US inflation freezes markets’ expectations

More persistent inflation than expected reduces the chances of new Fed intervention in the short term, and financial markets reacted with another weak day in equities and rising bond yields.

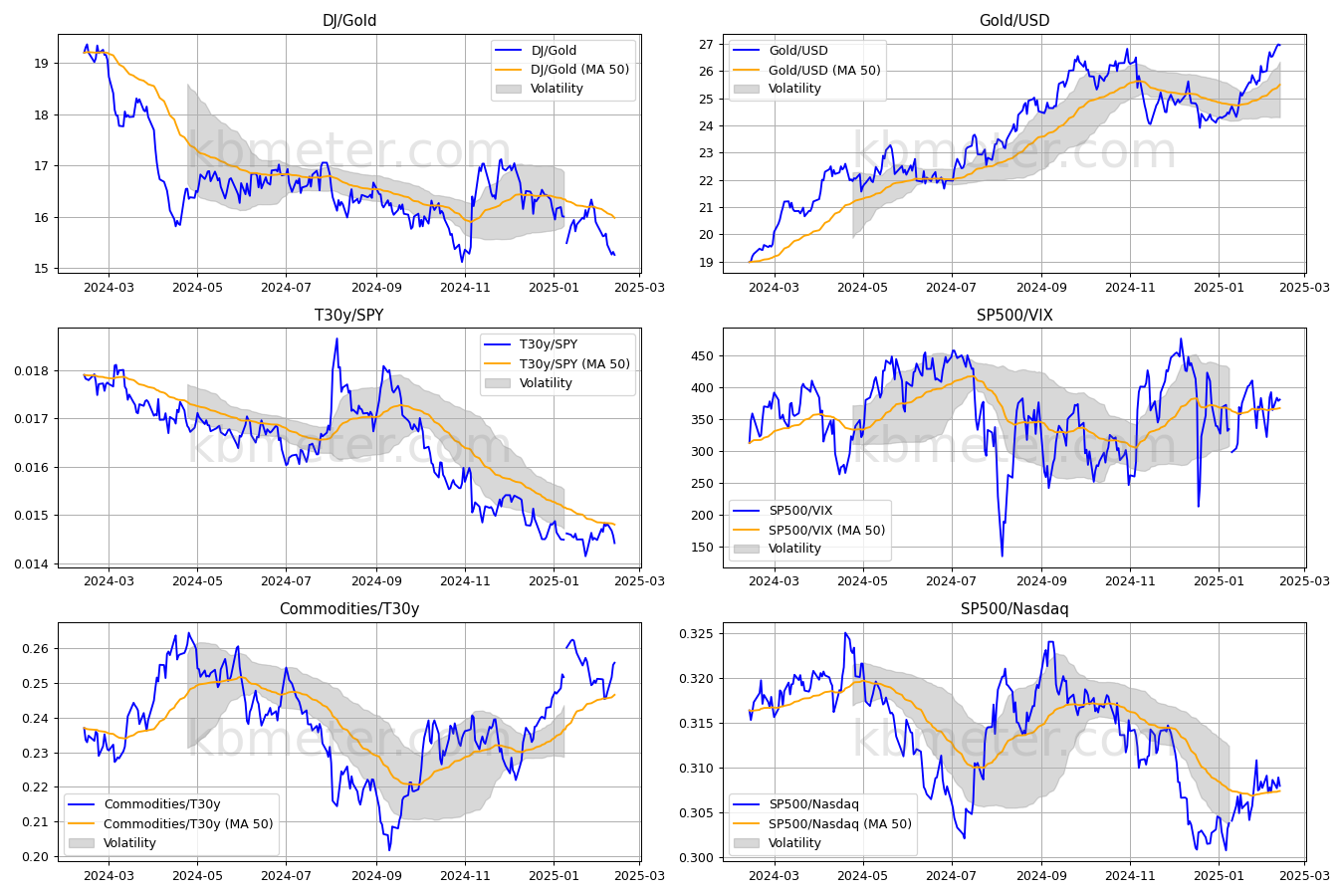

Looking at our intermarket dashboards, we first observe the movement in bonds, the resistance we have been talking about for a few weeks now rejecting the recent attempt to reaccelerate prices. Note yesterday’s decline in the light of unflattering US inflation data. The trend is still bullish for the relationship between Gold and the Dollar, while we are witnessing a recovery in the strength of the Nasdaq against the S&P500.

