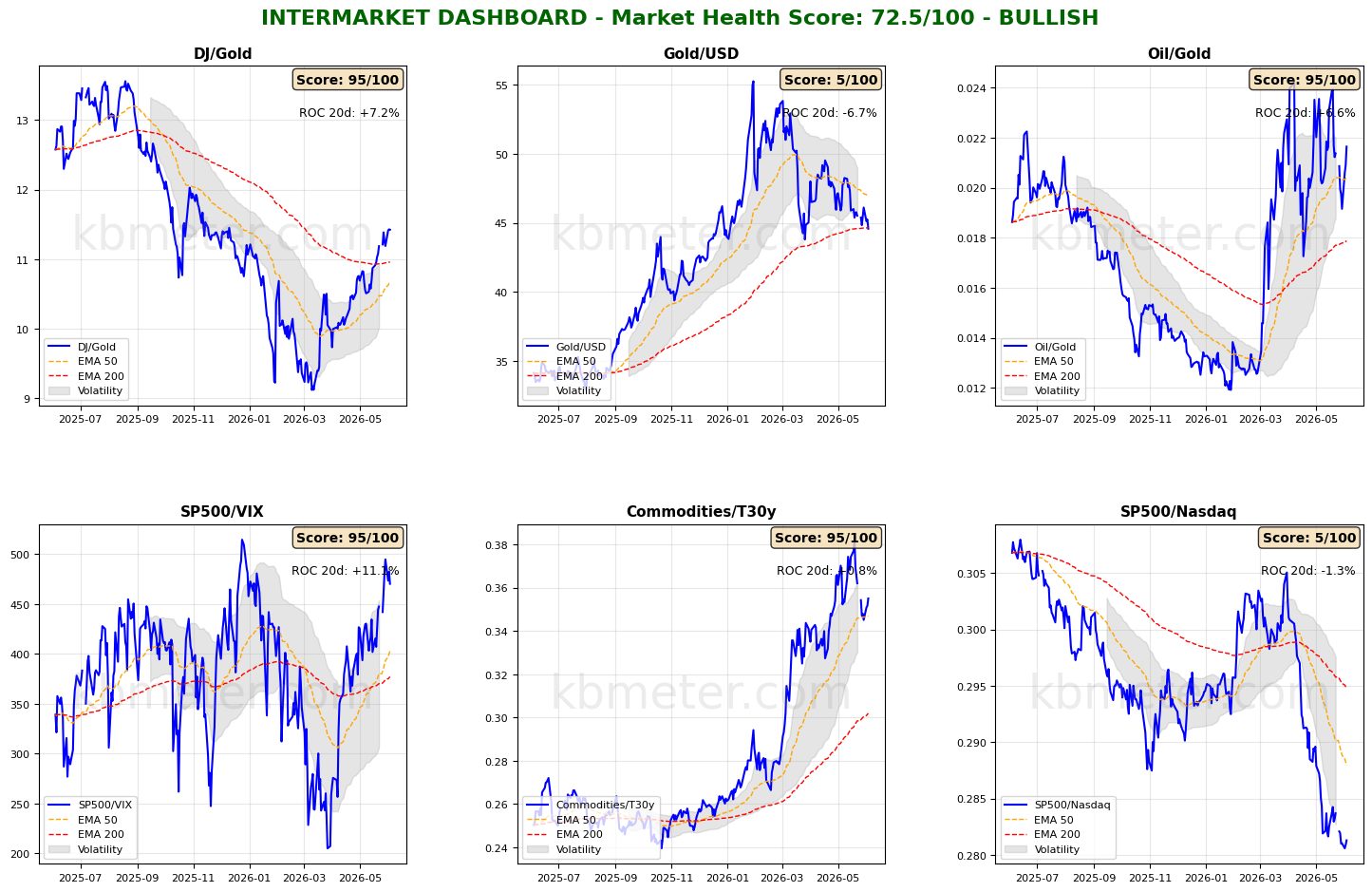

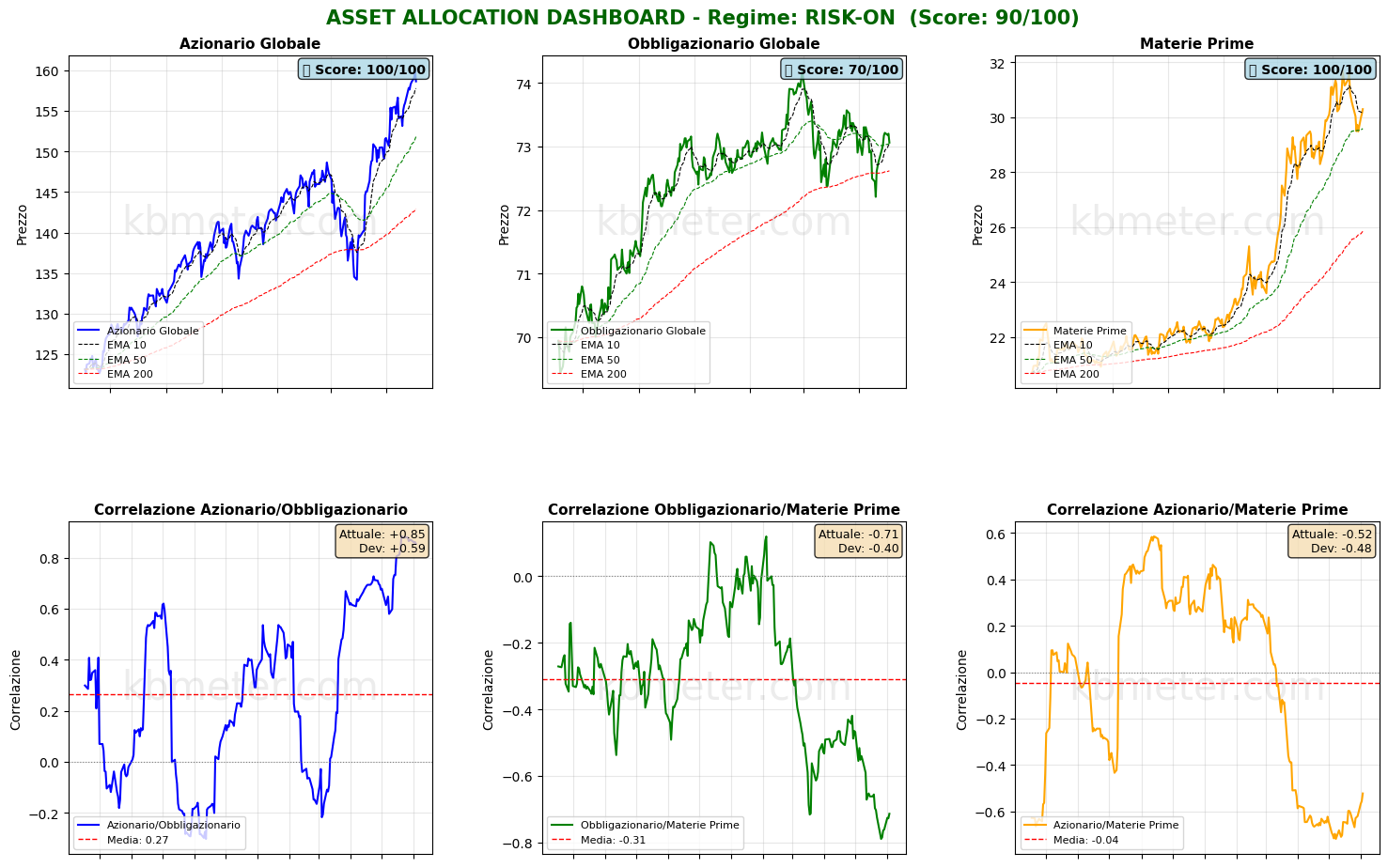

Financial markets are displaying a moderately positive sentiment today. Intermarket analysis shows a Market Health Score of 72/100, indicating a positive environment. Our intermarket dashboards continue to signal a risk-on backdrop, although risk appetite indicators have stabilized in recent sessions at the period lows reached last week.

The support provided by the 50-day moving average has halted the decline in the Commodities/Bonds ratio, highlighting persistent inflationary pressures. At the same time, the Dollar/Gold ratio remains anchored to its long-term moving average, a critical support level for the indicator.

Across asset classes, there are no major new developments. Uncertainty surrounding the situation in the Gulf is dampening the upward momentum in both global equities and bonds, while the first attempt by commodities to break below their medium-term moving average has been rejected following a brief surge in energy prices.

Our market weather map continues to assign scores above 60 points to both the U.S. dollar and the technology sector. The latter is the focus of our latest observation. The average Health Score across S&P 500 sectors currently stands at 47.4 points, with only three sectors above the 50-point threshold: Technology, Materials, and Industrials. In other words, market strength is far from broad-based. This is a situation that warrants close monitoring when assessing the medium-term sustainability of the current equity rally.

Global Futures – Pre-Market Sentiment

Global futures indicate a moderately risk-off sentiment, with an average decline of 0.32%. U.S. futures are slightly negative (-0.15%), European futures are down 0.37%, and Asian futures are lower by 0.42%.

📊 Global Futures – Pre-Market Sentiment

- CSI 300: +0.41%

- CAC 40 derived: +0.21%

- Russell 2000: +0.15%

- TecDAX derived: -1.26%

- FTSE MIB derived: -1.07%

- Nikkei 225 derived: -1.04%

Macroeconomic calendar

Today’s macroeconomic agenda includes the release of:

- Spain’s April 2026 Industrial Production data;

- Euro Area April 2026 Retail Sales figures.

From the United States, several key labor market indicators will be released, providing further insight into employment conditions:

- May Challenger Job Cuts;

- Weekly Initial Jobless Claims;

- First-quarter 2026 Productivity data;

- First-quarter 2026 Unit Labor Costs.

These releases will help investors assess the current health and resilience of the U.S. labor market.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 4 June 2026 - 7:51 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.