Risk Appetite Improves, Gold Finds Support While Technology Remains Fragile

The week opens with financial markets still characterized by a neutral sentiment, albeit with a slight risk-on bias. Investors will seek to digest the latest U.S. labor market data and Eurozone inflation figures, translating them into expectations for the next moves by central banks. Gold and the U.S. dollar will be the key assets to watch, with gold attempting to recover—despite its current weakness—on expectations that interest rates may at least remain stable. The technology sector remains in a state of uncertainty, as a convincing reacceleration will likely require strong corporate earnings results. Meanwhile, European equities continue to post higher Health Scores than the U.S. market. Equity futures point to a positive opening for both the United States and Europe.

Market Weather Map

July 6, 2026

US Equities

Eu Equities

Asia Equities

Commodities

Bonds

Dollar Index

Technology

Gold

Oil

Crypto

Market Summary

Do you want to see the score details for all assets monitored by KBMeter?

Try free for 14 days →Financial markets sentiment

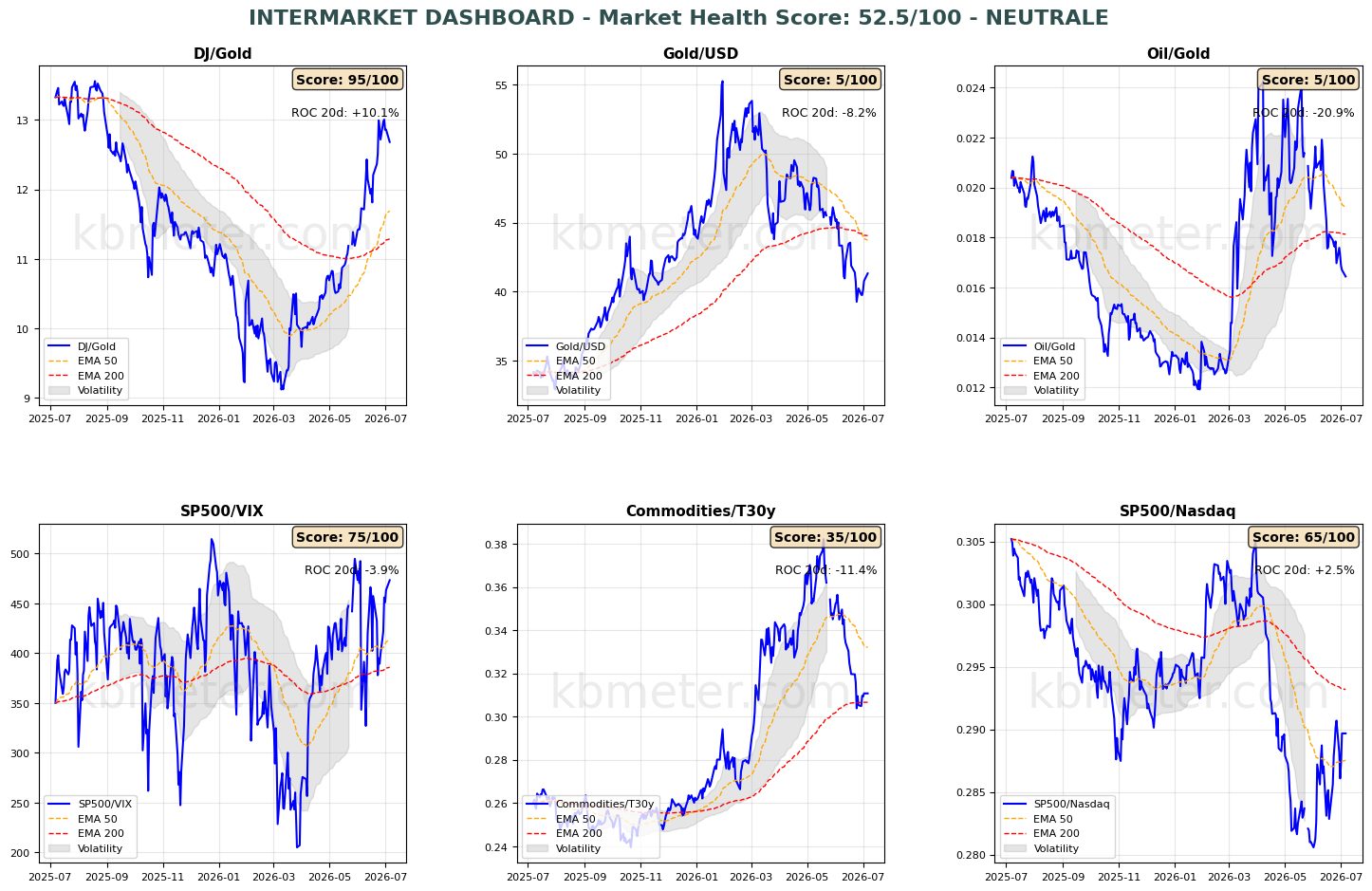

Financial markets currently display a neutral to moderately positive sentiment. Our intermarket analysis shows a Market Health Score of 52/100, indicating a neutral environment.

Looking at our intermarket dashboards, this week’s key development could emerge from the relationship between the U.S. dollar and gold. Markets now appear to have largely recalibrated their inflation expectations, as reflected by the Commodities/Bonds ratio, which remains stable around its 200-day moving average. In addition, the latest U.S. labor market data have pushed back, at least for a few months, expectations of another Federal Reserve rate hike.

