Markets Hold Neutral Bias as Tech Remains the Weak Link, Strong Dollar Weighs on Emerging Equities

From Strong Link to Weak Link. The technology sector continues to dominate market attention—for better or worse—this week. With the PCE inflation data coming in broadly in line with expectations, investors are once again questioning the actual profitability of massive AI-related investments. In this context, reports suggesting that OpenAI’s IPO could be postponed until 2027 have done little to ease concerns. The S&P 500/Nasdaq ratio remains firmly above its medium-term moving average, while the strengthening U.S. dollar is beginning to weigh on emerging equity markets. Overall market sentiment remains neutral, with futures pointing to a weaker open for U.S. markets and a slightly negative start for European equities.

Market Weather Map

June 26, 2026

US Equities

Eu Equities

Asia Equities

Commodities

Bonds

Dollar Index

Technology

Gold

Oil

Crypto

Market Summary

Do you want to see the score details for all assets monitored by KBMeter?

Try free for 14 days →Financial markets sentiment

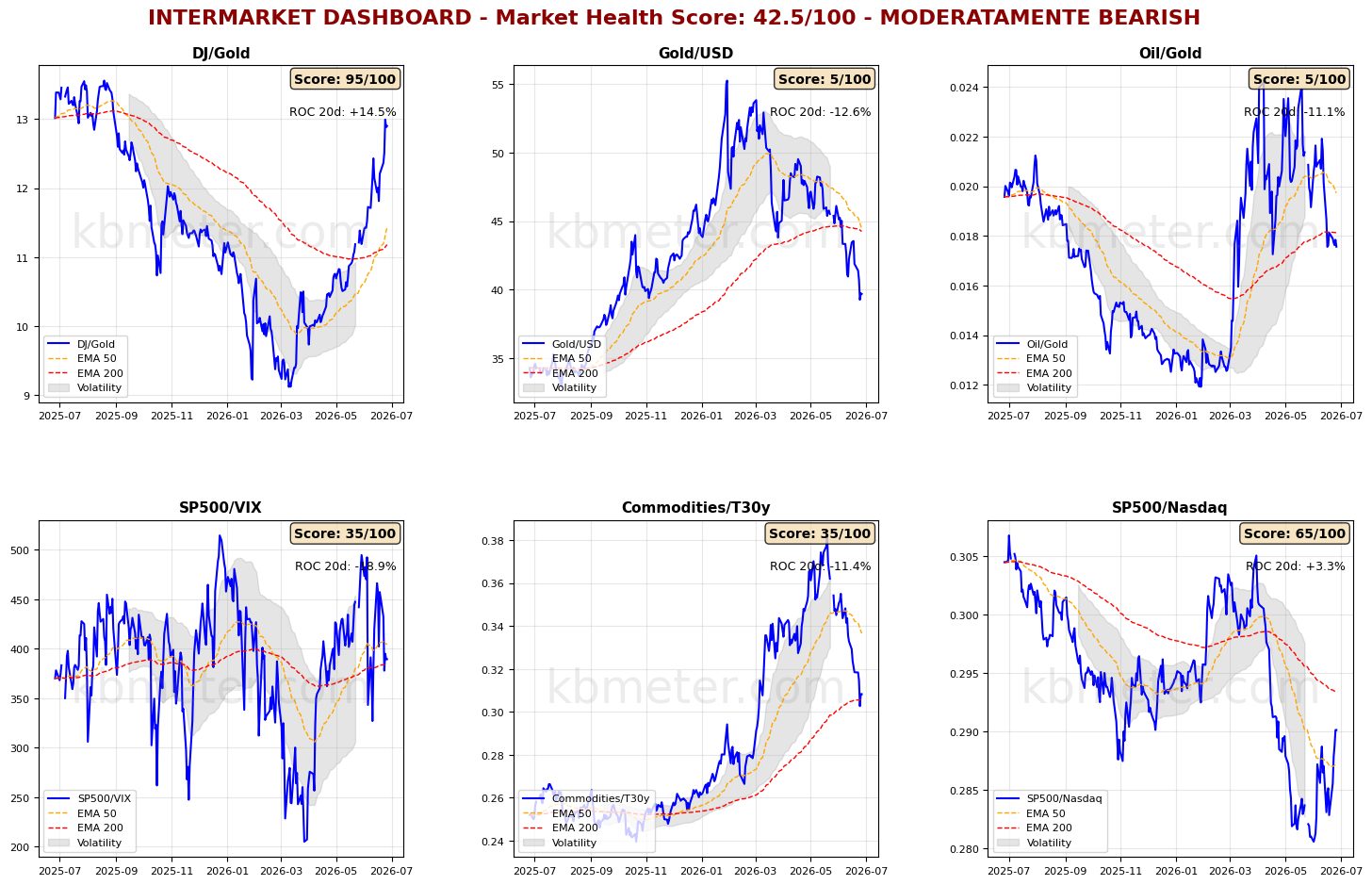

Financial markets are displaying a neutral sentiment today. Intermarket analysis points to a Market Health Score of 42/100, indicating a moderately negative environment.

There are few meaningful changes across our intermarket dashboards, with conditions remaining broadly consistent with yesterday’s assessment. The Commodities/Bonds ratio continues to hover around its long-term moving average, as the latest PCE data failed to fully resolve investor uncertainty regarding inflation expectations and the Federal Reserve’s next policy moves. The same uncertainty surrounding U.S.-Iran negotiations continues to prevent further declines in the Oil/U.S. Dollar ratio, while risk appetite indicators remain in neutral territory.

