Gold Rises on Labor Data, but Scores Keeps Fed Hike Scenario Alive

The latest U.S. employment data has not been enough to completely dispel the possibility of a Federal Reserve rate hike before year-end. While gold—highly sensitive to interest rate expectations—showed signs of life following the release of labor market data that pointed to a stable, though not overheating, jobs market, our proprietary scores continue to signal underlying weakness. Likewise, our directional analysis of short-term U.S. Treasuries does not yet point to a dovish Fed, while the U.S. dollar remains firmly supported.

Volatility in the technology sector continues to be a key theme for financial markets, although overall market sentiment remains between neutral and mildly positive. The extended Independence Day weekend in the United States is making today’s session characteristically quiet, with few significant market-moving events on the calendar. Equity futures point to a positive opening for European markets.

Market Weather Map

July 3, 2026

US Equities

Eu Equities

Asia Equities

Commodities

Bonds

Dollar Index

Technology

Gold

Oil

Crypto

Market Summary

Do you want to see the score details for all assets monitored by KBMeter?

Try free for 14 days →Financial markets sentiment

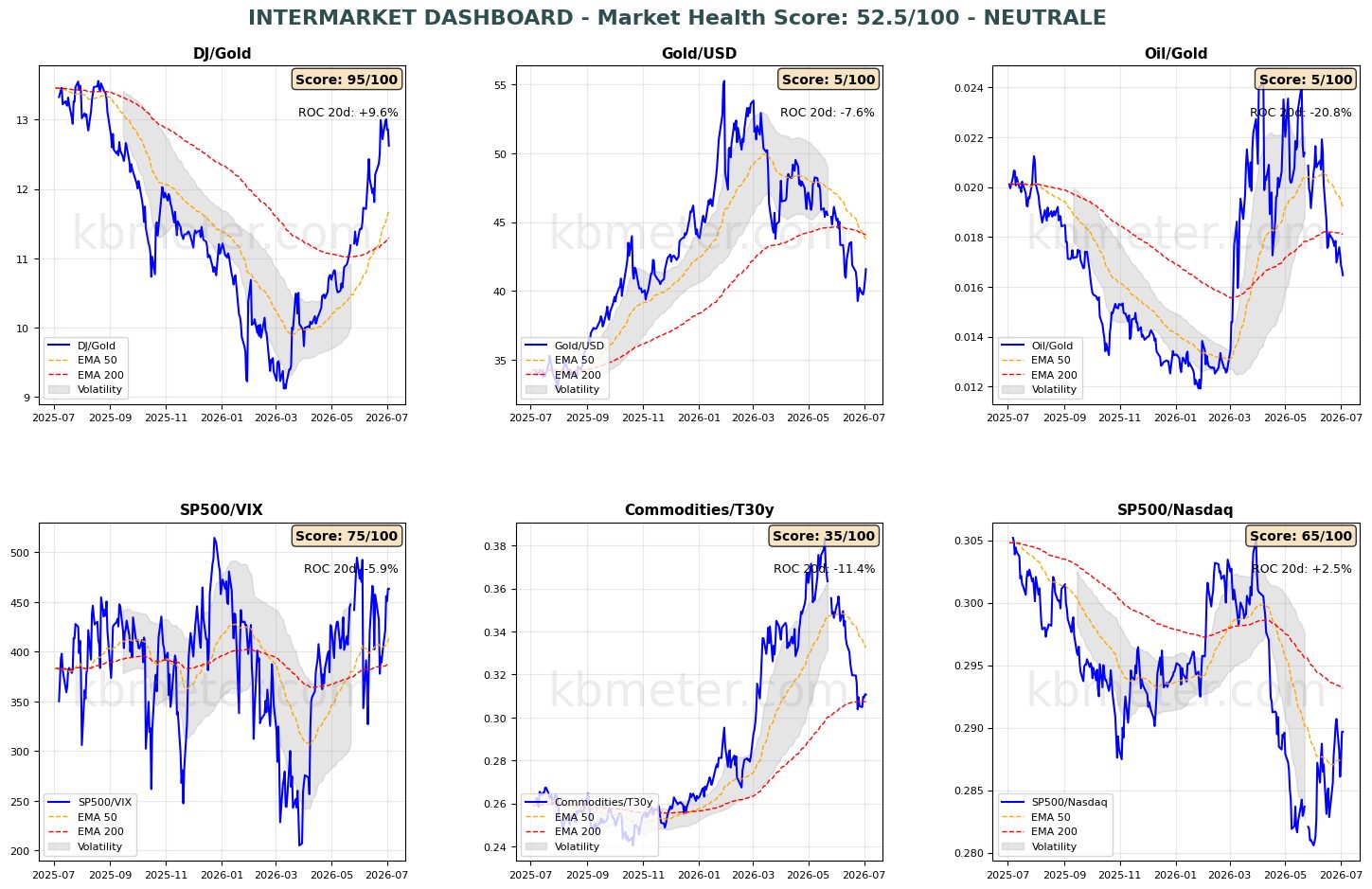

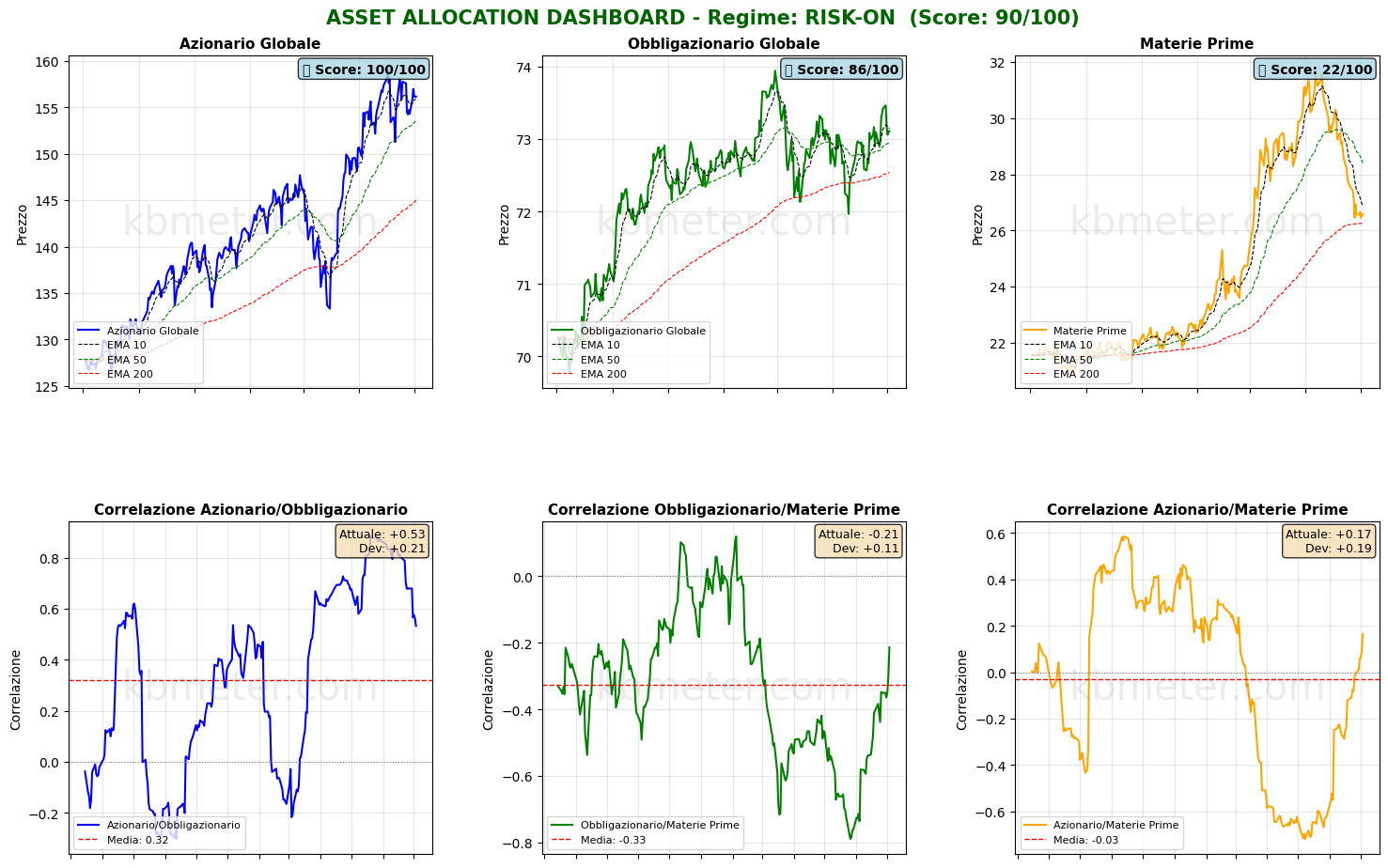

Financial markets are showing a neutral overall sentiment today. Our intermarket analysis currently assigns a Market Health Score of 52/100, indicating neutral conditions. U.S. labor market data, which came in weaker than expected, has reinforced expectations of a less aggressive Federal Reserve and generated two notable effects across our intermarket dashboards: gold has recovered against both the U.S. dollar and the Dow Jones, while the Oil/Gold ratio has accelerated to the downside. Risk appetite indicators remain in positive territory, although conviction is still limited, with the S&P 500/Nasdaq ratio continuing to reflect investors’ shifting sentiment toward the AI sector.

