Now investors are once again paying attention to economic data

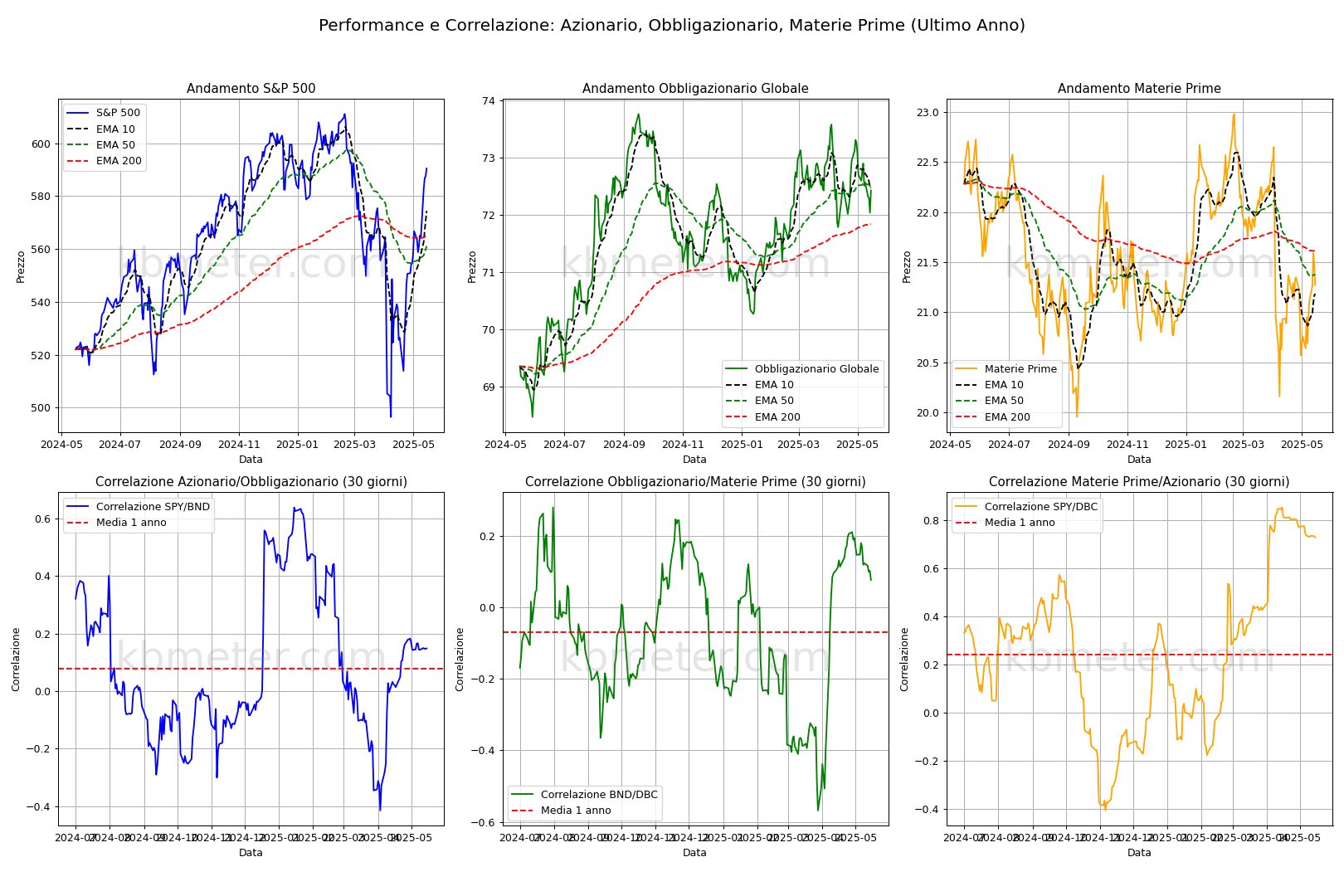

Investors are returning to the economy’s numbers and adopting a more cautious approach this weekend. Walmart’s announcement of rising prices due to tariffs and weak US retail sales dampened enthusiasm. However, the recovery in equities seems likely to continue, albeit at a slower pace. Bonds are still on an upward trend.

