Markets Move Beyond US-Iran Agreement, Shift Attention to Central Bank Week

Financial markets quickly digested the euphoria surrounding the recently reached agreement between the United States and Iran, as attention now shifts to a pivotal week for central banks. Interest rates, inflation, and growth forecasts have returned to the forefront of investors’ considerations, with market participants closely watching the Bank of Japan (which this morning delivered a historic rate hike to 1%), the Federal Reserve, and the Bank of England to better assess the implications of the Gulf crisis.

Equity market momentum remains positive, although our indicators continue to point to a still-weak outlook. Fixed income markets have staged a significant recovery, particularly in Europe, effectively offsetting the impact of the ECB’s recent actions. Gold is approaching critical levels that may determine its direction over the coming weeks, while oil prices are retreating and the U.S. dollar remains strong.

Market Weather Map

June 16, 2026

US Equities

Eu Equities

Asia Equities

Commodities

Bonds

Dollar Index

Technology

Gold

Oil

Crypto

Market Summary

Do you want to see the score details for all assets monitored by KBMeter?

Try free for 14 days →Financial markets sentiment

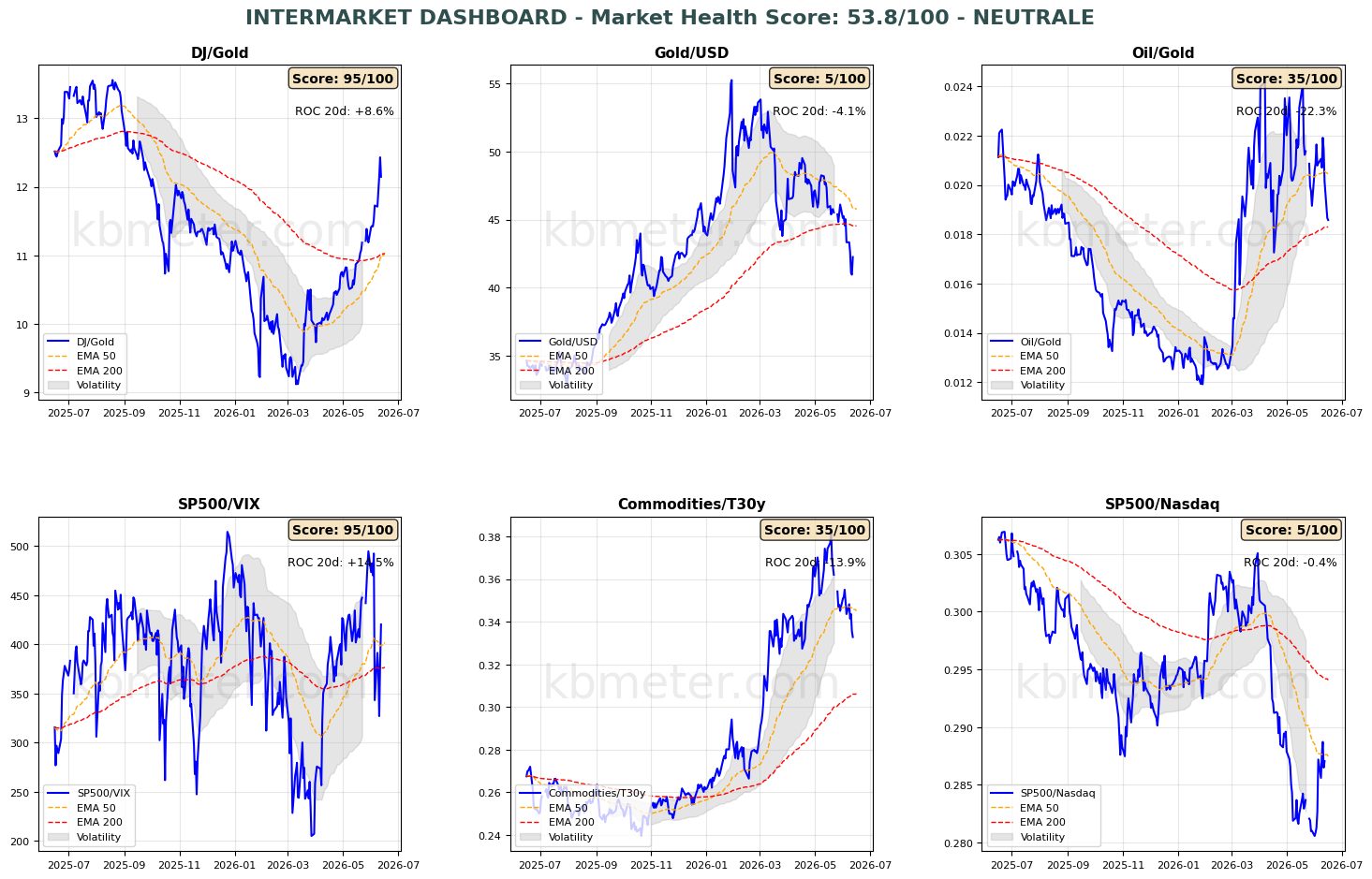

Financial markets currently exhibit a moderately positive sentiment. Intermarket analysis indicates a Market Health Score of 54/100 (neutral).

Our intermarket dashboards highlight two particularly noteworthy developments. The first concerns the Oil-to-Gold ratio, which has fallen rapidly below its 50-day moving average and is approaching support represented by the long-term moving average, returning to levels last seen in early March. The second relates to gold itself. Gold ratios show a modest recovery against both the U.S. dollar and the Dow Jones. In both cases, it is worth noting that the 50-day and 200-day moving averages are approaching a potential crossover—bearish for the Dollar/Gold ratio and bullish for the Dow/Gold ratio. The upcoming trading sessions, and particularly the Federal Reserve meeting, will help determine whether the precious metal can generate signs of improvement.

