Markets Turn Neutral as Tech Rally Pauses Ahead of ECB Decision and U.S. Inflation Data

An important week is beginning from a macroeconomic perspective for financial markets. Market sentiment—having shifted from risk-on to neutral—emerges somewhat bruised after a Friday session that saw the technology sector pause its rally and U.S. labor market data revive expectations of potential Federal Reserve rate hikes.

U.S. inflation figures for May and the European Central Bank’s policy decisions will be the main market movers this week. Investors will also continue to closely monitor developments in the Middle East, where geopolitical tensions have risen again. Futures indicate a negative opening for European markets and a slightly negative start for U.S. equities.

Market Weather Map

June 8, 2026

US Equities

Eu Equities

Asia Equities

Commodities

Bonds

Dollar Index

Technology

Gold

Oil

Crypto

Market Summary

Do you want to see the score details for all assets monitored by KBMeter?

Try free for 14 days →Financial markets sentiment

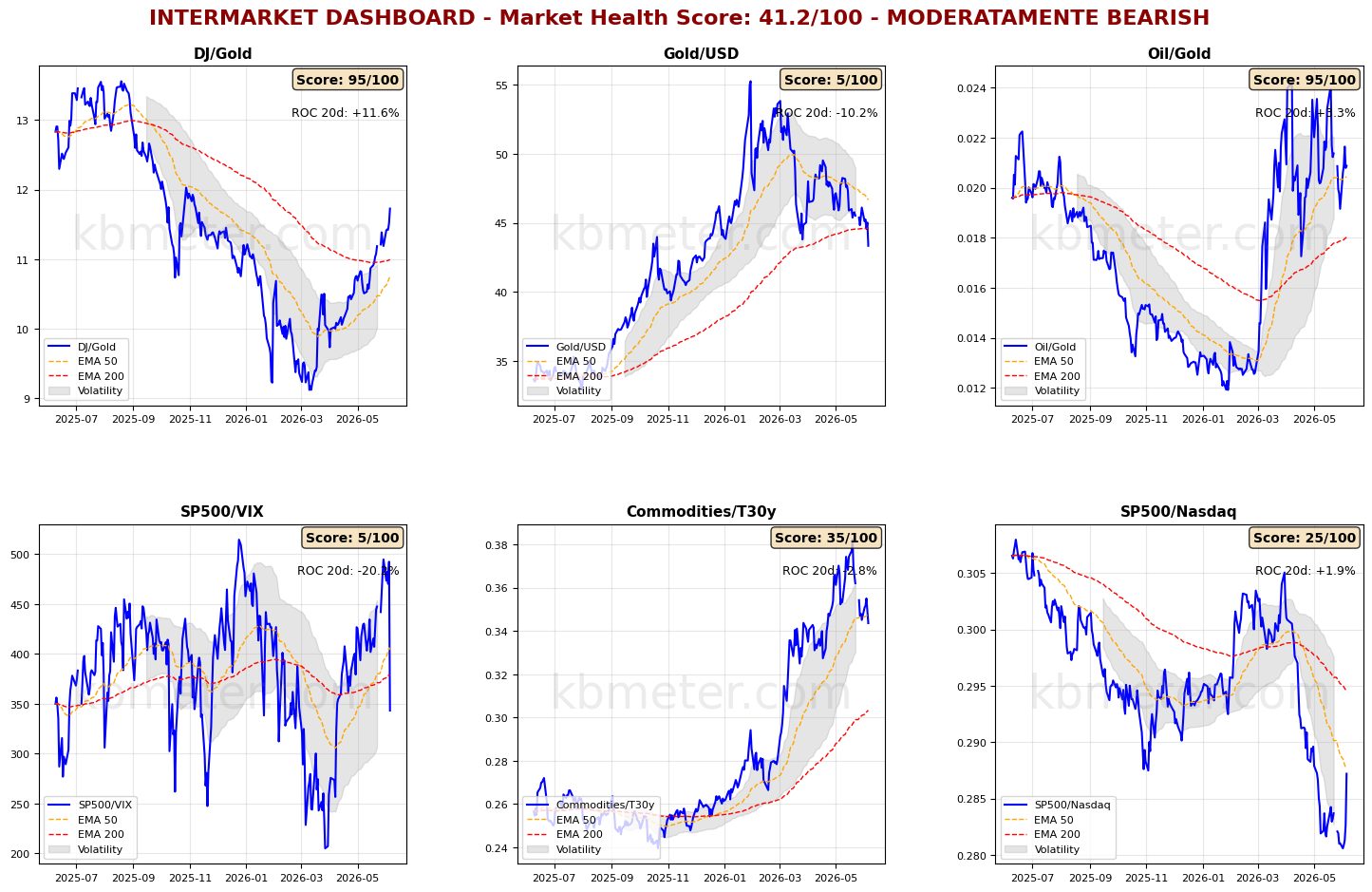

Financial markets currently reflect a neutral sentiment. Intermarket analysis shows a Market Health Score of 41/100, indicating a moderately negative environment. Our intermarket dashboards clearly highlight the impact of Friday’s session, with the technology sector losing momentum and the S&P 500/VIX ratio falling back below its long-term moving average in a single trading day. This sharp move has been amplified by the excessive concentration of the recent equity rally in technology stocks.

A closer look, however, reveals that the other indicators are not yet signaling a meaningful shift in market dynamics. Gold remains weak against both the U.S. dollar and the Dow Jones Industrial Average. Notably, the traditional Wall Street index, thanks to its composition, absorbed the technology-sector pullback much more effectively.