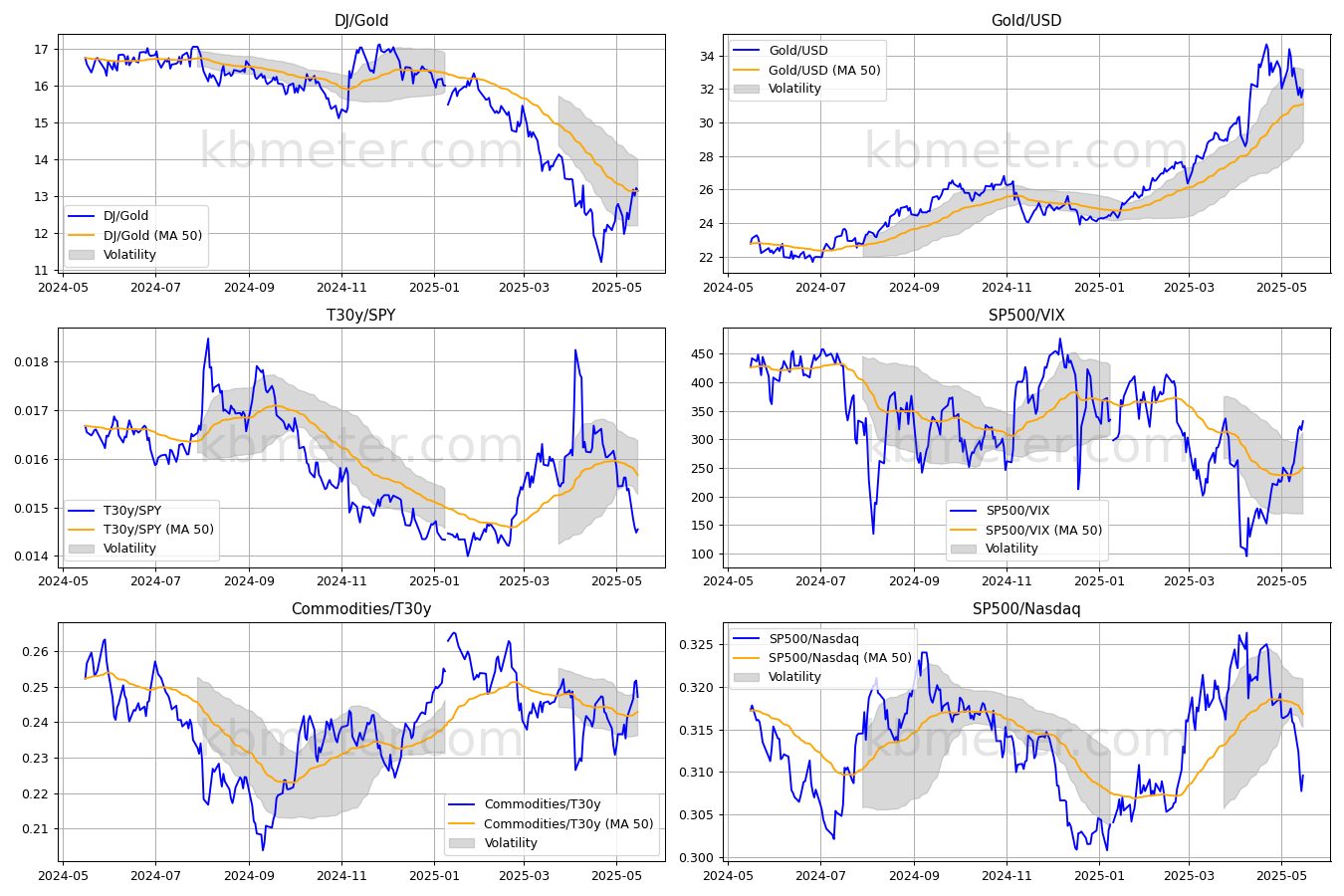

The momentum of the equity rally has definitely diminished towards the end of the week. Although our intermarket dashboards still indicate a risk-on sentiment, it is less convincing than it was a few days ago. This is evident in the compression of the leading indicators (Dow/Gold, S&P/Vix and S&P/Nasdaq). The S&P 500 is positive and appears to have the potential to reach the 6,000 level. Bonds remain weak, continuing to revolve around the 50-day average in an attempt to maintain the bullish trend that began at the start of the year.

In terms of macroeconomics, today’s data includes Japan’s GDP and the Eurozone trade balance. However, data on new residential construction, import price trends and the preliminary May reading of the University of Michigan’s consumer confidence index will come from US.

Our forecast analysis indicates a moderately positive day for equities, though there is more uncertainty surrounding Europe. There are still positive indications for the commodity index, while precious metals are showing signs of a wait-and-see approach. Bonds remained weak, while the dollar showed signs of recovery. Volatility remained unchanged.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 16 May 2025 - 7:37 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.