Financial Markets: Tech-Led Risk Rally Extends as Middle East Risks Rise and Tariff Threats Re-Emerge

The week in financial markets continues under a risk-on backdrop, despite growing uncertainty surrounding the situation in the Middle East and the White House’s announcement of new 10% tariffs on goods imported from major trading partners. The technology sector continues to lead the equity rally, while the unusual combination of inflation expectations and the resilience of the U.S. economy is driving the U.S. dollar higher. Volatility remains moderate. Futures point to a slightly positive opening in Europe and a flat start in the United States.

Market Weather Map

June 3, 2026

US Equities

Eu Equities

Asia Equities

Commodities

Bonds

Dollar Index

Technology

Gold

Oil

Crypto

Market Summary

Do you want to see the score details for all assets monitored by KBMeter?

Try free for 14 days →Financial markets sentiment

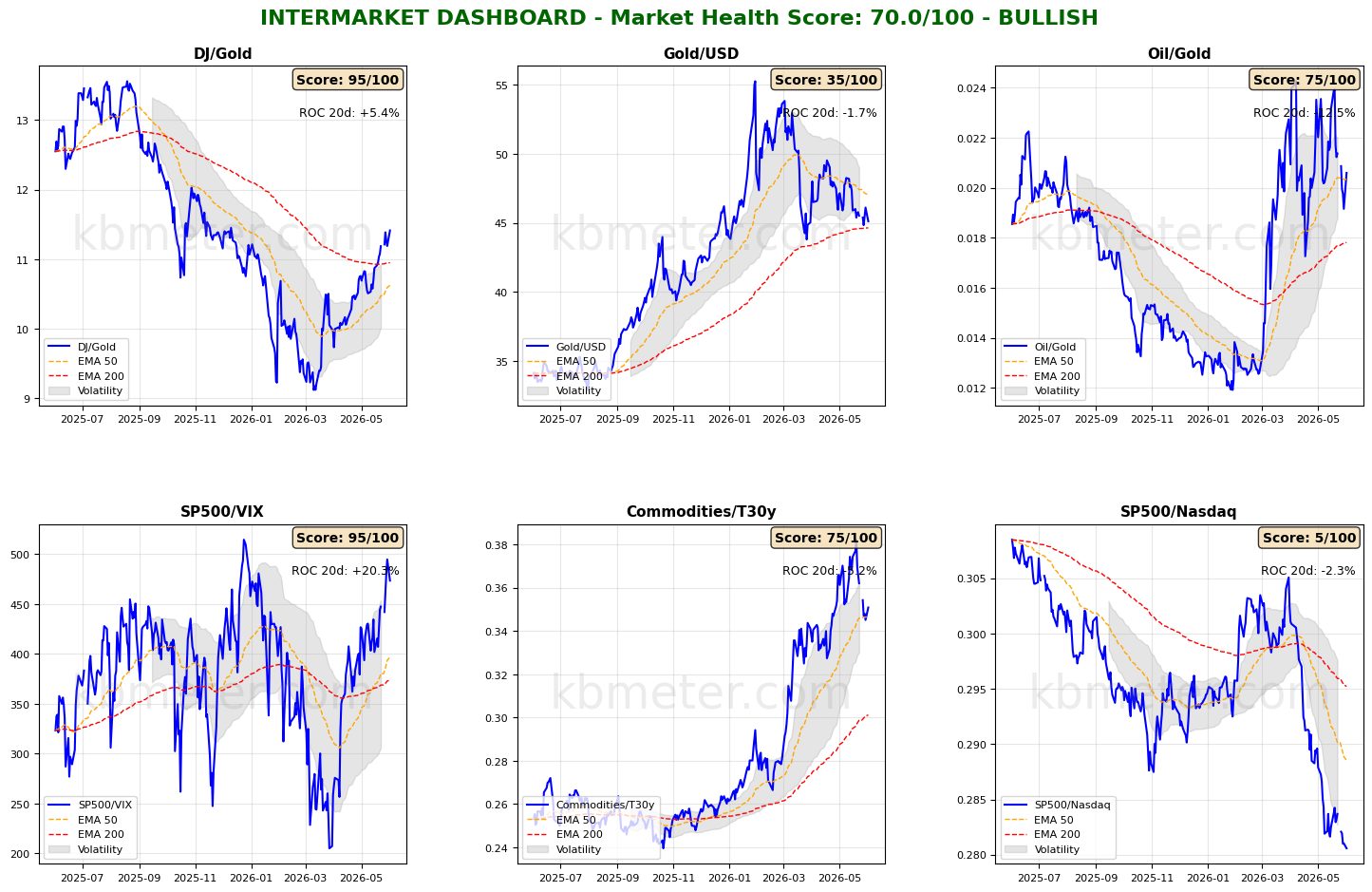

Financial markets are displaying a moderately positive sentiment today. Intermarket analysis shows a Market Health Score of 70/100 (positive). The expansion regime remains intact with a 55.6% probability, supported by a compressed High Yield spread of 2.72 and a positive yield curve at 0.47.

Three noteworthy developments emerge from our intermarket dashboards. First, the Commodities-to-Bonds ratio is rebounding from support provided by its medium-term moving average. Second, the Gold-to-Dollar ratio is, for the time being, holding above the critical support represented by its long-term moving average. Third, the combined reading of the Dow/Gold, S&P 500/VIX, and S&P 500/NASDAQ ratios continues to confirm the risk-on environment, while also highlighting that technology remains the primary driver of the rally.