One development worth monitoring is the continued recovery of the S&P 500/Nasdaq ratio, which is now firmly established above its medium-term moving average.

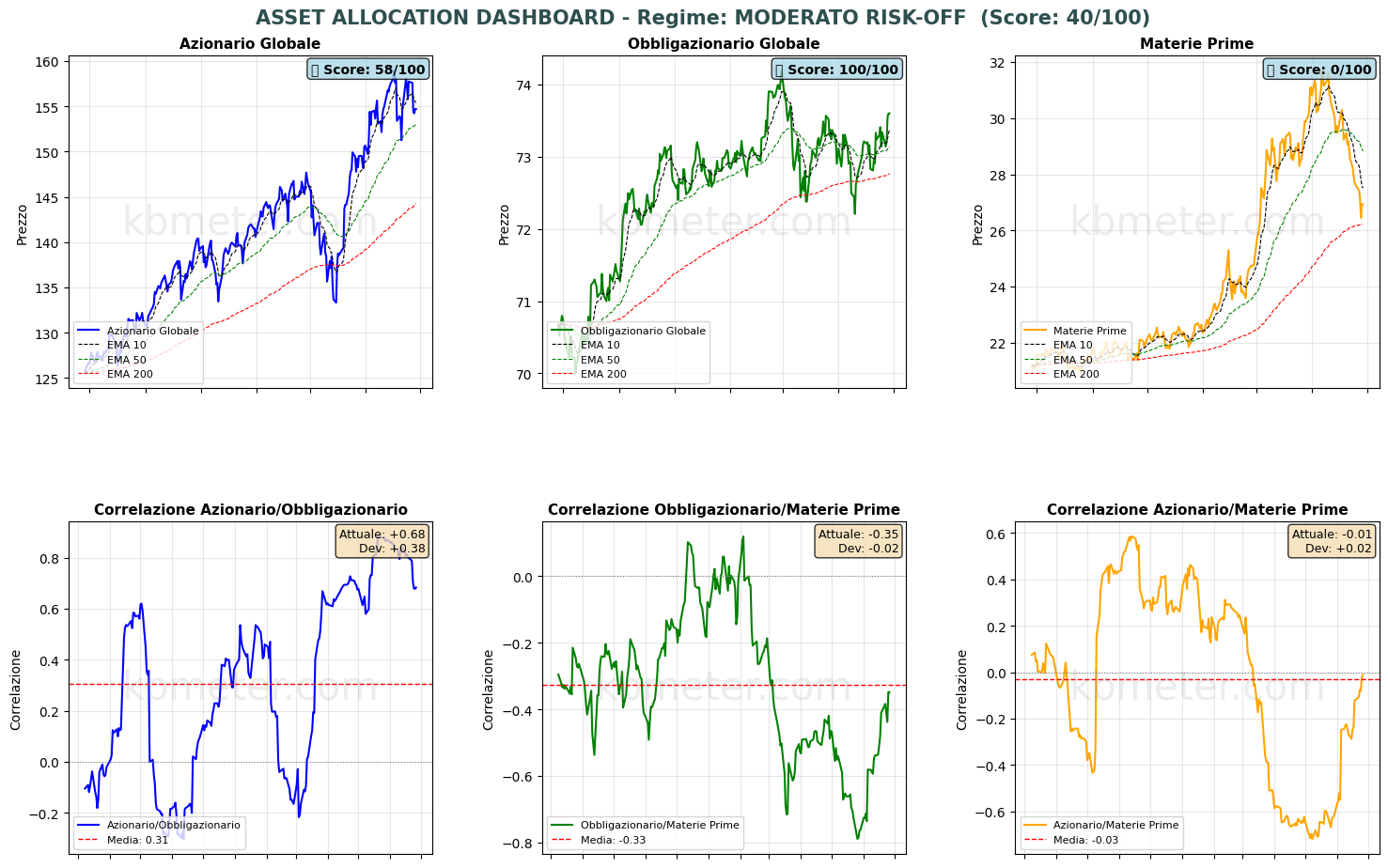

Across the major asset classes, market positioning remains largely unchanged. Commodities have so far failed in an initial attempt to break below their long-term moving average. Fixed income has moved back above its short-term moving average, while equities have lost some momentum and continue to trade between their short-term and medium-term moving averages.

Looking at our Market Weather Map and Health Scores, two related observations stand out. First, the U.S. dollar remains resilient following the PCE inflation release, which did not eliminate the possibility of another Fed rate hike. Second, on a weekly basis, some of the weakest Health Score performances are being recorded by South American and broader emerging equity markets. The persistence of a strong U.S. dollar is beginning to exert increasing pressure on emerging market equities and beyond.

Elsewhere, it is worth noting that both European equities and the technology sector currently have Health Scores below the 50-point threshold.

Global Futures – Pre-Market Sentiment

Futures Pre-Market: Global equity futures are pointing to a risk-off start to the session, with an average decline of 0.55%. U.S. futures are leading losses (-0.76%), European futures are modestly lower (-0.28%), while Asian futures are under the greatest pressure (-1.09%).

📊 Global Futures – Pre-Market Sentiment

- CSI 300: +1.46%

- IBEX 35 derived: +0.97%

- TecDAX derived: +0.46%

- Nikkei 225 derived: -3.26%

- US Tech 100 derived: -1.58%

- Hang Seng derived: -1.48%

Macroeconomic calendar

On the macroeconomic front, today’s calendar offers few major data releases. This afternoon, markets will focus on the final June reading of the University of Michigan U.S. Consumer Sentiment Index.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 26 June 2026 - 8:59 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.