Low volatility factor, a setback for investors

When financial markets start to get rough, investors rediscover the low volatility factor. This is confirmed by data from early 2025.

In February, the Invesco S&P 500 Low Volatility ETF (SPLV) outperformed the overall index by 5.9 percentage points, its best performance since April 2022, and recorded its first positive investment-divestment balance since last August. From December 2024 to date, the S&P500 index has not gained substantially, while the Low Volatility factor has outperformed by more than 5 per cent.

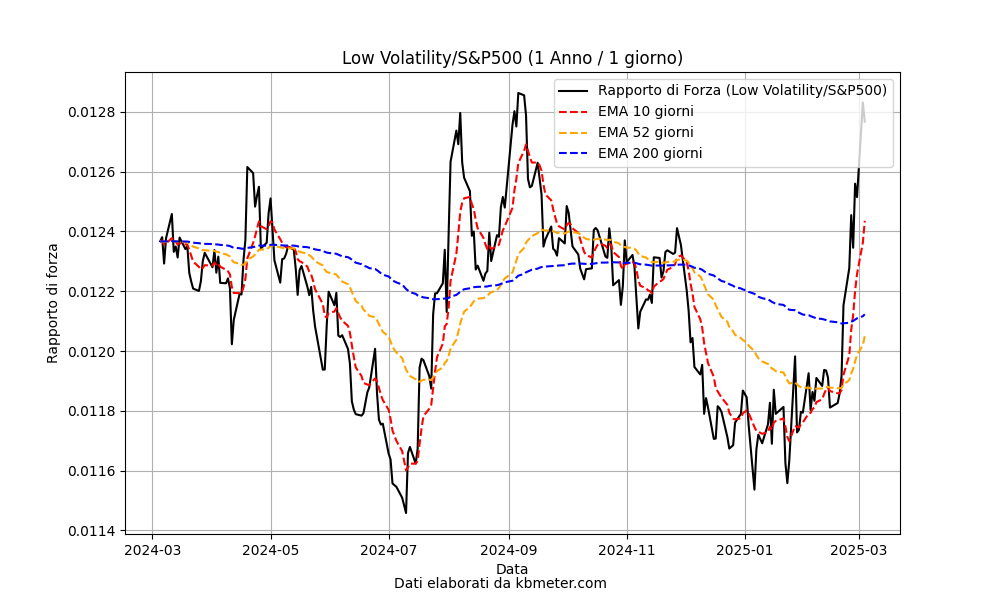

The relative strength ratio between the SPLV and the S&P500, graph above, shows the surge of the low volatility factor in February, with the indicator returning to the highs since last September. The last year also seems to indicate a much more balanced relationship between the overall index and low volatility.

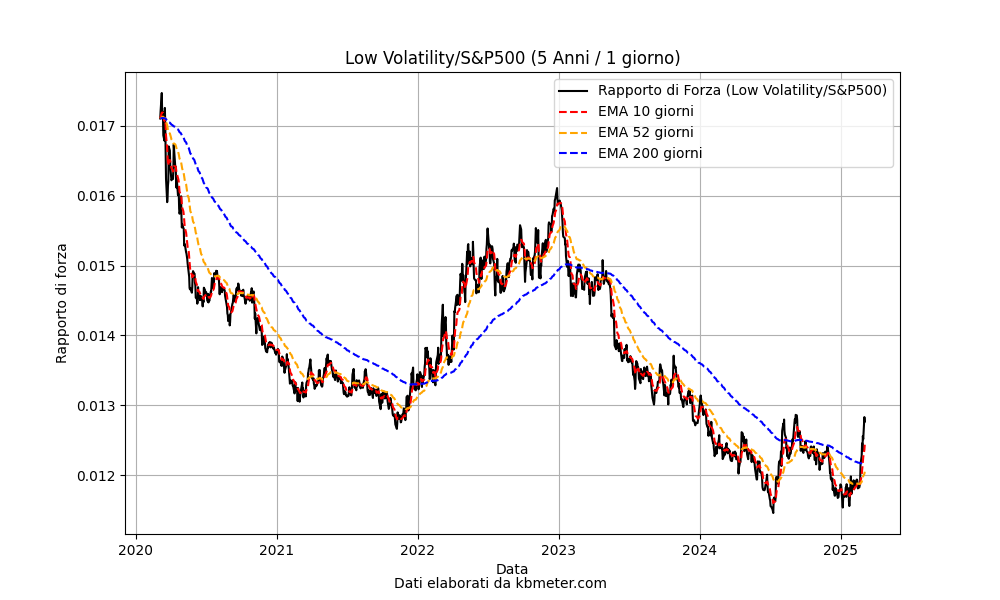

Extending the time horizon to five years, we observe how the general index has always done better than Low Volatility from the beginning of 2023 onwards. Now the ratio has broken through the 200-day moving average, a signal which, if confirmed, could indicate a new trend reversal, like the one at the end of 2022.