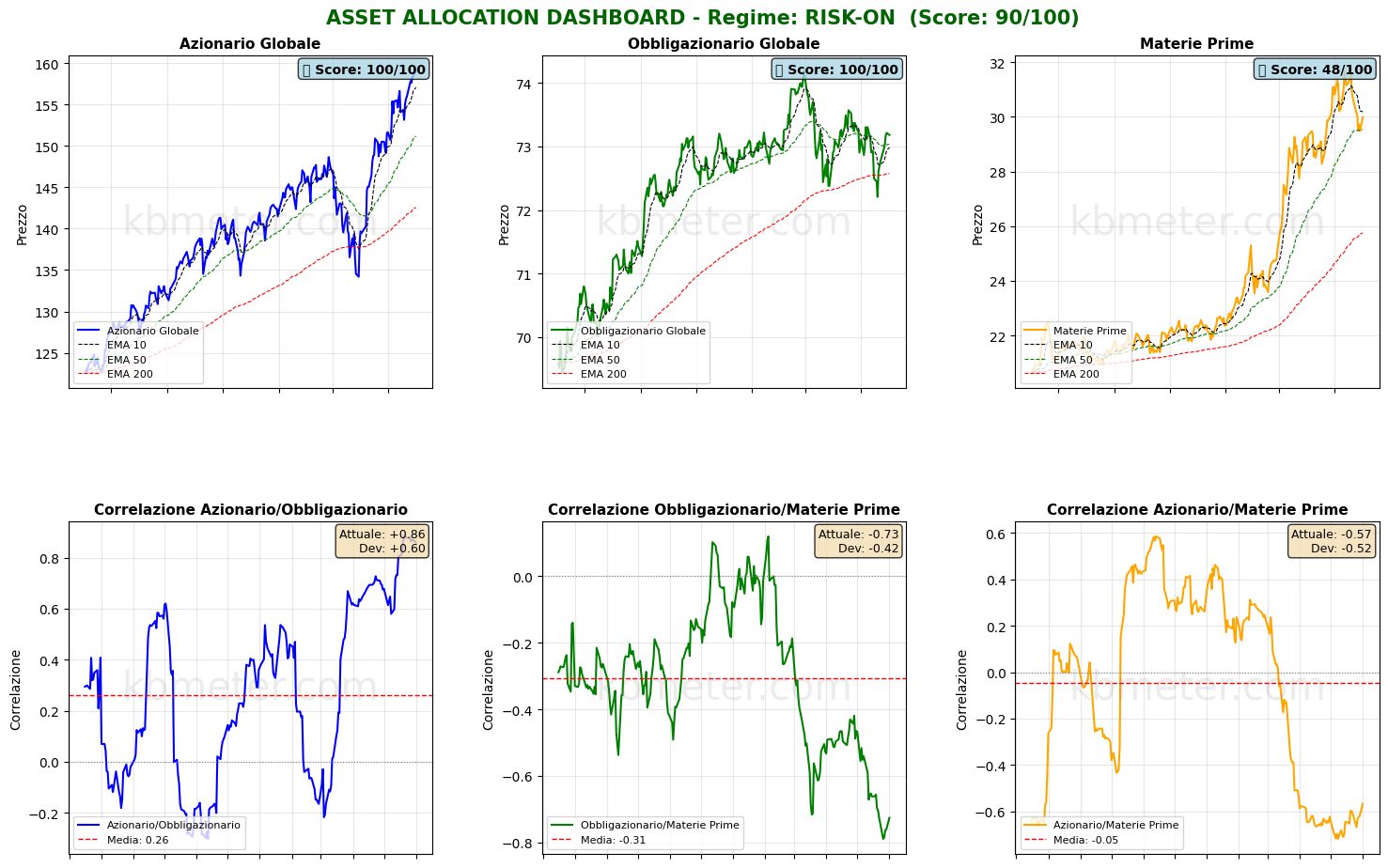

Regarding asset allocation, there are no major changes. In the short term, the equity rally appears uninterrupted; fixed income remains slightly above its 50-day moving average; and commodities are rebounding from support at their medium-term moving average. One additional point worth noting concerns correlations: the correlation between global equities and global bonds has reached +0.86 over the last thirty trading sessions, compared with a historical average of +0.26.

Our Market Weather Map continues to identify the U.S. dollar and the technology sector as the strongest-performing assets, while cryptocurrencies remain in a delicate position. Looking at our Health Scores, the biggest surprise this week within fixed income comes from emerging markets: local-currency and U.S.-dollar-denominated emerging-market bonds lead the weekly improvement rankings, with gains of +17.9 and +13.1 points respectively. In contrast, European bonds and European equity sectors have recorded the largest declines.

Global Futures – Pre-Market Sentiment

Pre-Market Futures. Global futures indicate a moderate risk-on sentiment (+0.25% on average), with U.S. futures slightly negative (-0.03%), European futures modestly positive (+0.24%), and Asian futures stronger (+0.66%).

📊 Global Futures – Pre-Market Sentiment

- Nikkei 225 derived: +1.82%

- FTSE MIB derived: +1.61%

- CSI 300: +1.52%

- Hang Seng derived: -1.37%

- IBEX 35 derived: -0.22%

- Euro Stoxx 50 derived: -0.15%

Intermarket details

| Ratio | Score | Value | vs 50-day average | 20-day Change | 50-day Change | Signal |

