Markets on edge ahead of the Fed

Financial markets are showing some nerves on the long-awaited day of the Fed meeting, which is expected to mark the return of the central bank’s rate-cutting cycle. A 25-basis-point reduction is taken for granted, but investors are wondering about what comes next: just one more move between now and year-end? Will the decision be made by majority or unanimously? In the meantime, equities remain tilted to the upside but with weaker momentum, bonds are in wait-and-see mode, and gold continues to rise, though overbought signals are starting to flash.

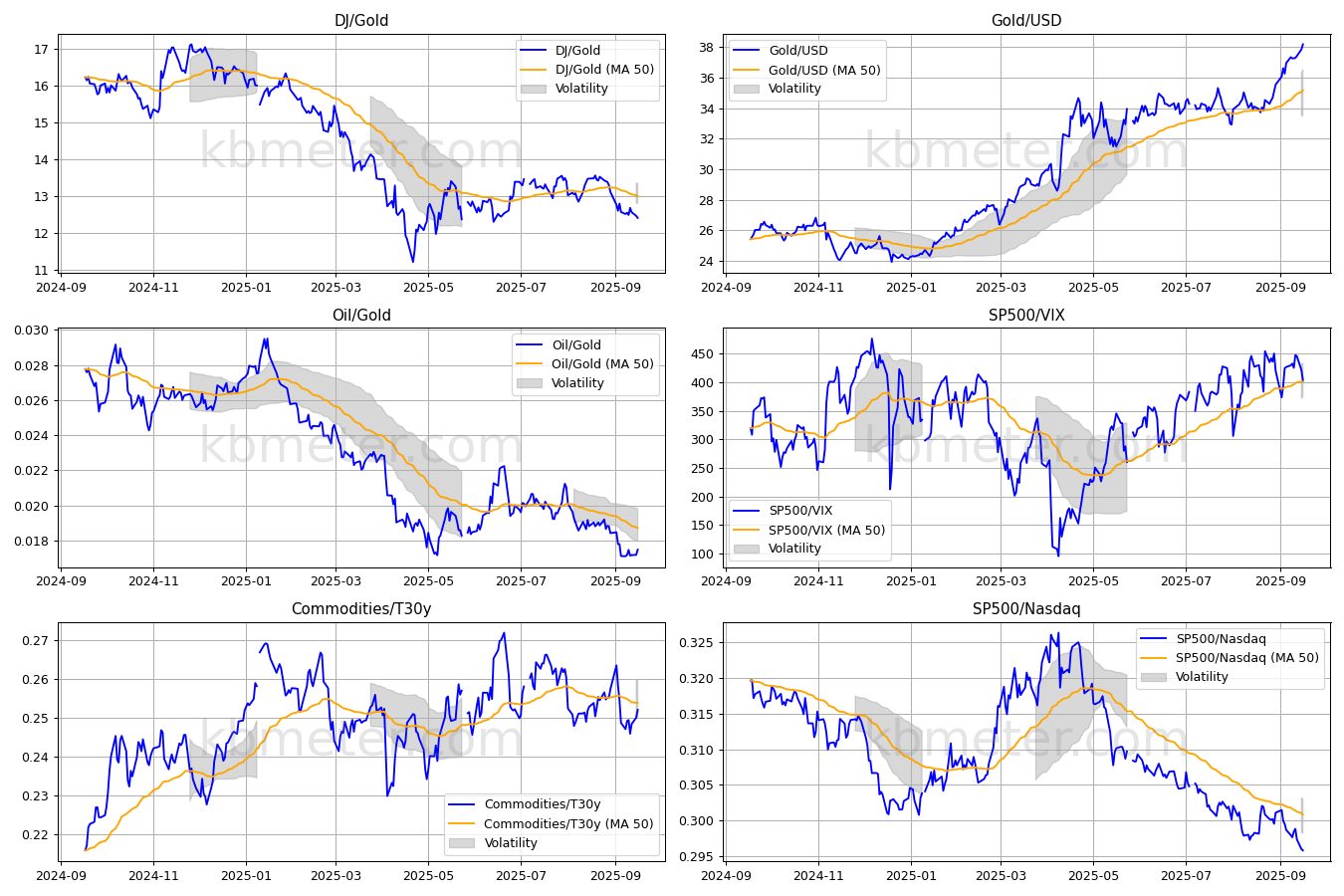

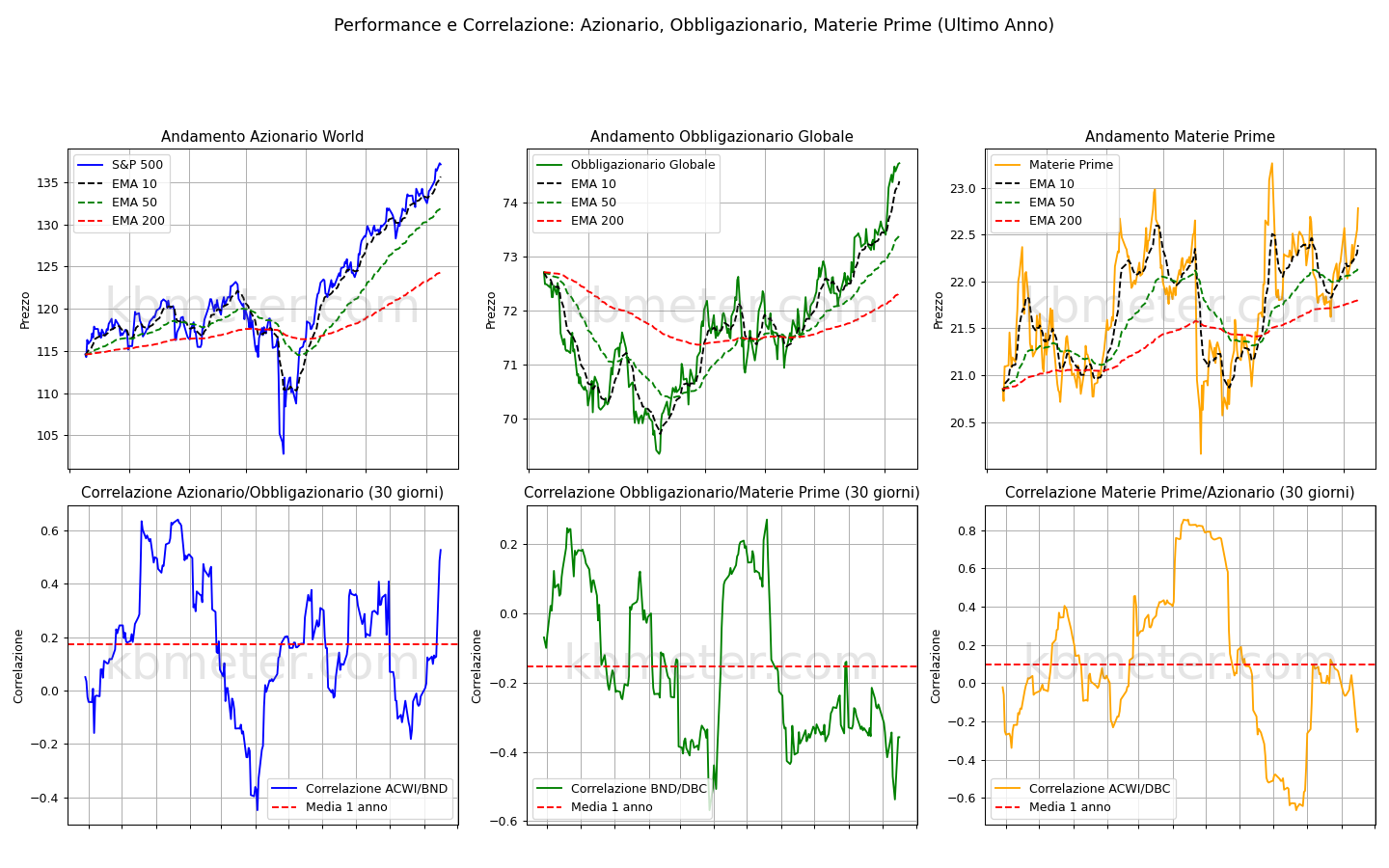

Everything remains stable on our intermarket dashboards. Equities and bonds are still biased to the upside, while awaiting potential surprises on the monetary policy front. Gold continues to show strength, and the S&P500-to-VIX ratio has returned to its annual moving average—signals of some tension ahead of tonight’s key event.

On the macroeconomic front, needless to say, today is Fed day, an event that has been at the center of market attention for many days. But we should also highlight the Bank of Canada meeting (with a rate cut expected here as well), UK inflation data (ahead of the BoE meeting), and Japan’s export figures.

Our forward-looking analyses point to another positive day for U.S. equities, albeit with much less momentum compared to recent sessions. European markets continue to show signs of uncertainty, while signals remain positive in Asia. Bonds remain in a wait-and-see mode. Equity volatility is ticking slightly higher. The dollar is still seen as weak, and gold remains in overbought territory.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 17 September 2025 - 7:22 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.