Markets Eye Value Rotation as Fed Minutes Loom, Bonds Come Under Renewed Pressure

Financial markets are attempting to maintain a risk-on stance despite renewed tensions in the Gulf, heightened volatility in the technology sector, and anticipation surrounding the release of the Federal Reserve’s meeting minutes. Our intermarket analysis and proprietary Health Scores confirm the ongoing rotation toward value stocks, with the Dow posting the strongest daily improvement in its score, while the S&P 500/Nasdaq ratio is approaching a key resistance area. Meanwhile, inflation and interest rate expectations are also beginning to shift, as the bond market loses momentum and the U.S. dollar remains strong. Against this backdrop, gold’s recent recovery still requires further confirmation. Futures point to a flat opening for U.S. markets and a positive start for European equities.

Market Weather Map

July 8, 2026

US Equities

Eu Equities

Asia Equities

Commodities

Bonds

Dollar Index

Technology

Gold

Oil

Crypto

Market Summary

Do you want to see the score details for all assets monitored by KBMeter?

Try free for 14 days →Financial markets sentiment

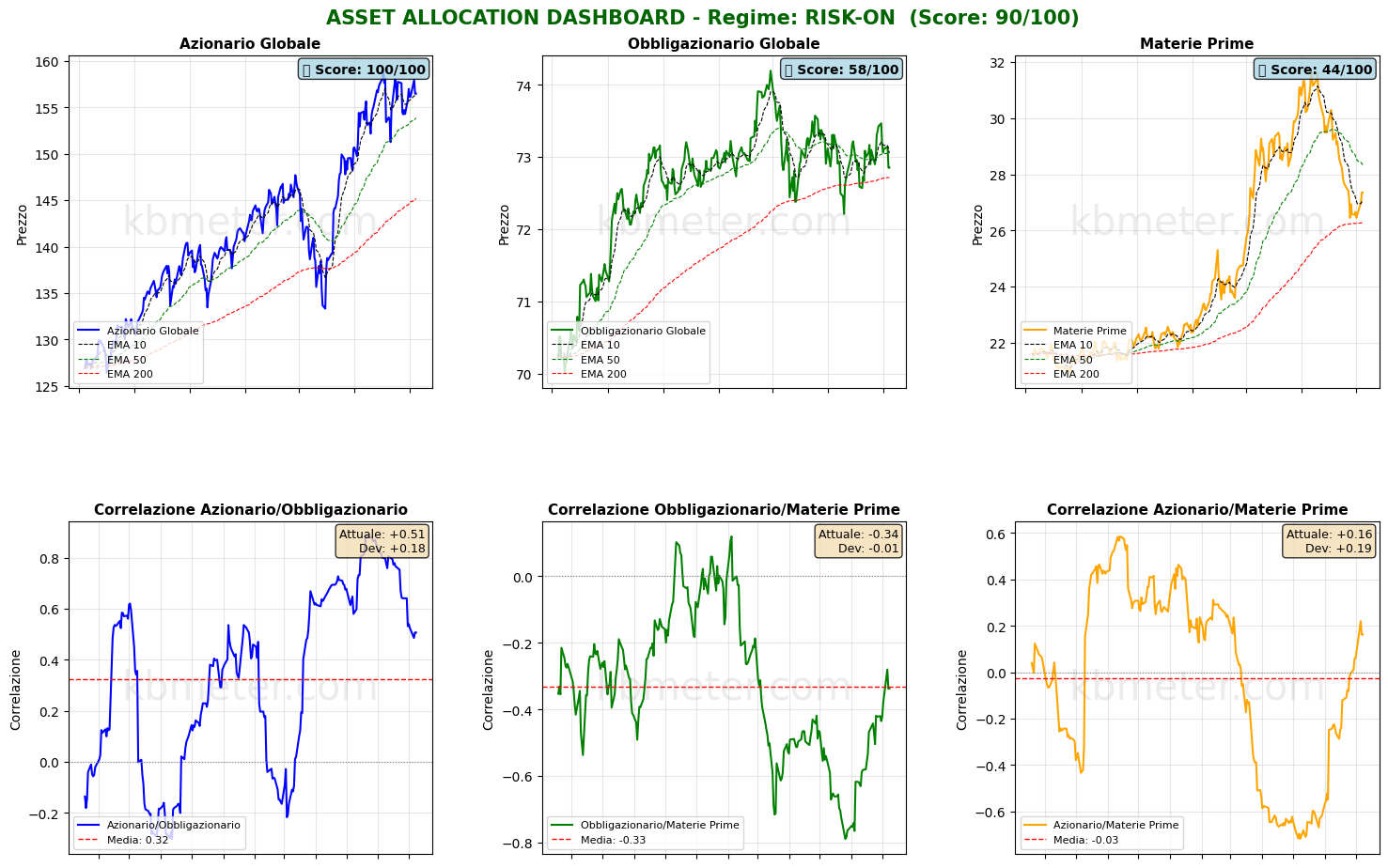

Financial markets are displaying a neutral to mildly positive sentiment today. Our intermarket analysis shows a Market Health Score of 58/100, indicating a moderately positive environment. The impact of renewed tensions in the Gulf is being reflected not only in oil prices but also in government bond prices and the strength of the U.S. dollar. With no major macroeconomic releases scheduled, markets awaiting the Fed minutes, and the technology sector remaining highly volatile, overall sentiment continues to favor a risk-on environment, albeit with increasing caution.

Our intermarket dashboards highlight the sharp move in the Oil/Gold ratio and, more importantly, the strong rebound in the Commodities/Bonds ratio. Another key indicator worth monitoring is the S&P 500/Nasdaq ratio. It has returned to April levels, its short-term trend remains bullish, and it is now approaching a significant resistance level represented by its long-term moving average.

Across the major asset classes, equities continue to trade within a solid uptrend, although momentum has declined considerably compared with a few weeks ago. Fixed income, on the other hand, deserves close attention. Bonds are now moving sideways and are trading below both their 10-day and 50-day moving averages, suggesting that inflation and interest rate expectations have started to re-emerge as important market drivers. This view is further supported by commodities, which successfully held above their long-term moving average before staging a rebound.

Looking at our proprietary Health Scores, several noteworthy developments stand out. Gold continues to recover and ranks among the top ten assets in terms of positive seven-day directional change. Commodities have also regained the neutral threshold of 50. The U.S. dollar remains notably strong, while equities continue to trade above the neutrality level.

Within equities, the rotation toward value remains clearly in place, with the Dow recording the strongest one-day improvement in our Health Score rankings. In fixed income, our statistics indicate a broad slowdown in momentum across the asset class.

Global Futures – Pre-Market Sentiment

Pre-Market Futures: Global equity futures indicate a moderately risk-on sentiment, with an average gain of +0.09%. U.S. futures are marginally negative (-0.03%), European futures are slightly positive (+0.02%), and Asian markets are posting modest gains (+0.46%).

📊 Global Futures – Pre-Market Sentiment

- Hang Seng derived: +2.32%

- TecDAX derived: +1.32%

- Nikkei 225 derived: +0.21%

- CSI 300: -1.15%

- FTSE MIB derived: -0.95%

- DAX derived: -0.10%

Macroeconomic calendar

The macroeconomic calendar offers few major catalysts today. The key event will be the release of the minutes from the latest Federal Reserve meeting, which represents the market’s primary opportunity to gain further insight into the central bank’s current stance on interest rates.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 8 July 2026 - 7:42 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.