On the macroeconomic front, after the higher-than-expected inflation data, producer price numbers are awaited in the US, hoping that at least these will show signs of cooling. In Europe, on the other hand, the wait is for economic growth numbers in Great Britain in the last quarter of 2024. Expectations are for a minus sign.

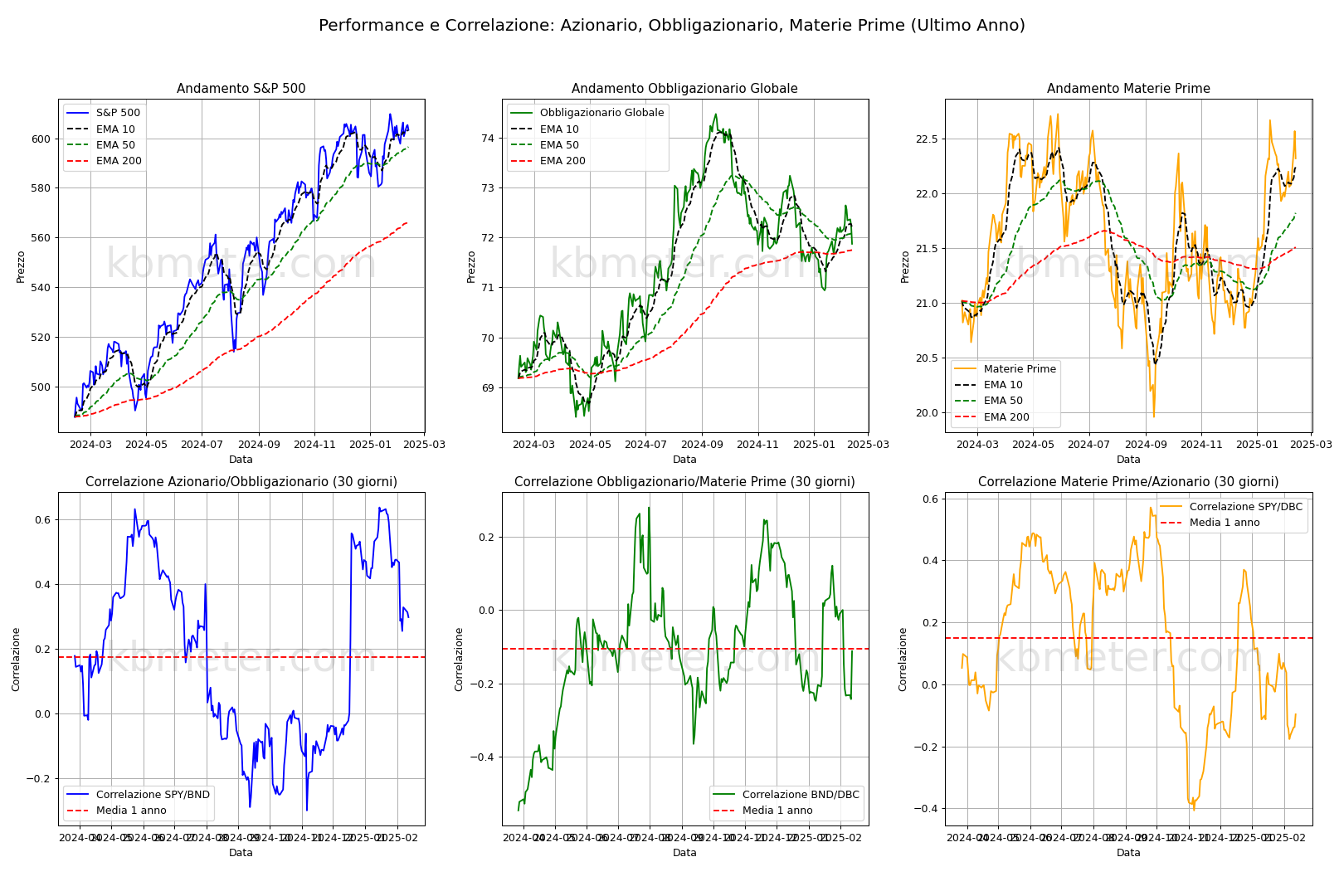

Our forecast analyses continue to indicate an interlocutory phase for the major asset classes. In equities, there continue to be better indications for Europe than for the US. Buying signals for US government bond yields. Volatility in the normal range, somewhat higher for equities.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 13 February 2025 - 7:32 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.