U.S. May Jobs Data Looms as Tech Rally Stalls; Markets Search for Fresh Catalysts to Sustain Risk-On Sentiment

In an equity rally driven almost exclusively by the technology sector, Broadcom’s weaker-than-expected results were enough to put the brakes on the market’s advance. Equity markets are heading toward the end of the week with the key market-moving event being the release of the U.S. labor market data for May 2026. Meanwhile, the U.S. dollar remains strong, and renewed weakness in the bond market continues to highlight the importance of the inflation and interest rate narrative.

Market sentiment remains tilted toward a risk-on environment, while volatility stays at normal levels. Futures point to a flat opening in Europe and a weaker start in the United States.

Market Weather Map

June 5, 2026

US Equities

Eu Equities

Asia Equities

Commodities

Bonds

Dollar Index

Technology

Gold

Oil

Crypto

Market Summary

Do you want to see the score details for all assets monitored by KBMeter?

Try free for 14 days →Financial markets sentiment

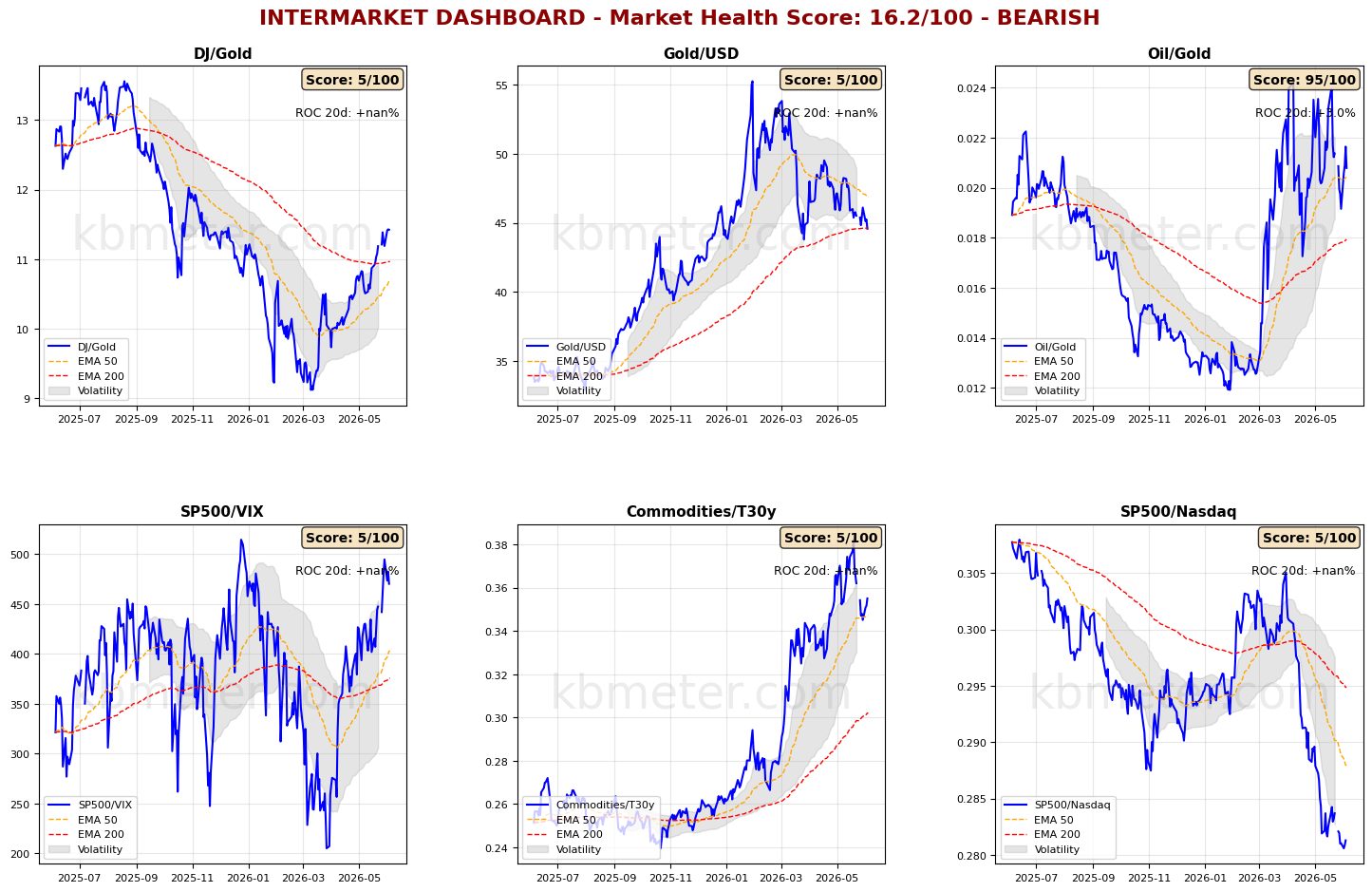

Financial markets currently exhibit a neutral sentiment. Intermarket analysis shows a Market Health Score of 16/100 (negative). Among our intermarket indicators, the U.S. Dollar-to-Gold ratio is testing support at its long-term moving average, signaling both renewed strength in the greenback and weakness in gold (with the Dow/Gold ratio at its highest level since November of last year).

Risk appetite indicators remain broadly unchanged, while inflationary pressures continue to support the rebound in the Commodities/Bonds ratio from its medium-term moving average.