The Oil/Gold ratio remains highly volatile. In addition to gold’s weakness, uncertainty surrounding the Middle East continues to weigh on market behavior. Inflation expectations remain broadly stable around the 50-day moving average. From this level, a rebound could be expected should conditions in the Gulf deteriorate further or if U.S. inflation data come in significantly above expectations.

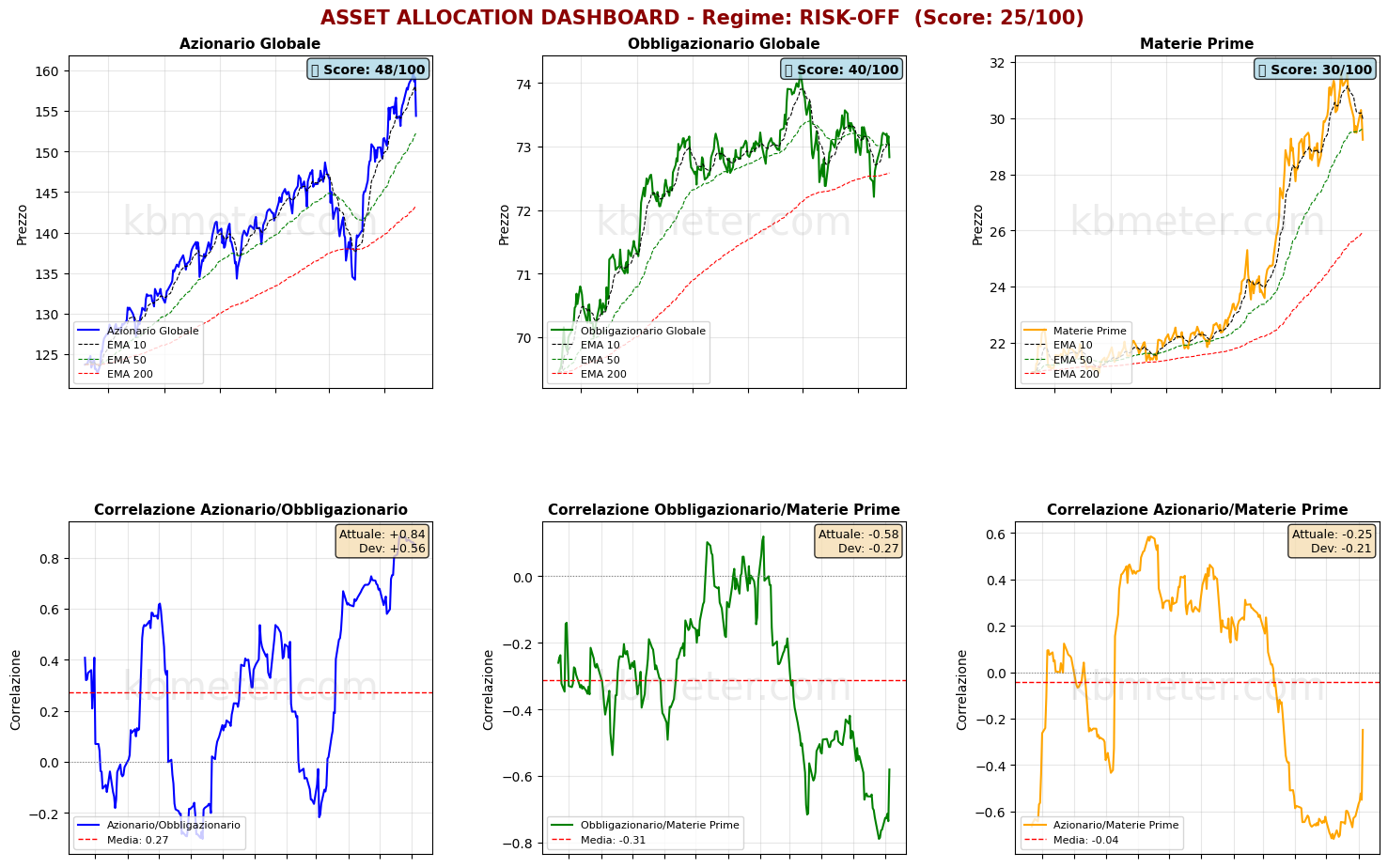

The weight of U.S. equities has dragged global equities below their short-term moving average, while global bonds have broken below their medium-term moving average support, signaling the risk of further increases in yields. Commodities are also trading slightly below their 50-day moving average.

Our market weather map shows that the U.S. dollar remains exceptionally strong, standing as the only asset class in our framework with a score above 60. Cryptocurrencies continue to occupy a critical position, while Asian equity markets are feeling the combined impact of a strong dollar, elevated interest rates, and a pause in the technology rally.

Global Futures – Pre-Market Sentiment

Pre-Market Futures. Global futures are signaling a risk-off sentiment, with an average decline of 0.62%. U.S. futures are slightly negative (-0.15%), European futures are down 0.91%, and Asian futures are lower by 0.35%.

📊 Global Futures – Pre-Market Sentiment

- Nikkei 225 derived: +0.46%

- US Tech 100 derived: +0.42%

- Russell 2000: +0.26%

- TecDAX derived: -3.09%

- CSI 300: -1.73%

- Dow Jones 30 cv1: -1.42%

Macroeconomic calendar

Today’s macroeconomic agenda includes the final reading of Japan’s first-quarter 2026 GDP growth figures. Investors will also focus on Germany’s April 2026 industrial orders data and on U.S. inflation expectations for May 2026.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 8 June 2026 - 7:35 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.