|---|---|---|---|---|---|---|

| S&P500/VIX | 99.8 | 48.17 | above | +15.66% | +92.18% | period highs |

| Gold/Dollar | 97.5 | 4.15 | below | −1.42% | +0.09% | period highs |

| Commodities/Bonds | 96.9 | 0.352 | above | −4.64% | +4.30% | period highs |

| Dow Jones/Gold | 19.3 | 11.43 | above | +5.54% | +14.61% | — |

| Oil/Gold | 9.1 | 0.021 | above | −11.30% | −2.91% | period lows |

| S&P500/Nasdaq | 0.0 | 1.018 | below | −4.60% | −8.76% | period lows |

Macroeconomic calendar

Today is one of the busiest days of the week from a macroeconomic perspective. In Europe, final May Composite PMI readings are being released this morning for Italy, Spain, France, Germany, and the Eurozone as a whole. In the U.S. afternoon session, attention will focus on two key data releases: the May ISM Services Index, expected to remain above the 50 threshold following Monday’s stronger-than-expected manufacturing reading, and the ADP Employment Report, which provides the first indication of labor market conditions ahead of Friday’s official employment data.

Later in the day, the Federal Reserve will publish its Beige Book, the qualitative assessment of economic conditions across its twelve districts, which may help shape expectations for the tone of the next FOMC meeting. The OECD will also release its updated economic forecasts.

On the earnings front, investors will be closely watching Broadcom’s results, which have the potential to be a significant market mover for the technology sector.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 3 June 2026 - 7:34 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.