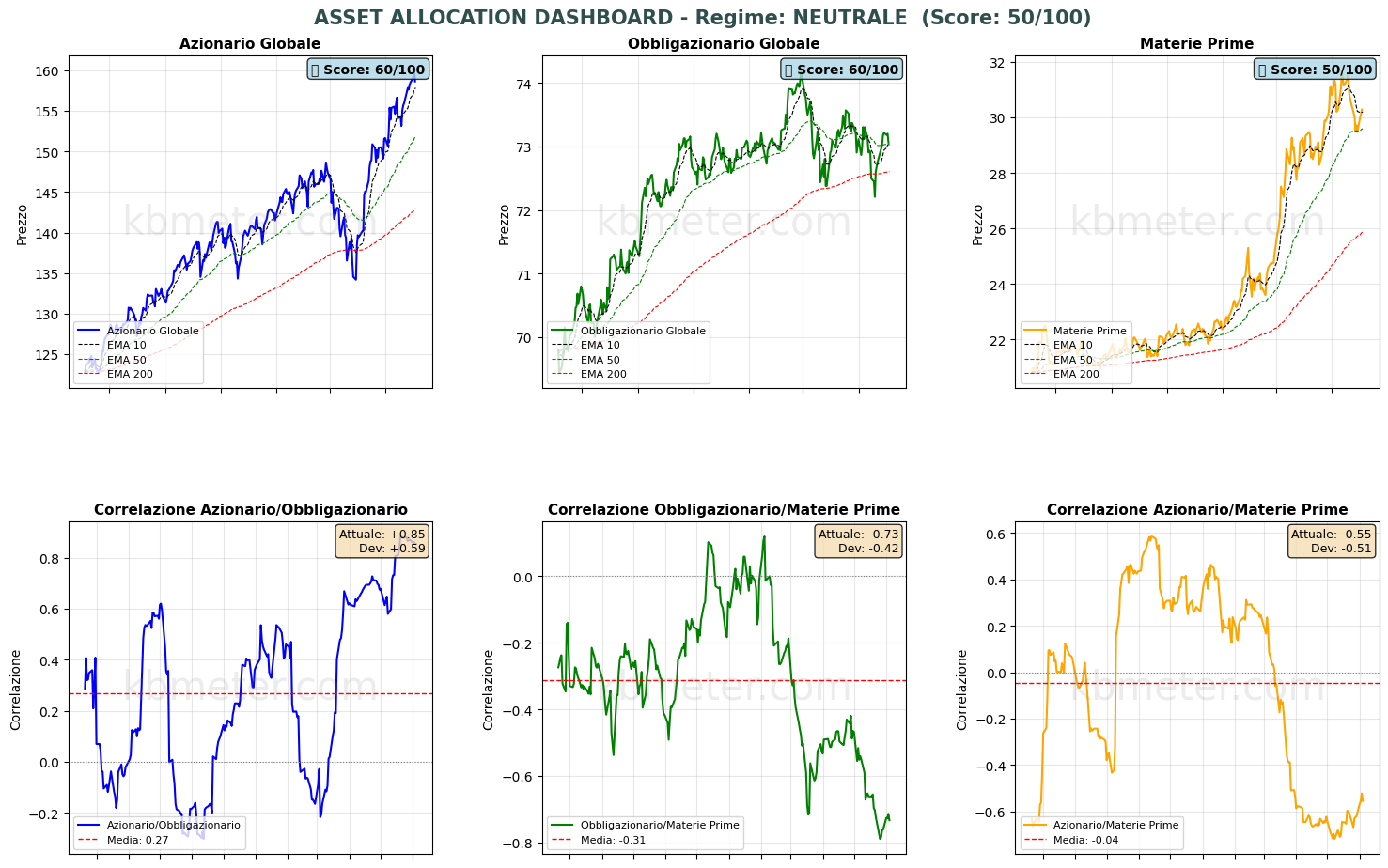

The overall asset-class picture does not show any significant short-term shifts. However, it is worth emphasizing once again that an equity rally driven largely by a single sector has limited sustainability unless additional sources of support emerge. Otherwise, inflation and slowing economic growth could become the dominant themes across financial markets.

Our market weather map shows that only the U.S. dollar remains above the 60-point health score threshold, while all other asset classes are experiencing sharp daily declines.

Global Futures – Pre-Market Sentiment

Pre-Market Futures: Global futures indicate a moderately risk-off sentiment (-0.29% on average), with U.S. futures slightly negative (-0.47%), European futures marginally positive (+0.01%), and Asian markets weaker (-0.93%).

📊 Global Futures – Pre-Market Sentiment

- IBEX 35 derived: +0.76%

- TecDAX derived: +0.60%

- FTSE MIB derived: +0.25%

- Nikkei 225 derived: -1.39%

- US Tech 100 derived: -0.82%

- Hang Seng derived: -0.72%

Macroeconomic calendar

Today’s macroeconomic calendar is dominated by employment-related data. During the morning session, final first-quarter 2026 labor market figures for the Eurozone will be released. In the afternoon, attention will shift to the highly anticipated U.S. jobs report and Canadian employment data, both referring to May 2026.

Among other key releases, investors will also be watching the final revision of Eurozone first-quarter 2026 GDP and India’s economic growth figures for the first three months of the year, following the central bank’s decision to leave interest rates unchanged.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 5 June 2026 - 7:53 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.