Markets breathe a sigh of relief as US tit-for-tat tariffs postponed to April

The announcement of reciprocal tariffs did not do too much damage on the stock markets. Perhaps mindful of the reactions following the tariffs imposed on Canada and Mexico, the Trump administration postponed their implementation until April, with ample room for negotiation with partners. Financial markets are drawing breath and heading into a day that, on the face of it, seems to be quiet.

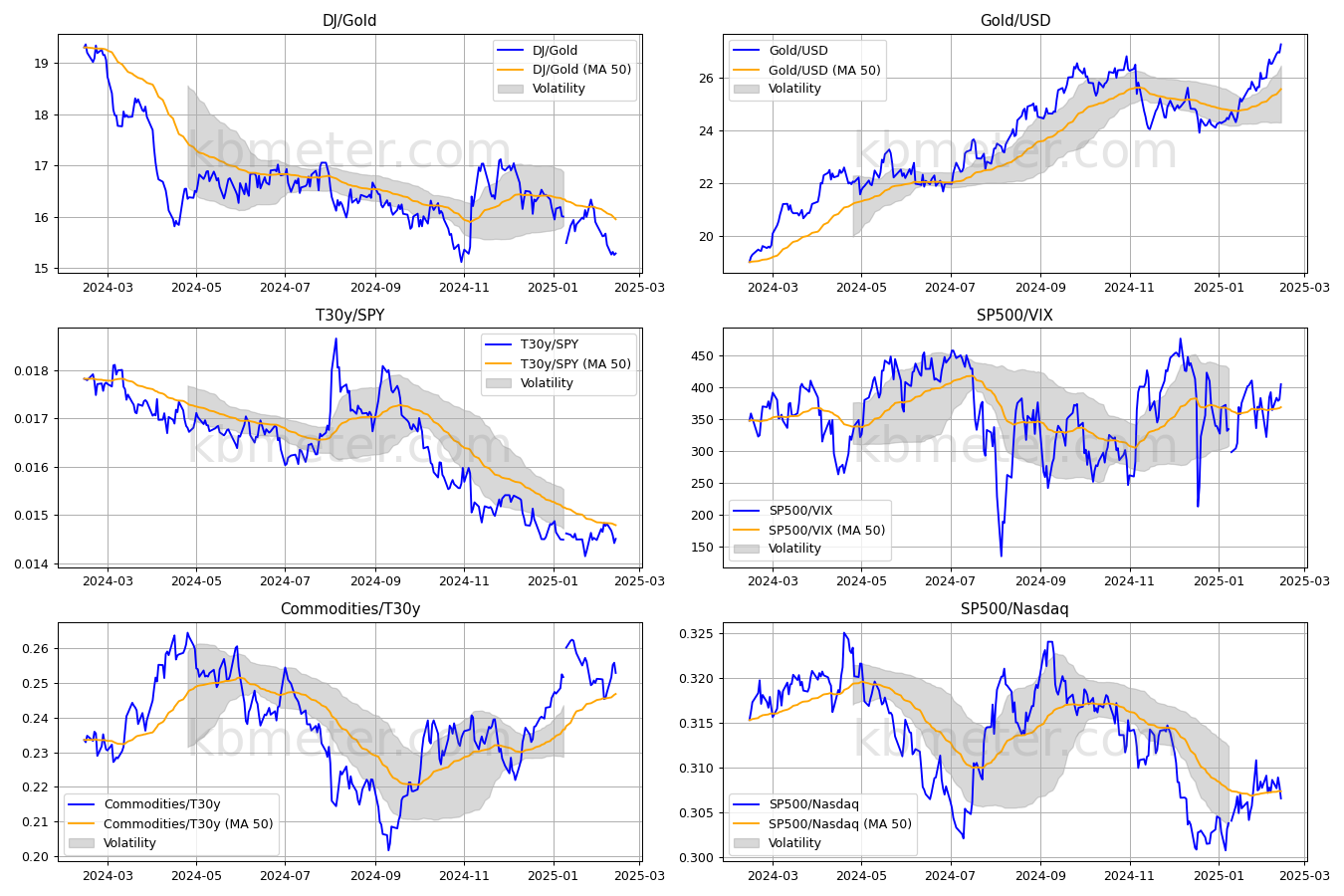

Looking at the intermarket dashboards, we can only observe how the trend in equities is intact in its medium/long-term bullish setting, while bonds will once again try the assault on dynamic resistance. Gold’s strong phase continues, while the 30-year yield ratio to the S&P500, despite the recent braking, continues to signal a risk-on situation in the market.

On the macroeconomic front, today sees the US retail sales figure for January, an indicator of the health of consumer spending that will test the resilience of domestic demand to persistent inflation. Also of interest are data on import prices and industrial production. From Europe, meanwhile, will come the second estimate of Q4 2024 growth in the Eurozone and the employment situation.

On the whole, our forecast analyses indicate a day without any upsurge, but buying signals on equities are increasing, while yields are retreating and the wait-and-see signal on gold and the dollar remains. Volatility down, signs of improvement for cryptocurrencies.

Already a subscriber? Login here

NOTES AND WARNINGS

Analysis automatically generated by kbmeter.com. Analysis date: 14 February 2025 - 7:31 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.