June Opens With Risk-On Mood as Tech Leads Gains, Bonds Rebound

Having closed out a risk-on month of May, financial markets are attempting to maintain positive sentiment at the start of both the new month and the new trading week. The technology sector remains the primary driver of market performance, while the rebound in fixed income suggests a repositioning of inflation expectations. The week will bring several key data releases, including the U.S. May employment report and Broadcom’s earnings results. Futures point to a positive opening for both European and U.S. markets.

Market Weather Map

June 1, 2026

US Equities

Eu Equities

Asia Equities

Commodities

Bonds

Dollar Index

Technology

Gold

Oil

Crypto

Market Summary

Do you want to see the score details for all assets monitored by KBMeter?

Try free for 14 days →Financial markets sentiment

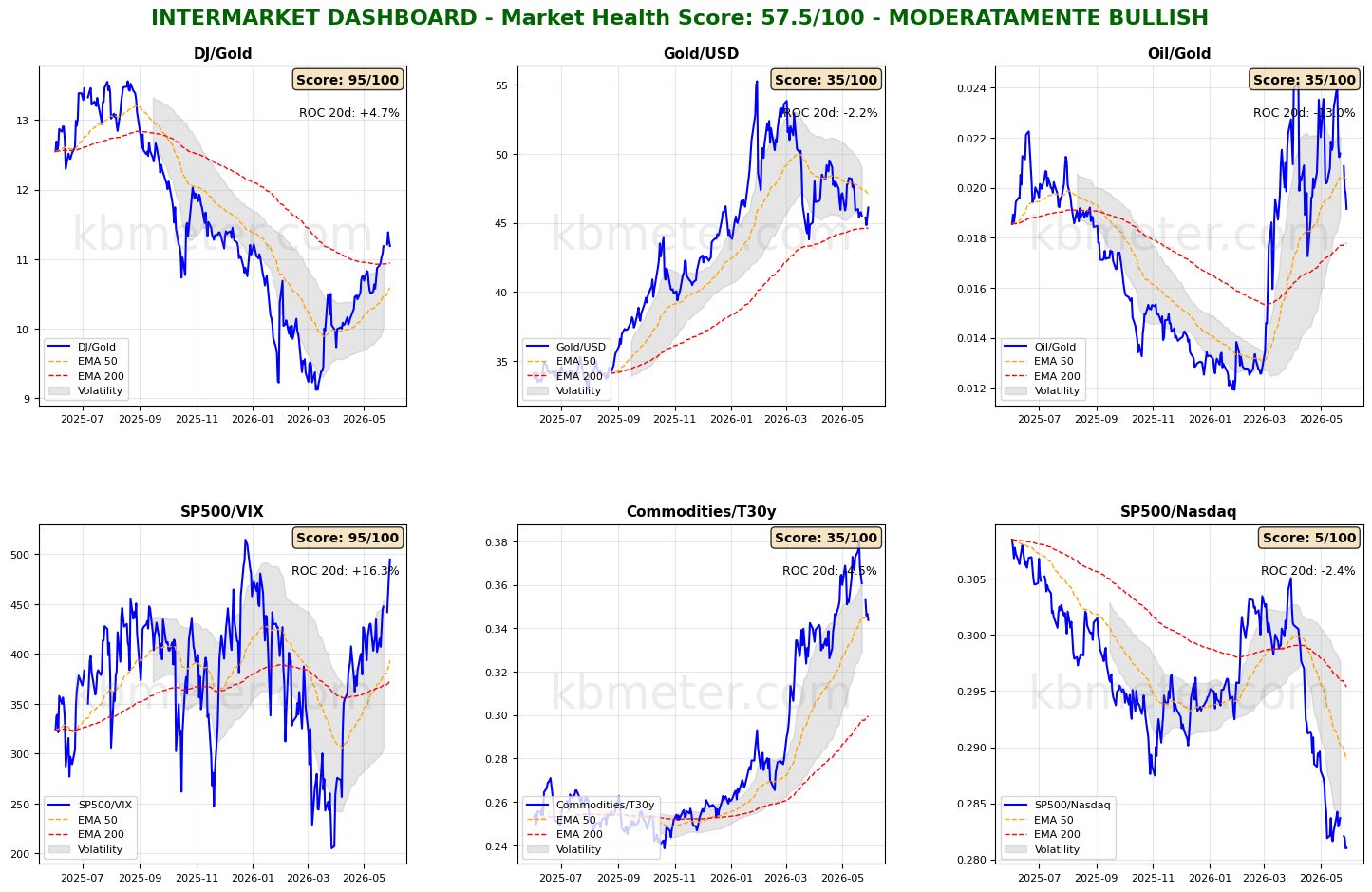

Financial markets are displaying a moderately positive sentiment today. Intermarket analysis shows a Market Health Score of 57.5/100 — slightly positive, with the regime classified as expansionary.

The S&P 500/VIX ratio is at the highest level of the observed period, indicating strong risk appetite and compressed volatility. However, a closer look reveals where this appetite is concentrated. The Commodities/Bonds ratio — which measures the cyclical differential between real assets and interest rates — remains elevated relative to the observed period, but it has reversed direction over the past week. Bonds are outperforming commodities, reflecting inflation expectations that appear more contained over time and perhaps signaling greater anticipation than action from the Federal Reserve. Meanwhile, the S&P 500/Nasdaq ratio has returned to the lows of the observed period, indicating that the strength of the equity rally remains concentrated in the technology sector.

