Markets Enter Q3 With Strong Dollar as Focus Shifts to U.S. Jobs Data and Eurozone Inflation

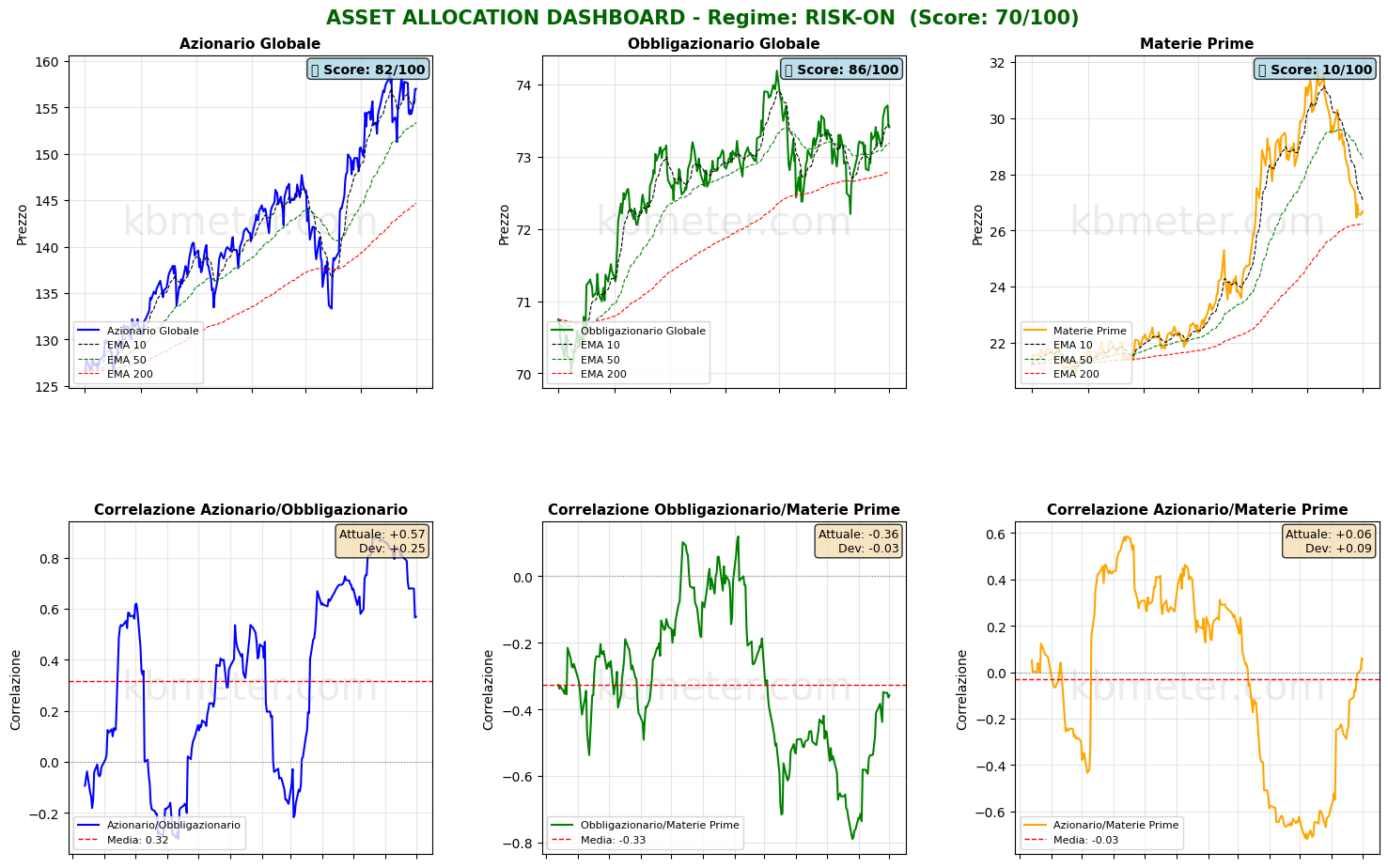

Financial markets enter the third quarter of 2026 with sentiment still broadly neutral, although there are some renewed signs of risk-on positioning. Investors’ attention is now focused on the U.S. labor market. Following yesterday’s stronger-than-expected JOLTS job openings data, today’s ADP employment report and tomorrow’s official U.S. Department of Labor payrolls report should provide further insight into the health of the U.S. economy and the Federal Reserve’s next policy moves.

Yesterday, bond markets lost momentum as expectations of interest rates remaining unchanged—or even moving higher—gained traction once again. Meanwhile, the U.S. dollar continues to strengthen, putting pressure on the Japanese yen, gold, commodities, and emerging equity markets. Equity futures point to a slightly weaker open in both the United States and Europe.

Market Weather Map

July 1, 2026

US Equities

Eu Equities

Asia Equities

Commodities

Bonds

Dollar Index

Technology

Gold

Oil

Crypto

Market Summary

Do you want to see the score details for all assets monitored by KBMeter?