Our proprietary scores suggest that it is still too early to draw firm conclusions. The dollar remains fundamentally strong, while gold continues to exhibit weakness. However, score levels above 65 and around 40 have historically tended to coincide with the formation of market highs and lows, respectively. Without extrapolating too far, we note that the Gold/U.S. Dollar ratio, while still in a bearish configuration, is attempting to rebound from last November’s lows. Similarly, the Dow Jones/Gold ratio has started to retrace from its September highs.

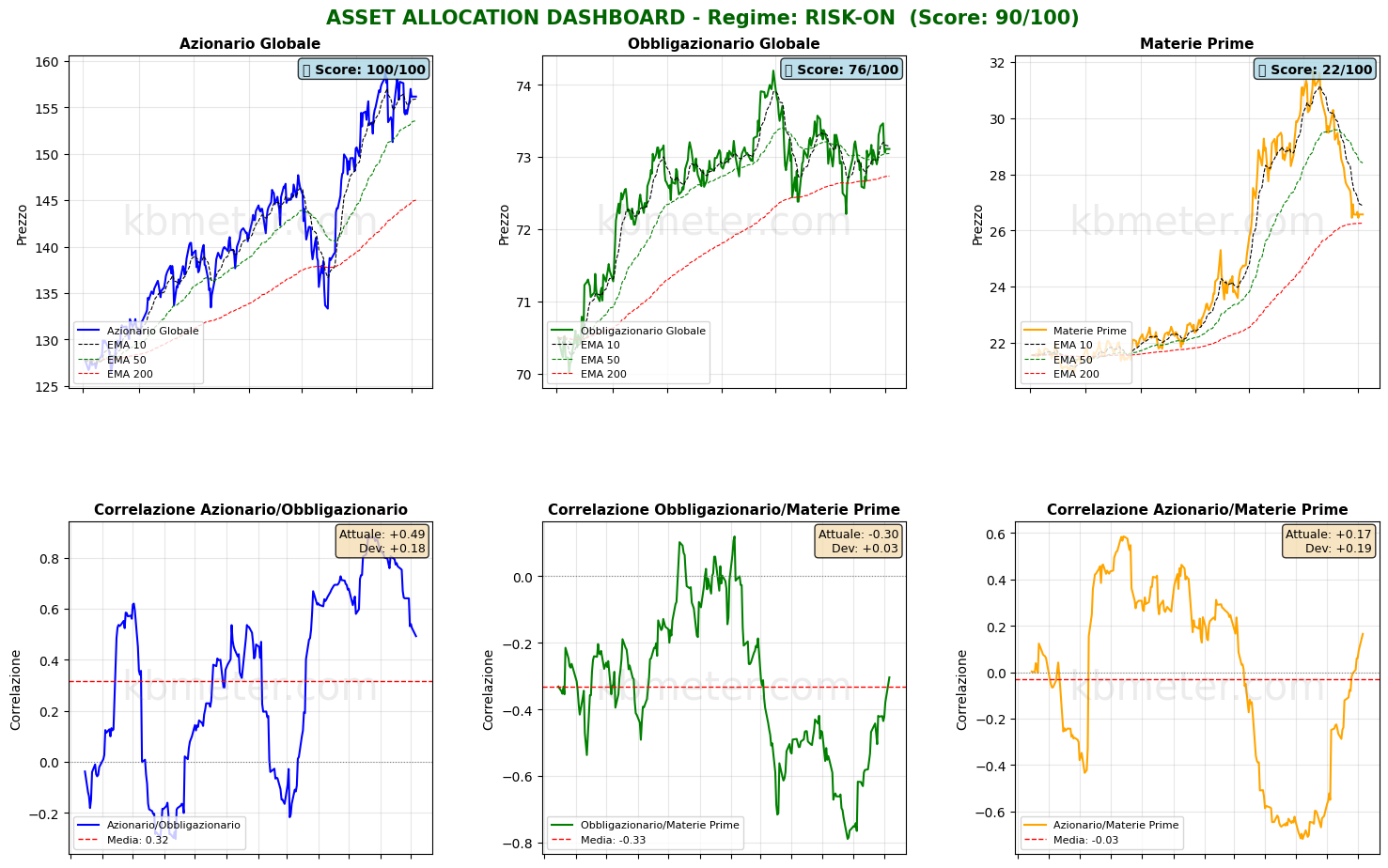

Across asset classes, the overall picture remains broadly unchanged. Commodities continue to trade around their long-term moving average, while equities remain the only major asset class trading above all three of our key moving averages.

Regarding our Health Scores, we have already highlighted the outlook for gold and the U.S. dollar. Elsewhere, both U.S. and European equities continue to register scores above 50. Among the most notable developments, we highlight the renewed acceleration in the DAX, alongside a loss of momentum in the energy and telecommunications sectors, as well as in short-term TIPS.

Global Futures – Pre-Market Sentiment

Pre-Market Futures. Global equity futures indicate a moderately risk-on tone, with an average gain of +0.34%. U.S. futures are modestly higher (+0.24%), European futures are also slightly positive (+0.29%), while Asian markets are outperforming with gains of +0.65%.

📊 Global Futures – Pre-Market Sentiment

- Hang Seng derived: +1.16%

- IBEX 35 derived: +1.09%

- TecDAX derived: +0.90%

- Euro Stoxx 50 derived: -0.12%

- FTSE 100 derived: -0.11%

- Nikkei 225 derived: -0.07%

Macroeconomic calendar

On the macroeconomic front, today’s calendar includes Eurozone May retail sales, May producer price inflation (PPI), May German factory orders, and the June U.S. ISM Services PMI.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 6 July 2026 - 7:25 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.