More doubts than certainties in financial markets. Tariffs weighed and PCE awaited

The week ended with more doubts than certainties for the financial markets, with US equities and the technology sector in particular suffering. Tariffs once again became the main market mover ahead of data on consumer spending and the PCE price index. Equities remain weak while the rally in bonds is likely to continue.

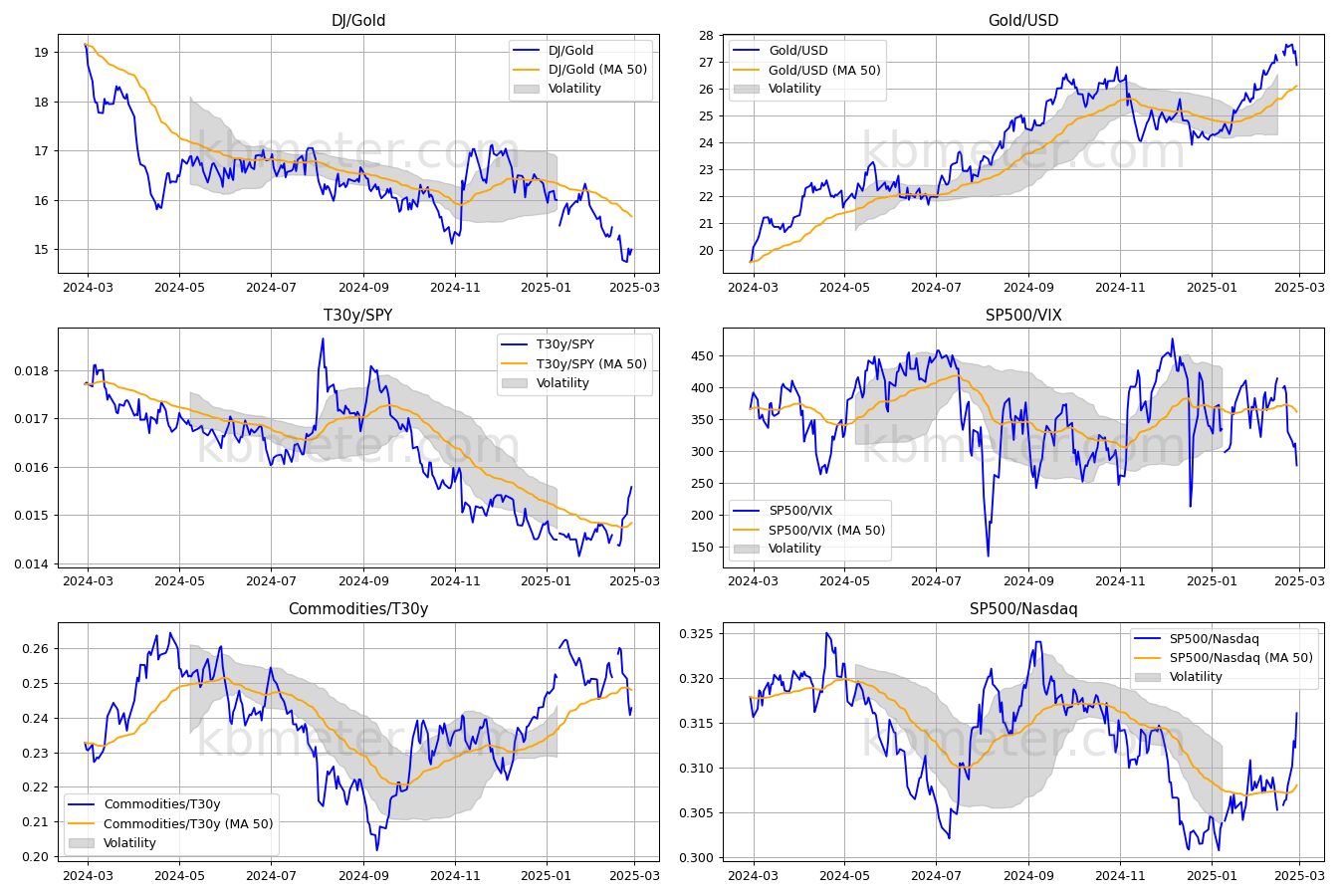

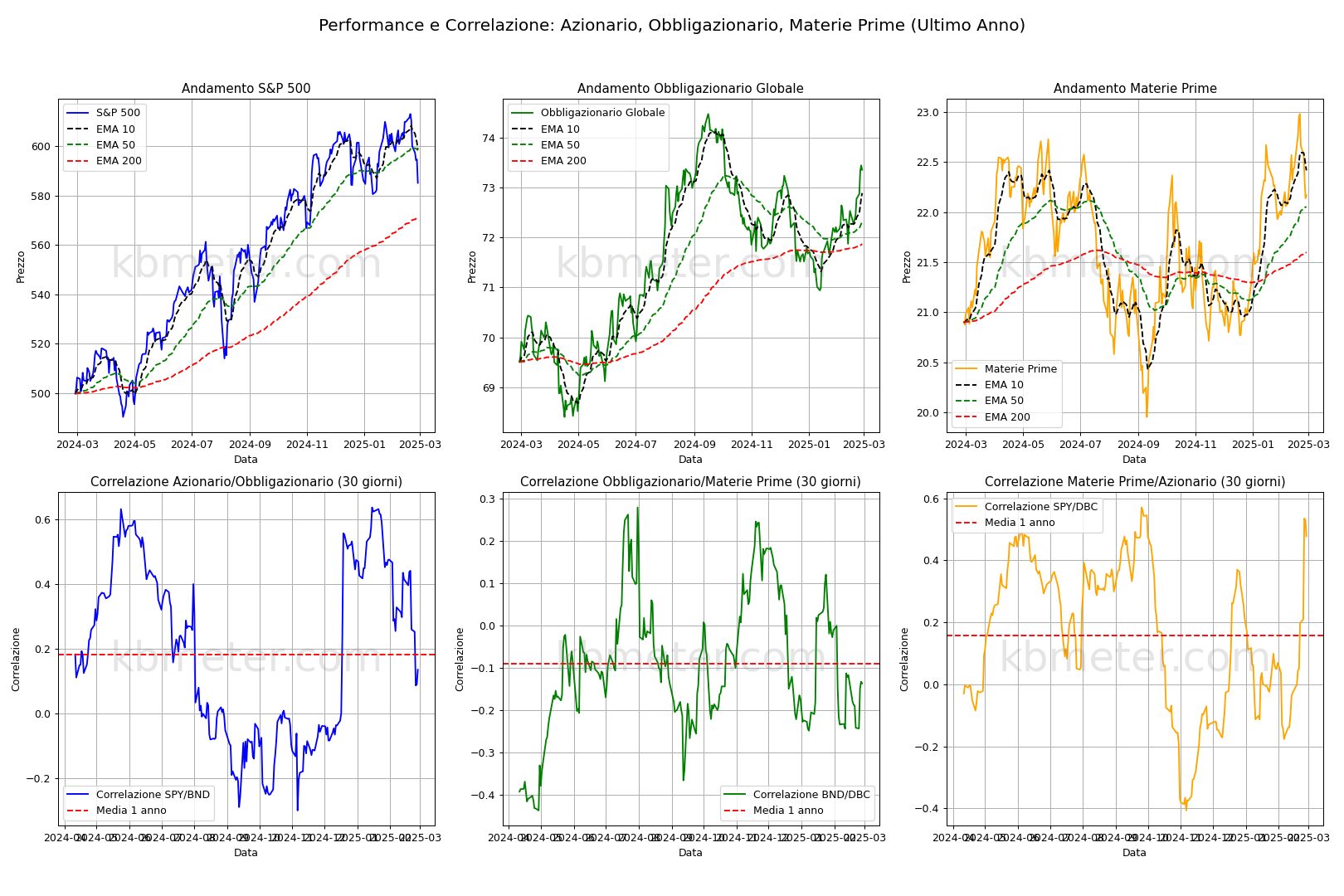

Our intermarket dashboards show the new trends that developed during the week. In the charts on the left we see the rise in the ratio of the S&P500 to the Nasdaq and the opposite movement in the ratio of the S&P500 to the VIX. Taken together, these two indicators signal a reduction in investor risk appetite. It is also worth noting that gold’s rally against the dollar has slowed. In the charts to the right, we can see the sharp slowdown in the S&P500; the correlation between equities and commodities has risen, reaching its highest level since last November. On the other hand, the rally in bonds continues.

On the macroeconomic front, investors are currently awaiting with some concern the data on the PCE price index, the inflation index most closely monitored by the FED. The data on personal spending, an indicator of the resilience of consumption, will also be important. In Europe, all eyes will be on Germany for February’s inflation and retail sales figures.

Our forecast analysis continues to point to a difficult period for equities, especially in the US. The situation remains mixed for commodities and slightly positive for the dollar (although the general tone is one of expectation). For bonds, the music is unchanged: yields are still expected to fall. Slight increase in volatility.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 28 February 2025 - 7:28 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.