Try free for 14 days →Financial markets sentiment

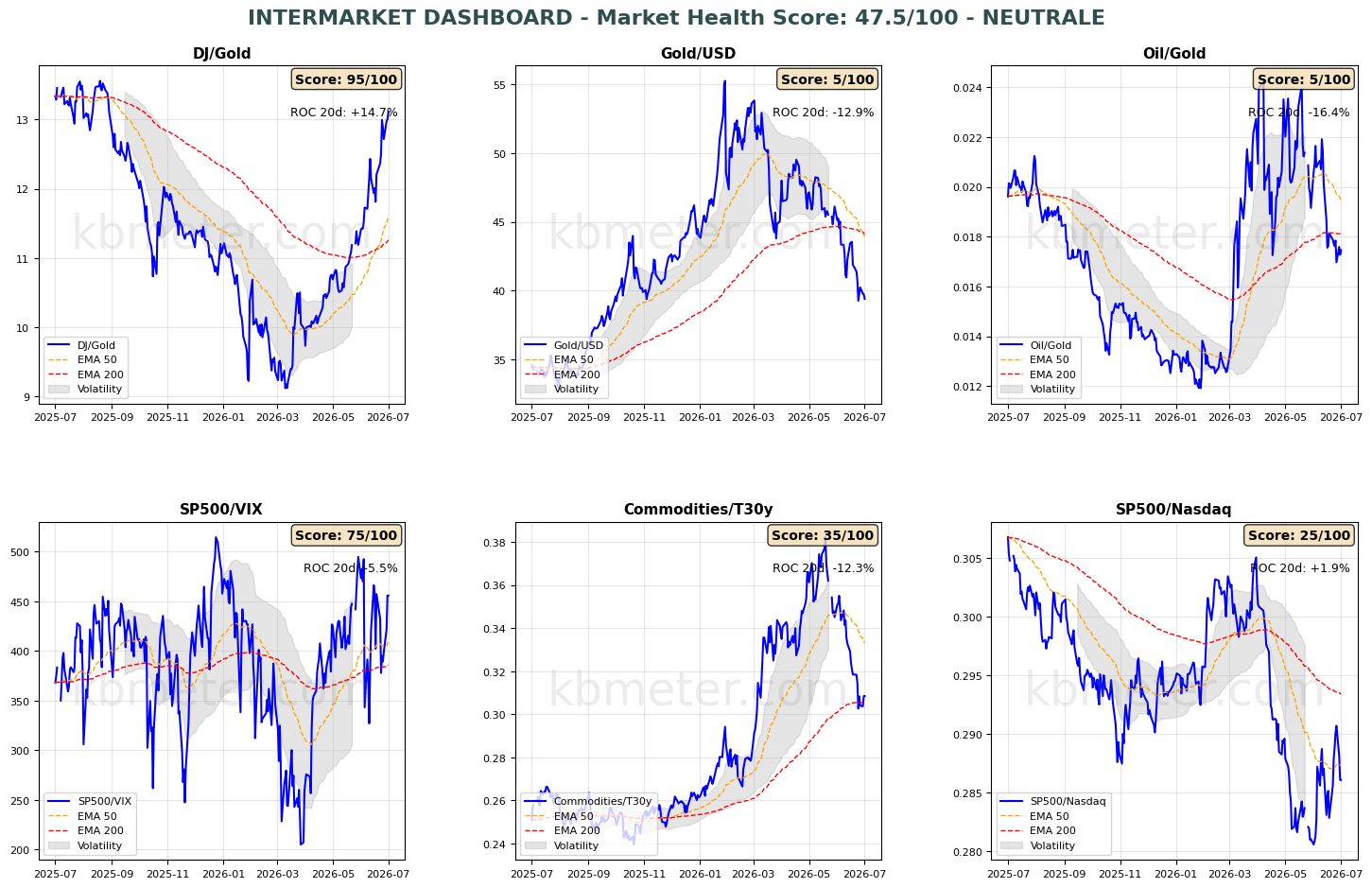

Financial markets are displaying a neutral to mildly positive sentiment today. Intermarket analysis shows a Market Health Score of 48/100, indicating a neutral market environment.

Our intermarket dashboards begin July with a bearish signal developing in the Gold/U.S. Dollar ratio. Weakness in bullion, combined with continued strength in the greenback, is bringing the 50-day and 200-day moving averages closer together. At the same time, risk-on signals are attempting to consolidate, with the S&P 500/VIX ratio recovering to late-May levels, while the S&P 500/Nasdaq ratio has slipped back below its medium-term moving average.

Positive U.S. labor market data—particularly May’s stronger-than-expected job openings—and Eurozone inflation figures have weighed on fixed income markets. The Commodities/Bonds ratio has moved back above its long-term moving average and remains above the levels seen before the Gulf crisis.

Global equities continue to trade above their three main moving averages, while bonds are undergoing a pullback; however, both asset classes remain in short-term uptrends. Commodities are currently finding support around their 200-day moving average.

Our Financial Markets Weather Map shows a strengthening positive directional signal for European equities, with the score approaching the 60-point mark. The U.S. dollar remains firm, continuing to weigh on gold, commodities, and both emerging and Asian equity markets.

Global Futures – Pre-Market Sentiment

Pre-Market Futures: Global equity futures point to a moderately risk-off tone (average -0.04%), with U.S. futures slightly lower (-0.33%), European futures marginally negative (-0.04%), and Asian futures modestly higher (+0.35%).

📊 Global Futures – Pre-Market Sentiment

- CSI 300: +1.37%

- FTSE MIB derived: +1.00%

- IBEX 35 derived: +0.27%

- TecDAX derived: -1.08%

- Nikkei 225 derived: -0.42%

- US 500 derived: -0.37%

Intermarket details

Macroeconomic calendar

On the macroeconomic front, today’s calendar includes the final June 2026 PMI surveys, the preliminary estimate of June Eurozone inflation (following yesterday’s releases from the region’s major economies), the monthly U.S. ADP employment report, and the June ISM Manufacturing Index. Markets are also awaiting one of the first public appearances by the Federal Reserve Chair.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 1 July 2026 - 7:36 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.