Markets Shrug Off U.S.-Iran Deal and Fed Hold; Risk-On Mood Persists as Dollar Stays Strong

Largely priced in during previous trading sessions, the news of the signing of the agreement between the United States and Iran, together with the Federal Reserve’s decision to leave interest rates unchanged (while signaling the possibility of a rate hike later this year), has had only a limited impact on financial markets. Investors continue to maintain a risk-on sentiment, although a degree of uncertainty still lingers beneath the surface of the market. This uncertainty may only be dispelled by the upcoming earnings season.

The U.S. dollar remains strong, gold has failed to stage a meaningful recovery, and risk-appetite indicators remain relatively stable. Sector rotation patterns also do not currently suggest excessive investor enthusiasm. Meanwhile, futures are pointing to a positive opening for U.S. markets and a slightly positive start for Europe.

Market Weather Map

June 18, 2026

US Equities

Eu Equities

Asia Equities

Commodities

Bonds

Dollar Index

Technology

Gold

Oil

Crypto

Market Summary

Do you want to see the score details for all assets monitored by KBMeter?

Try free for 14 days →Financial markets sentiment

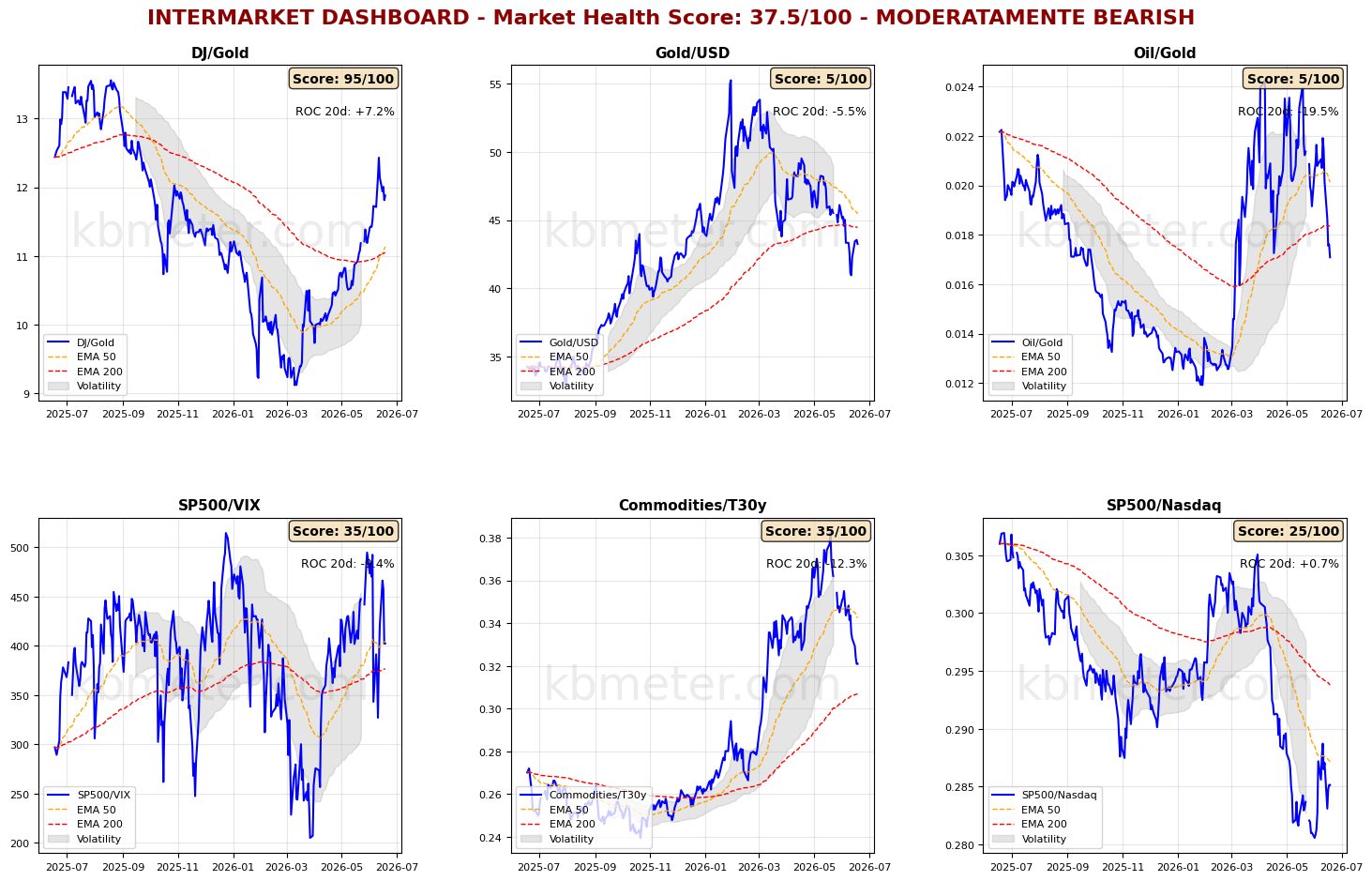

Financial markets are showing a moderately positive sentiment today. Intermarket analysis indicates a Market Health Score of 38/100, which remains moderately negative. Our intermarket dashboards show no significant changes compared with previous observations. To a large extent, both the U.S.–Iran agreement and the Fed’s decision had already been priced in by investors over recent days.

