U.S. Tech Gains on Buy-the-Dip Demand and IPO Buzz; Strong Dollar Weighs on Asia and Bonds

Financial market sentiment remains between neutral and moderately positive. The return of the buy-the-dip strategy has reignited enthusiasm for the U.S. technology sector (with SpaceX reportedly preparing for a Nasdaq listing, OpenAI moving toward an IPO, and Marvell set to join the S&P 500), while pressure continues in the background on the U.S. dollar (higher) and bonds (lower) as markets respond to persistent expectations of elevated inflation and interest rates. Cryptocurrencies remain under pressure, while gold continues its phase of weakness. Volatility remains subdued. Futures indicate a positive opening for the United States and a flat start for Europe.

Market Weather Map

June 9, 2026

US Equities

Eu Equities

Asia Equities

Commodities

Bonds

Dollar Index

Technology

Gold

Oil

Crypto

Market Summary

Do you want to see the score details for all assets monitored by KBMeter?

Try free for 14 days →Financial markets sentiment

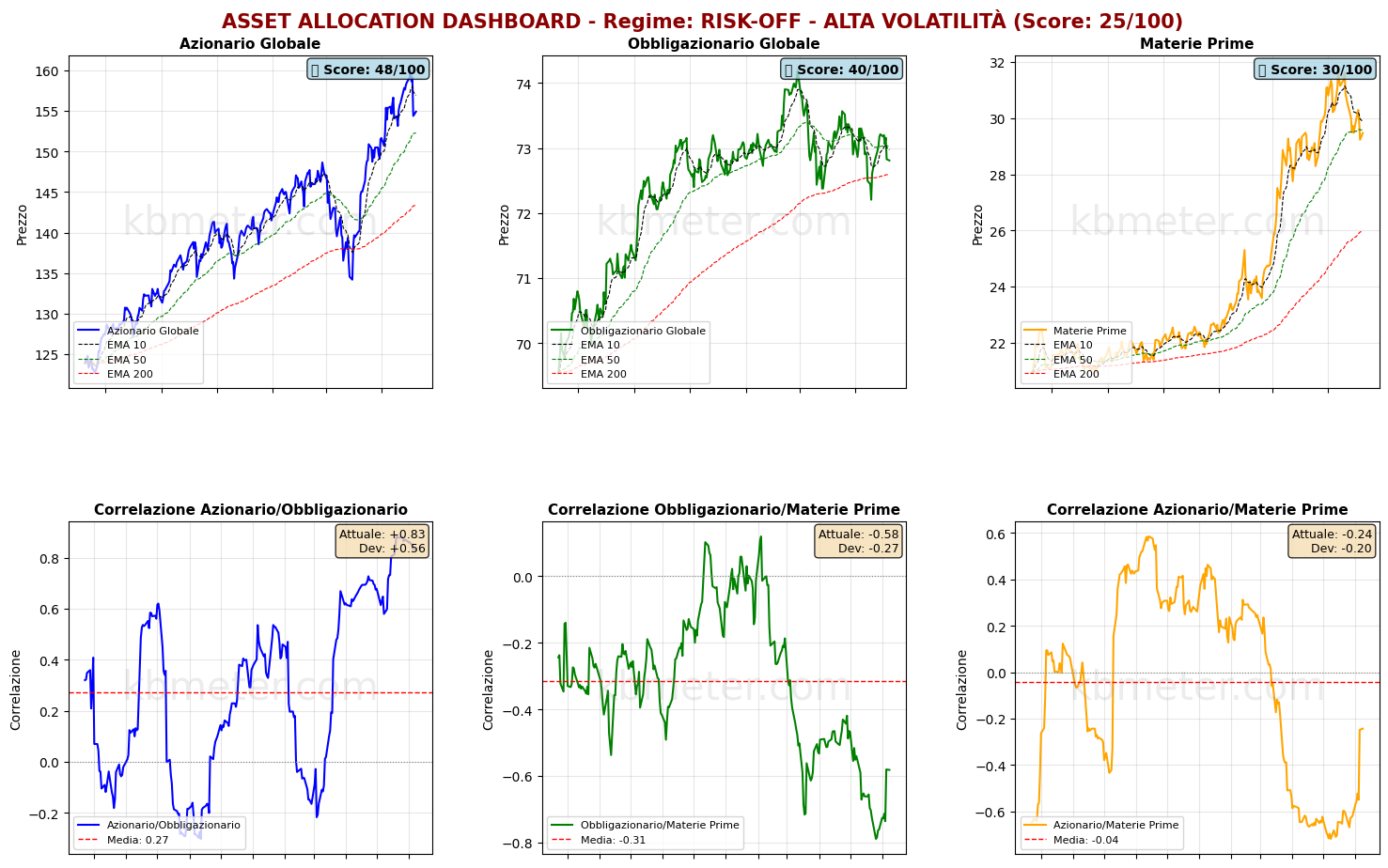

Financial markets are showing a neutral sentiment today. Intermarket analysis points to a Market Health Score of 56/100, indicating a moderately positive environment. Buy-the-dip activity has returned, partially absorbing last Friday’s sell-off in the technology sector. Our intermarket dashboards show the S&P 500/VIX ratio moving back above its long-term average, while the S&P 500/Nasdaq ratio has been rejected at the resistance represented by its 50-day moving average.

Beyond this isolated short-term move, market signals remain largely unchanged. The U.S. dollar continues to outperform gold, with the precious metal losing ground both against the Dow Jones (the ratio is at its highest level since November last year) and against crude oil. The Commodities-to-Bonds ratio remains around its 50-day moving average, currently lacking a clear direction as markets await macroeconomic data capable of reshaping inflation expectations.

As far as asset classes are concerned, there have been no major movements. Global equities have recovered from last Friday’s decline but remain below their 10-day moving average, suggesting that the rebound is still not particularly convincing. Global bonds also appear directionless at the moment, although they continue to trade below their medium-term moving average.

Our market weather map, which tracks the health scores of a selected range of assets, shows that investors continue to rely on two distinct narratives. On one hand, a strong U.S. dollar (weighing on Asian equities and emerging-market bonds) and bond markets remaining below neutral levels point to expectations of rising inflation and interest rates. On the other hand, the technology sector is once again approaching a health score of 60, more than 10 points above the average score of the sectors within the S&P 500.

Global Futures – Pre-Market Sentiment

Pre-Market Futures: Global futures are signaling a mildly risk-off sentiment (-0.05% on average), with U.S. futures slightly positive (+0.30%), European futures marginally positive (+0.03%), and Asian futures negative (-0.79%).

📊 Global Futures – Pre-Market Sentiment

- FTSE MIB derived: +0.64%

- US Tech 100 derived: +0.52%

- Russell 2000: +0.33%

- CSI 300: -2.24%

- IBEX 35 derived: -0.60%

- Nikkei 225 derived: -0.18%

Macroeconomic calendar

On the macroeconomic front, the day will be characterized by international trade data for April and May, including Chinese export figures for last month and April trade data from Germany, Canada, and the United States. Investors will also focus on Germany’s April 2026 industrial production data, the latest update on Australian consumer confidence, U.S. existing home sales for May, and the weekly ADP employment report.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 9 June 2026 - 7:47 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.