Tech Acts as Market Lightning Rod as Uncertainty Builds; Micron Earnings Loom

The U.S. technology sector continues to act as a lightning rod for financial markets: the first to rebound when optimism returns, and the first to come under pressure when uncertainty regains control of investor sentiment.

The underlying market tone remains broadly risk-on, although signs of sectoral and geographic rotation continue to emerge in our health scores. Investors are awaiting Micron’s earnings results for further insight into the health of the technology sector, while tomorrow’s PCE inflation data and next week’s labor market figures are likely to amplify—or dampen—current market movements.

Meanwhile, the strong U.S. dollar continues to weigh on gold and commodities, while oil remains weak despite the ongoing and still uncertain negotiations between Iran and the United States. Futures point to a slightly positive opening in the U.S. and a negative start in Europe.

Market Weather Map

June 24, 2026

US Equities

Eu Equities

Asia Equities

Commodities

Bonds

Dollar Index

Technology

Gold

Oil

Crypto

Market Summary

Do you want to see the score details for all assets monitored by KBMeter?

Try free for 14 days →Financial markets sentiment

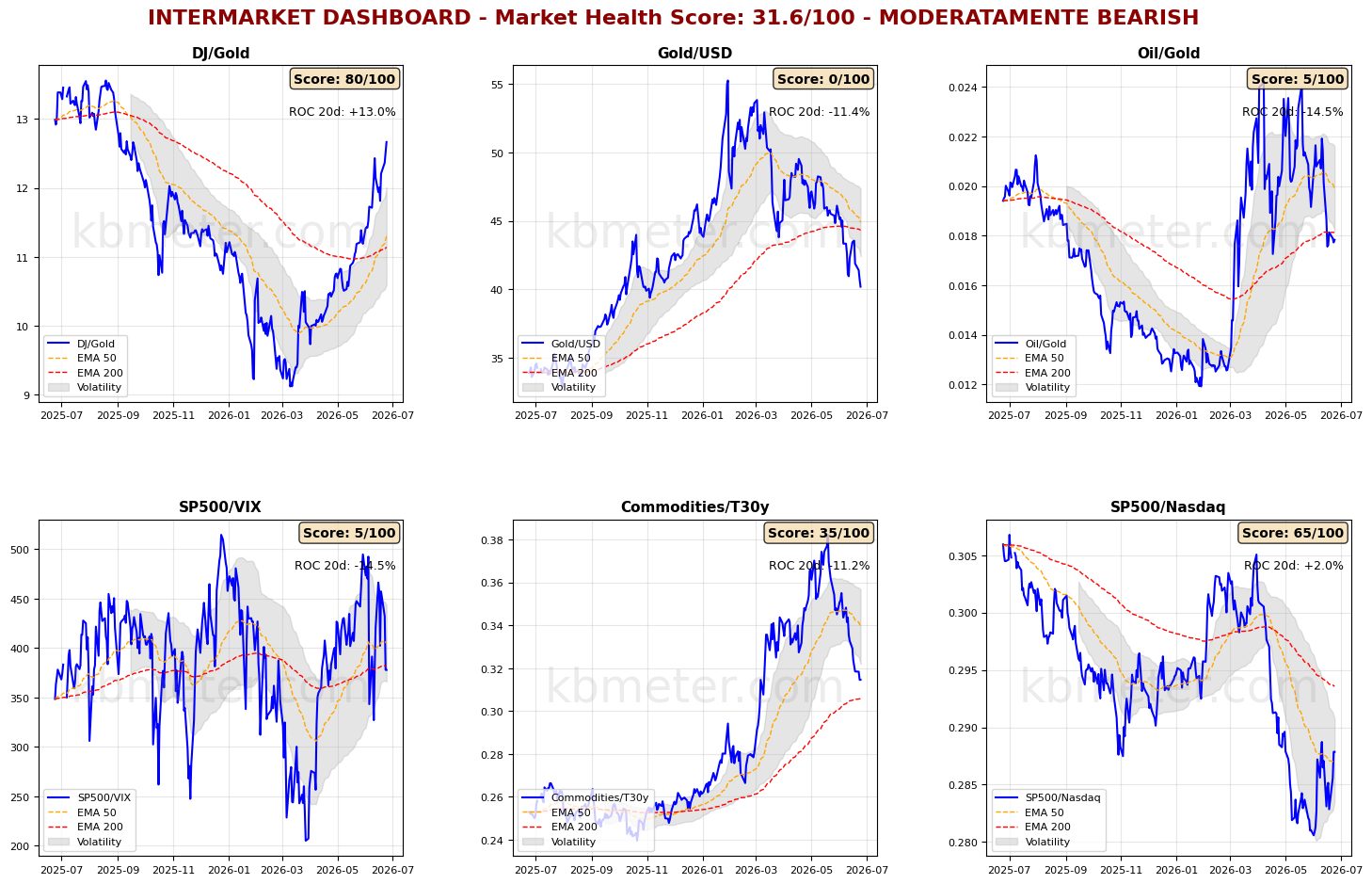

Financial markets are displaying a neutral sentiment today. Intermarket analysis shows a Market Health Score of 32/100 (negative). Uncertainty continues to weigh on our intermarket dashboards, particularly with regard to risk appetite.

The S&P 500/VIX ratio remains highly volatile and yesterday declined to its long-term moving average, a support area that is likely to be tested further in the coming sessions. The S&P 500/Nasdaq ratio highlights the source of this weakening risk-on momentum: technology stocks are effectively the market’s lightning rod, leading advances during periods of optimism but also being the first to suffer when sentiment turns more cautious. The ratio has moved above its medium-term moving average, a resistance area that was already tested a few sessions ago.

