U.S. Consumer Confidence: Intermarket Update – October 2025

A few months on, we return to update our intermarket assessment of U.S. consumer sentiment.

Overall, the indicators remain tilted toward optimism, supported by resilient confidence in the economy’s outlook. However, in recent weeks, some signs of growing caution have emerged, pointing to a more uncertain environment compared with earlier in the year.

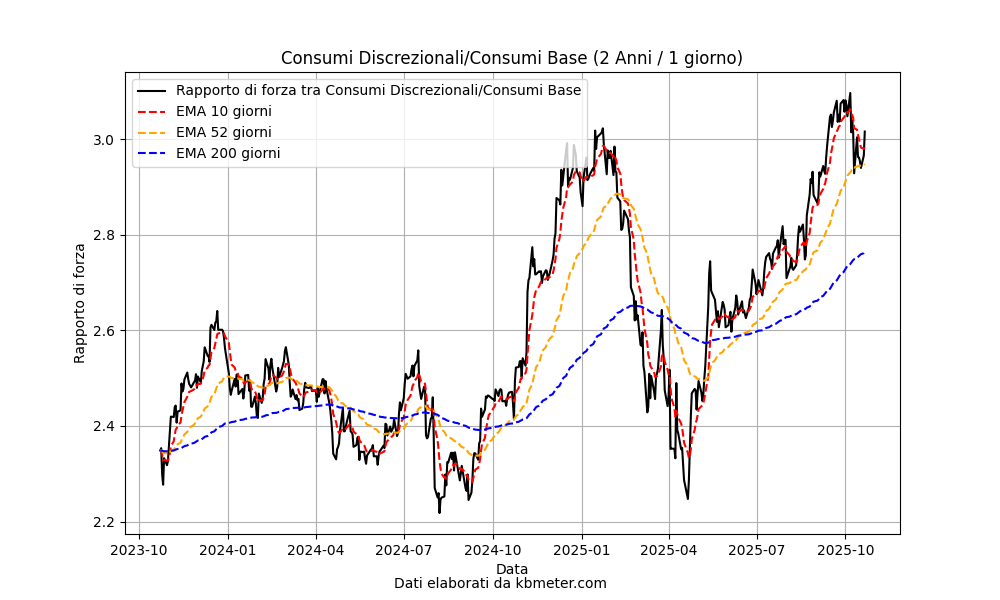

As usual, we begin by examining the relationship between the two S&P 500 consumer sectors: discretionary and staples.

The chart above highlights how, over the medium term, consumer discretionary stocks have continued to outperform consumer staples, signaling robust consumer confidence.

At the same time, it’s worth noting that since early October the indicator has shown a gradual weakening, reflecting increased uncertainty even if not yet suggesting a clear trend reversal.

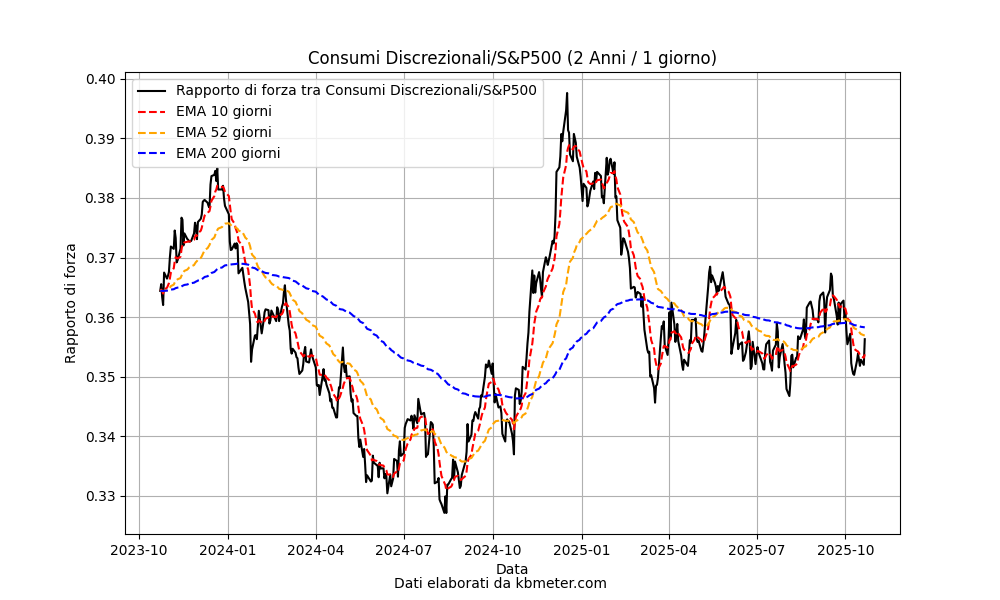

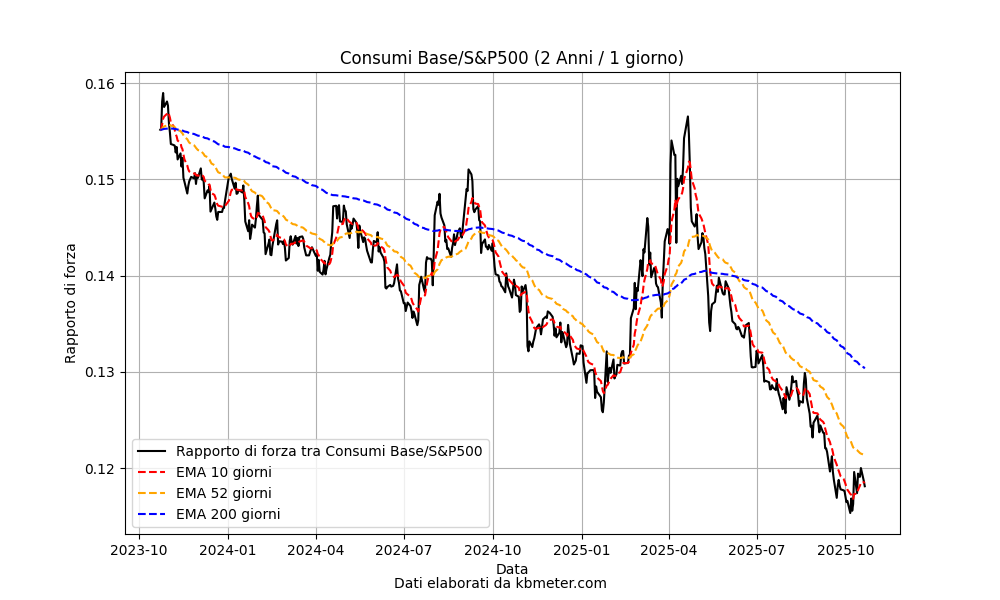

This view is confirmed by the analysis of the relative strength indicators of both sectors compared with the broader S&P 500.

On the left, the relative strength line for discretionary stocks is moving sideways — a sign of consolidation and modest loss of momentum.

On the right, meanwhile, the long phase of weakness in consumer staples appears to have bottomed out in early October, with the indicator attempting a rebound toward its 50-day moving average.

In summary, the intermarket indicators linked to consumer sentiment still point to an overall positive backdrop, though recent data highlight a rising sense of caution and a slightly more uncertain tone in the consumer outlook.