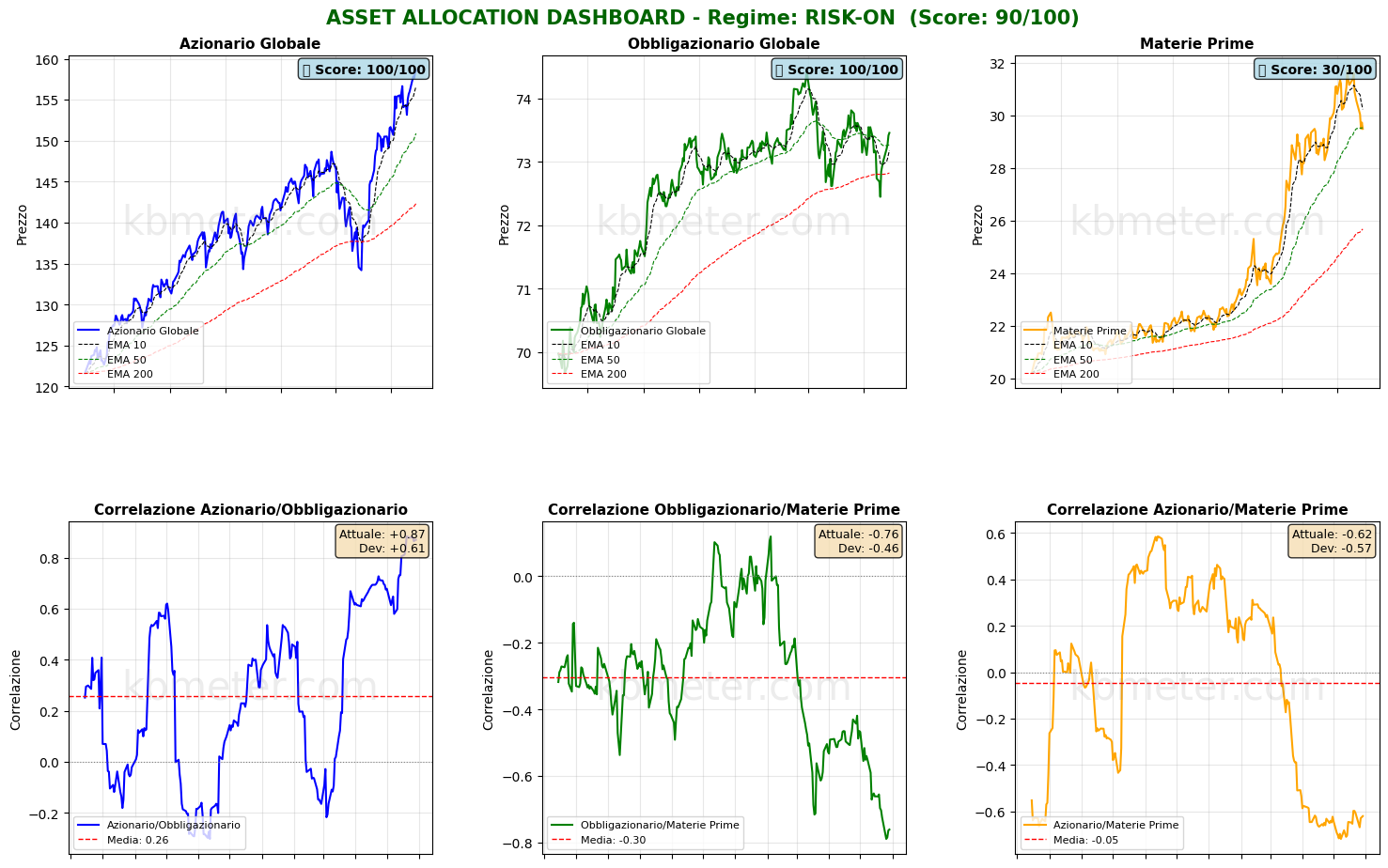

Across asset classes, the picture is largely consistent with what was observed at the end of last week. Equities remain in an uptrend, global fixed income is attempting to extend its move further above the 50-day moving average, while commodities are positioned near the support provided by their medium-term moving average.

Technology remains the strongest asset class in the system, with a health score of 64, a directional signal of +28, and a positive overall condition. Trend and momentum remain aligned, with no significant daily change, suggesting a solid underlying structure rather than a short-term move. Fixed income has recorded the strongest weekly improvement, gaining more than eight health-score points over seven trading sessions, while its directional signal has moved from negative territory to +9.

At the opposite end of the spectrum, cryptocurrencies remain under significant pressure, with a health score of 36 and a directional signal of -27, reflecting both daily and weekly deterioration. Also noteworthy is the position of European equities, which posted the strongest daily improvement among all asset classes (+2.66 points), although their weekly balance remains slightly negative. Today’s rebound therefore follows a week of relative weakness.

Global Futures – Pre-Market Sentiment

Pre-Market Futures. Global futures are signaling a moderately risk-on environment, with an average gain of +0.25%. U.S. futures are modestly positive (+0.44%), European futures are slightly positive (+0.09%), and Asian futures are also modestly positive (+0.44%).

📊 Global Futures – Pre-Market Sentiment

- TecDAX derived: +1.08%

- Nikkei 225 derived: +0.97%

- Hang Seng derived: +0.71%

- CSI 300: -0.35%

- FTSE 100 derived: -0.34%

- Euro Stoxx 50 derived: -0.21%

Macroeconomic calendar

Today’s macroeconomic agenda includes the final May PMI survey readings, Germany’s April retail sales data, India’s April industrial production figures, and the May 2026 ISM Manufacturing Survey update in the United States.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 1 June 2026 - 7:57 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.