Global equities and bonds are showing a short-term loss of momentum but continue to trade comfortably above their 50-day moving averages. Meanwhile, commodities remain engaged in a test of long-term moving average support.

Our Market Weather Map continues to recommend caution on gold, which is still expected to weaken, while equity market scores remain broadly stable. The U.S. dollar continues to display underlying strength, reinforcing the view that inflation remains a central issue and one that investors have not yet fully priced in.

Looking at weekly changes, one development stands out and will be worth monitoring if confirmed over the coming days. Over the past seven days, short-term U.S. Treasuries rank among the ten weakest assets in our system in terms of directional strength, while short-term Eurozone government bonds rank among the ten strongest. In other words, our models continue to suggest that markets are still assigning some probability to additional Fed rate hikes, whereas a similar scenario appears to be largely ruled out for the European Central Bank.

Global Futures – Pre-Market Sentiment

Pre-Market Futures: Global equity futures indicate a risk-on tone, with an average gain of +0.53%. U.S. futures are modestly higher (+0.40%), European futures are stronger (+0.67%), while Asian futures are also slightly positive (+0.31%).

📊 Global Futures – Pre-Market Sentiment

- Nikkei 225 Derived: +1.94%

- FTSE MIB Derived: +1.60%

- TecDAX Derived: +1.33%

- CSI 300: -2.22%

- Mini MDAX Derived: +0.00%

- FTSE 100 Derived: +0.13%

Macroeconomic calendar

The macroeconomic calendar offers few catalysts today, partly due to the U.S. Independence Day holiday weekend. The main releases include the final June 2026 Composite PMI readings and May 2026 industrial production figures for Spain and France.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 3 July 2026 - 8:02 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.