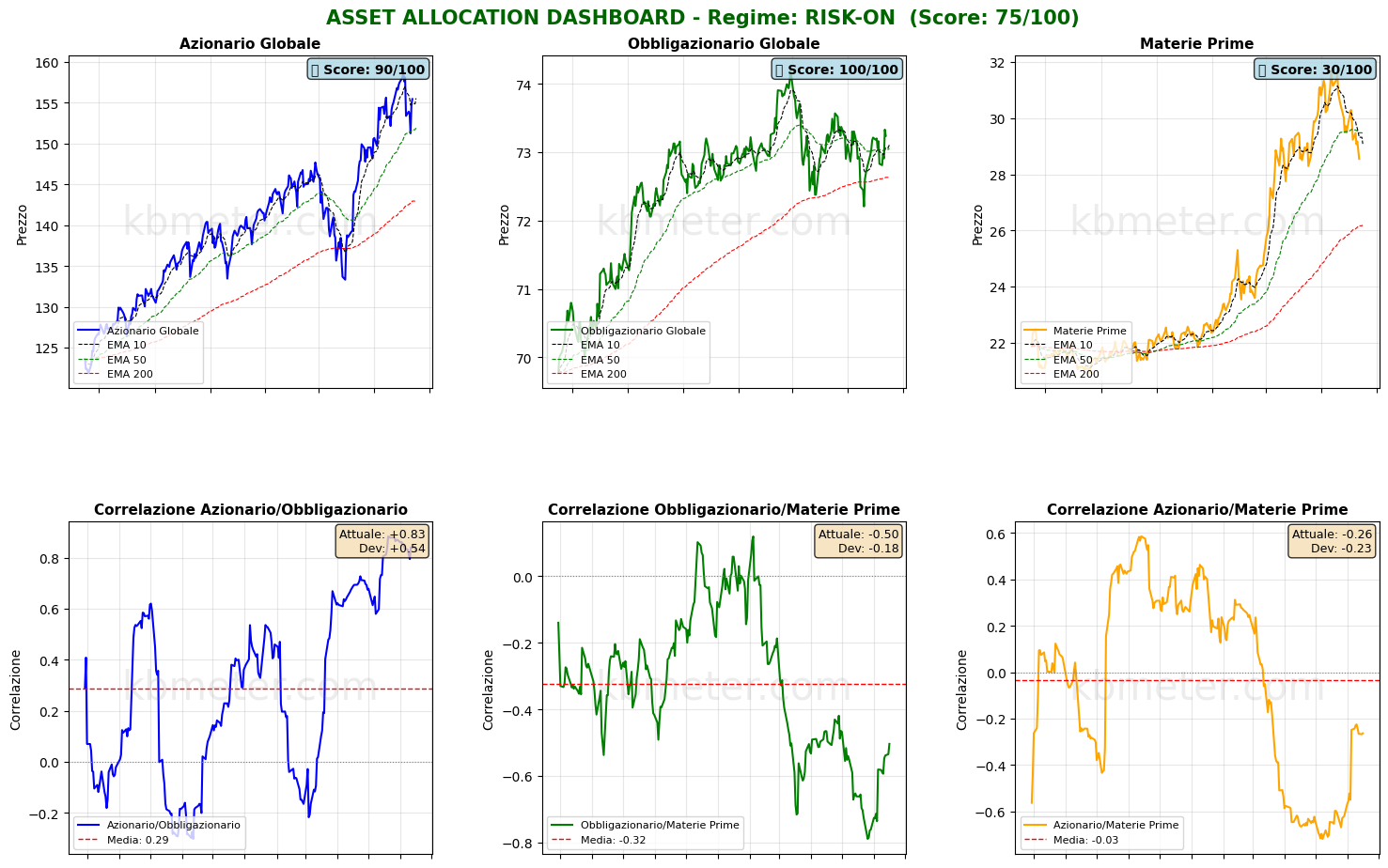

With risk appetite remaining in positive territory, asset classes are consolidating the trends observed since last weekend: equities and fixed income remain above their medium-term moving averages, while commodities continue to trade below that threshold.

Looking at our Health Scores, equities have recovered the 50-point level, with particularly notable improvements in Asia (+6 points over the past week) and South America (+10 points over the same period). Momentum remains in bullish territory, while the outlook continues to be weak. In fixed income markets, two developments stand out. First, the weakness of U.S. inflation-linked bonds may signal a reassessment of inflation expectations. Second, Eurozone bonds continue to improve despite the ECB’s policy stance. Both aspects warrant close attention in the coming days.

Global Futures – Pre-Market Sentiment

Pre-Market Futures. Global futures indicate a moderately risk-on sentiment, with an average gain of +0.24%. U.S. futures are slightly negative (-0.03%), European futures are modestly positive (+0.35%), and Asian futures are also slightly positive (+0.30%).

📊 Global Futures – Pre-Market Sentiment

- CSI 300: +2.07%

- IBEX 35 derived: +1.55%

- TecDAX derived: +1.32%

- Hang Seng derived: -1.14%

- Mini DAX: -0.20%

- US Tech 100 derived: -0.19%

Macroeconomic calendar

On the macroeconomic front, central bank week is now in full swing, highlighted by the Bank of Japan’s historic rate increase and the Australian central bank’s more conservative policy decision. Also noteworthy are the mixed data on China’s economic performance in May 2026, Germany’s ZEW survey results, first-quarter 2026 wage developments across the Eurozone, U.S. housing starts, and export trends in the United States.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 16 June 2026 - 7:39 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.