The Oil/Gold ratio is moving more decisively below its long-term moving average, with a target toward the levels seen in early March. Gold remains weak and continues to underperform both the U.S. dollar and the Dow Jones. The Gold/Dollar ratio remains below its 200-day moving average, while the Gold/Dow ratio is showing a developing bullish crossover between its 50-day and 200-day moving averages.

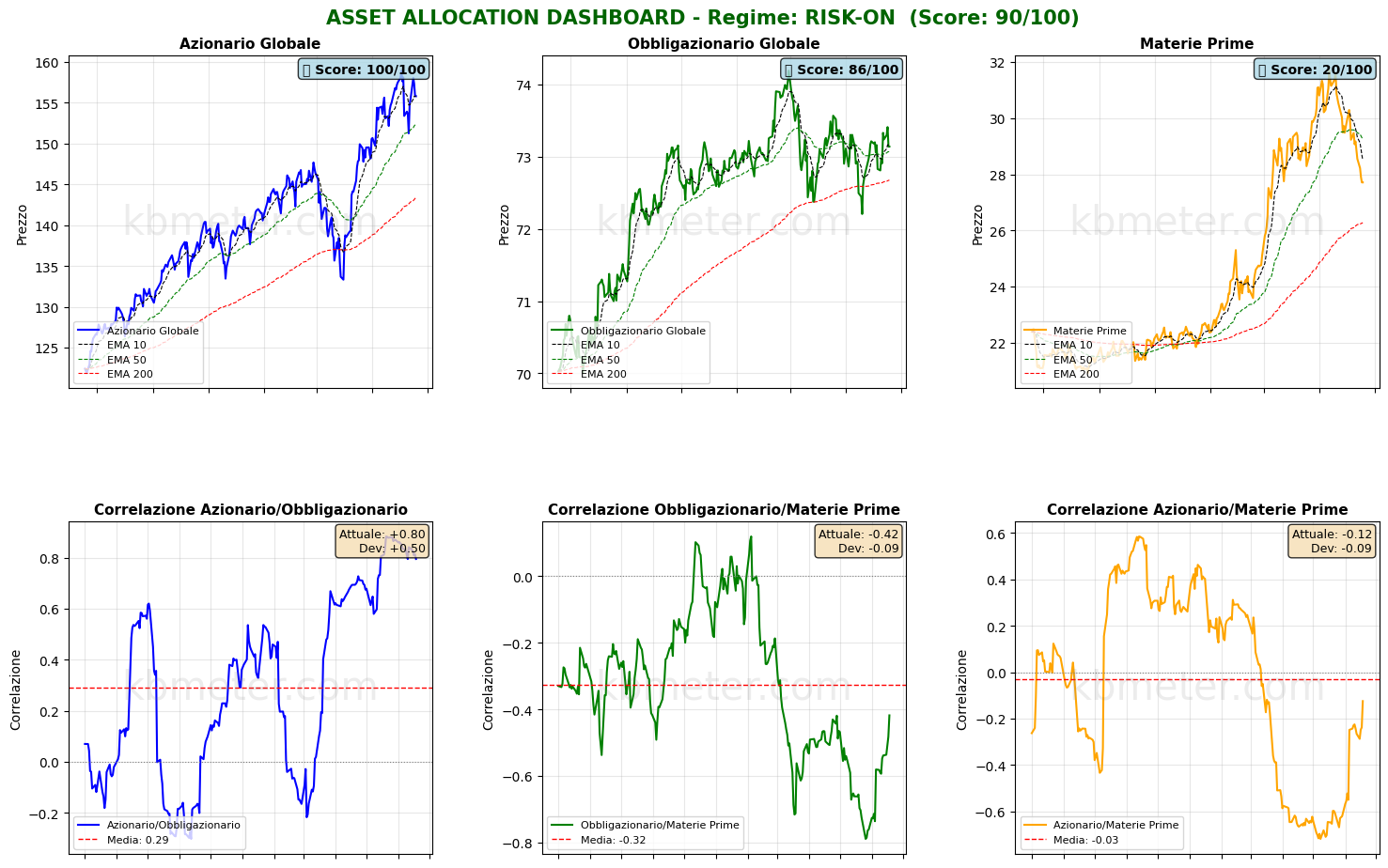

The overall asset-class picture remains largely unchanged. Commodities could accelerate to the downside on the back of the U.S.–Iran agreement, while the U.S. dollar continues to trade from a position of strength.

Our market weather map confirms readings above the 50 threshold for both equities and fixed income. Once again, the strength of the U.S. dollar stands out. Another noteworthy development is that the crypto score has now surpassed that of oil.

Global Futures – Pre-Market Sentiment

Pre-Market Futures. Global futures are signaling a moderate risk-on sentiment (+0.25% on average), with U.S. futures positive (+0.80%), Europe slightly positive (+0.03%), and Asia modestly higher (+0.18%).

📊 Global Futures – Pre-Market Sentiment

- Nikkei 225 derived: +1.74%

- IBEX 35 derived: +1.46%

- US Tech 100 derived: +1.00%

- Hang Seng derived: -1.20%

- TecDAX derived: -0.68%

- Euro Stoxx 50 derived: -0.43%

Macroeconomic calendar

Central banks remain in focus today. Monetary policy decisions are expected from the Bank of England and Bank Indonesia. No policy changes are anticipated from the former, while the latter is expected to deliver a 25-basis-point rate increase. Today’s agenda also includes UK employment data for the three months ending in April, the June Philadelphia Fed update, and the latest U.S. unemployment claims figures.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 18 June 2026 - 7:50 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.