Gold continues to show signs of weakness. The Dow/Gold ratio has climbed to its highest level since September 2025, while the Dollar/Gold ratio has fallen back to levels last seen in November 2025, below its long-term moving average.

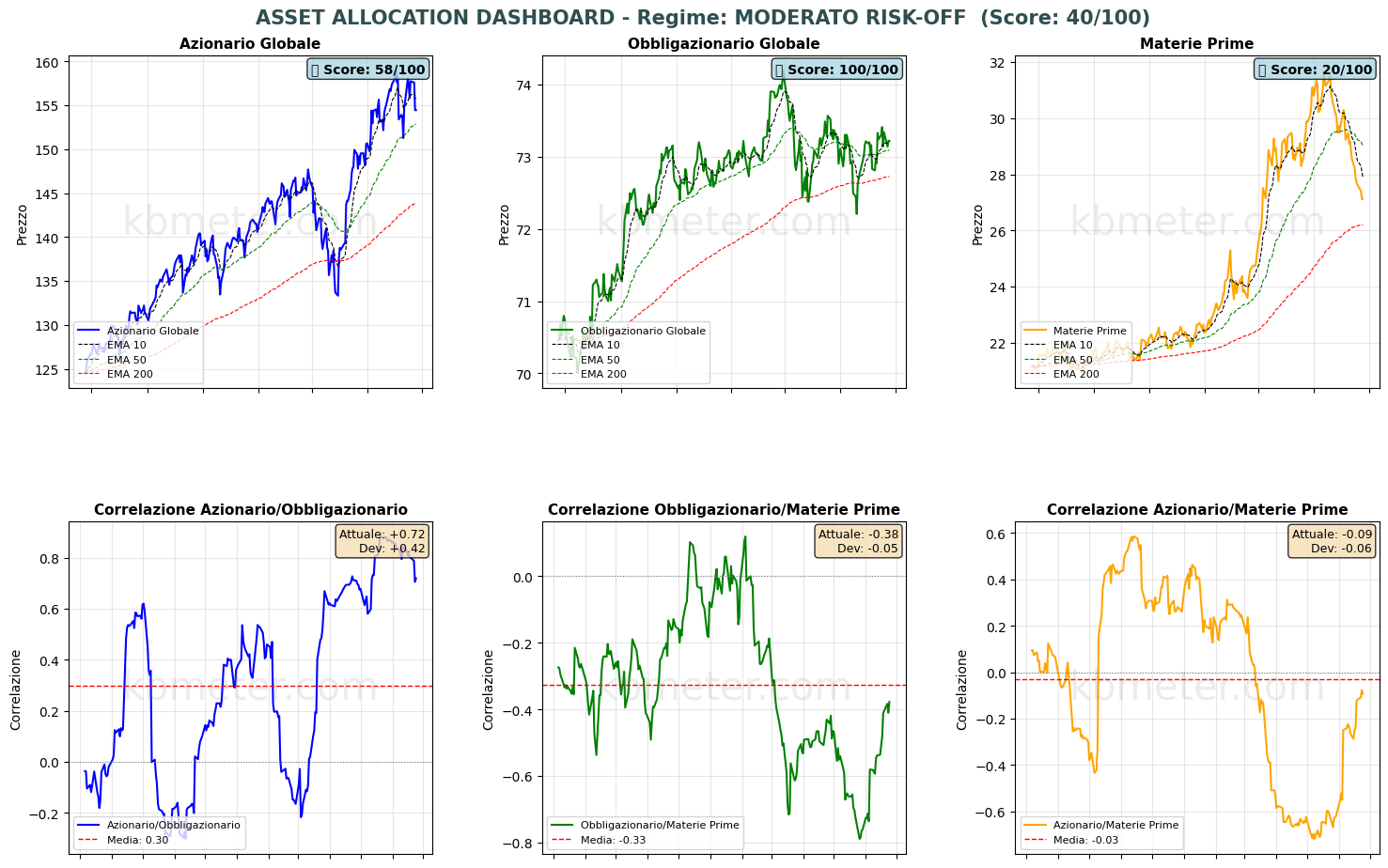

Across asset classes, the divergence between global equities and bonds on one side—still in a short-term uptrend and above their medium-term moving average—and commodities on the other remains evident, with commodities continuing their bearish approach toward the long-term moving average.

Our weather map highlights the rapid deterioration in the U.S. technology sector, although the broader U.S. equity market remains above the 50-point threshold. Conditions remain challenging for gold, oil, and cryptocurrencies.

Among the most significant daily changes, emerging markets lost 13 points, while semiconductors declined by 9 points. Noteworthy gains were recorded in both the European and U.S. pharmaceutical sectors, as well as in the main Milan stock index.

Global Futures – Pre-Market Sentiment

Pre-Market Futures. Global futures indicate a moderate risk-off sentiment (-0.46% on average), with U.S. futures slightly positive (+0.17%), European futures slightly negative (-0.45%), and Asian futures sharply lower (-1.34%).

📊 Global Futures – Pre-Market Sentiment

“`- US Tech 100 derived: +0.42%

- US 500 derived: +0.22%

- Russell 2000: +0.07%

- CSI 300: -3.02%

- FTSE MIB derived: -1.49%

- TecDAX derived: -1.09%

Macroeconomic calendar

On the macroeconomic front, the day offers limited catalysts. Key releases include Australia’s May 2026 inflation data, the June update on German business confidence, and U.S. mortgage market activity.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 24 June 2026 - 7:54 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.