Awaiting new US inflation data, stock markets take a breather

Financial markets appreciate the somewhat softer line taken by the Trump administration in recent days on the upcoming tit-for-tat tariffs. The rally in equities continues, while US yields pause to wait for more on inflation with next Friday’s PCE data.

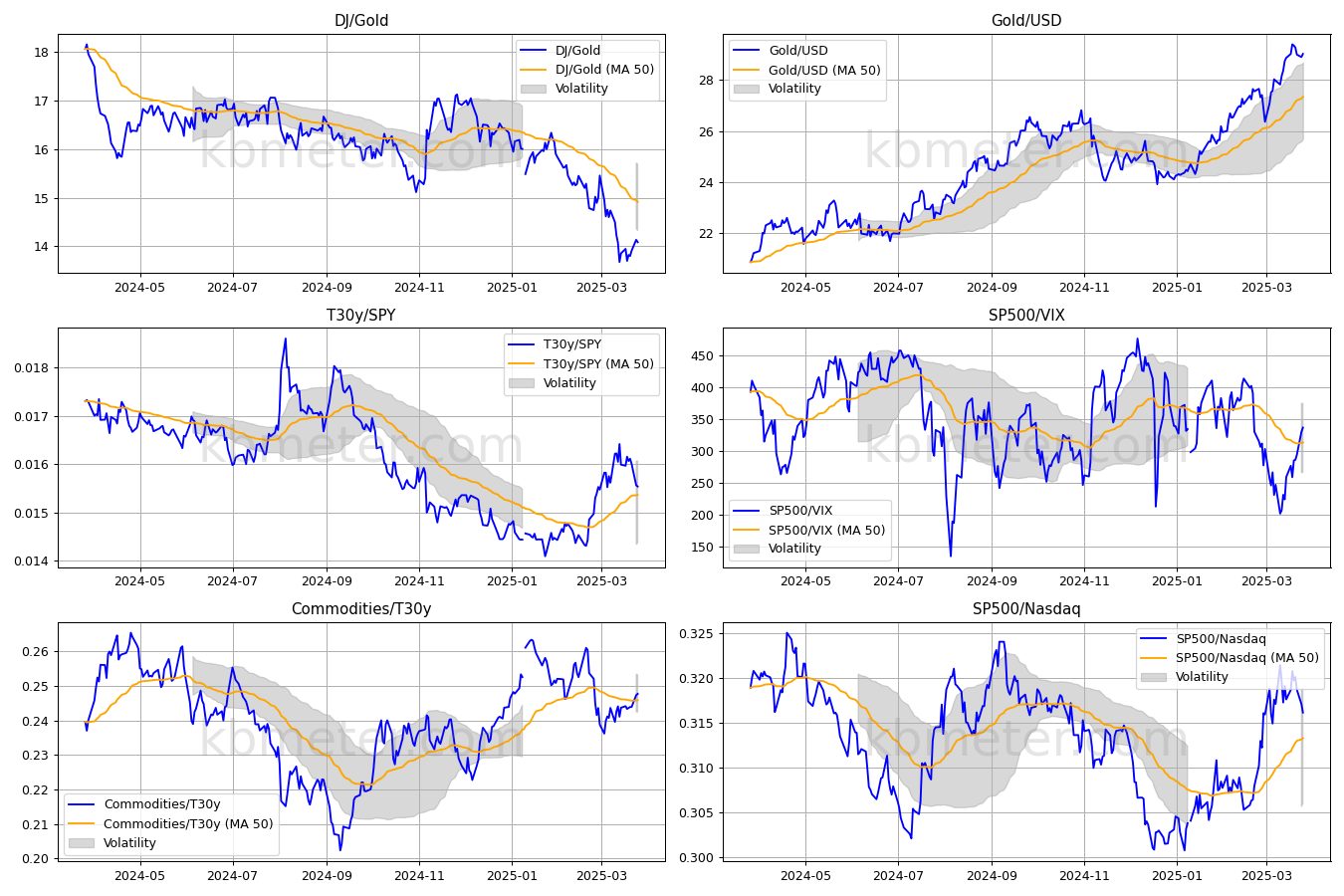

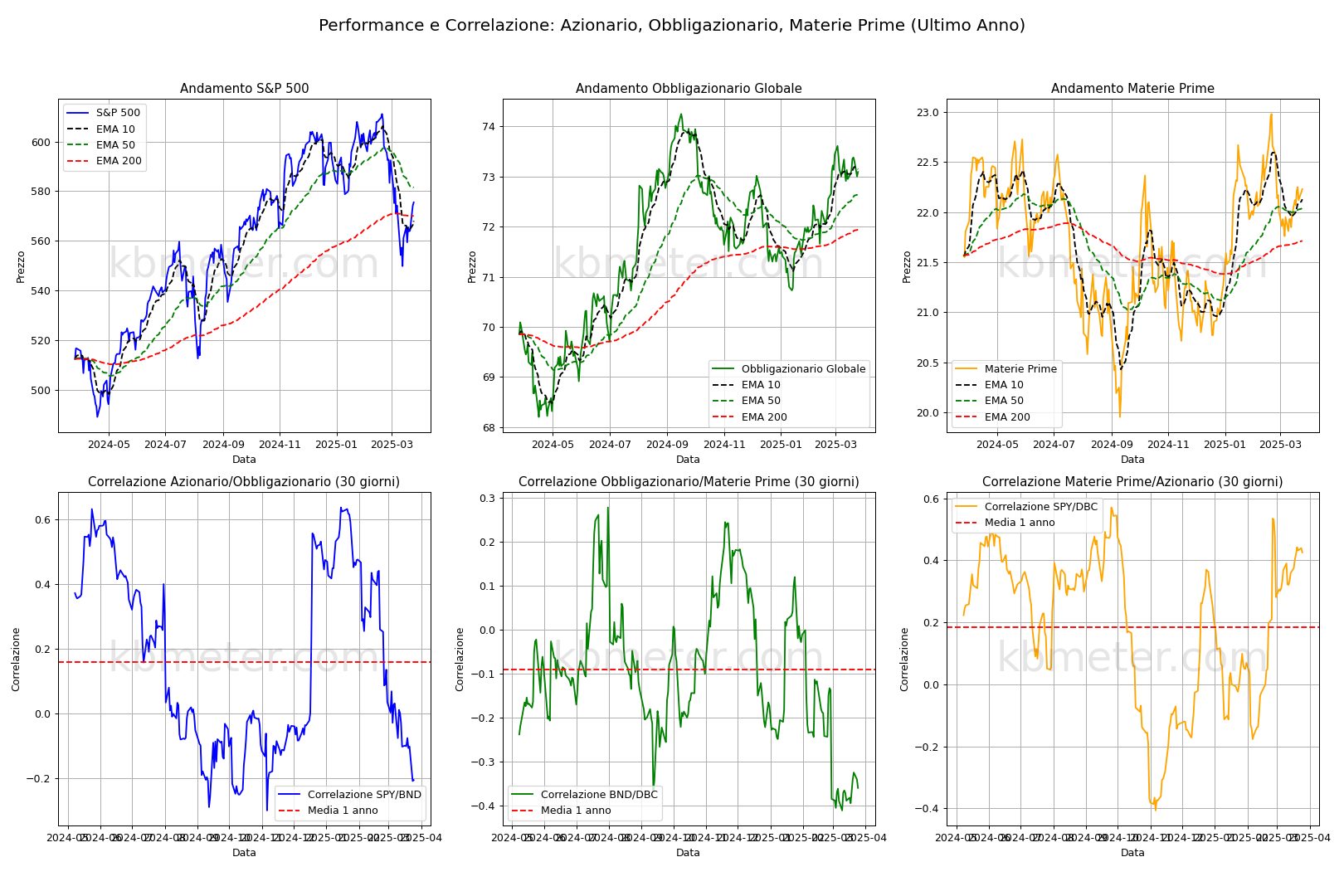

Our intermarket dashboards show that equity markets continue to stabilise after the slide of recent weeks. The S&P500/VIX ratio is back above its 50-day average and the T30/S&P500 is also moving towards risk-on. The S&P500 continues to rally but still lacks the crossing of the moving averages to give more stability to the move. Bonds seem to have no real direction these days, but the bullish trend that started in January is still valid for now. The picture for commodities is more complicated, but March still ended on a positive note.

On the macroeconomic front, February’s UK inflation data and US durable goods orders are worth watching.

Our forecast analysis points to another positive day for the equity markets, with some more uncertainty in Asia. On the bond front, positive signs are returning for European corporate bonds, while there is uncertainty over the direction of Treasury yields. Mixed signals for commodities, pause for gold. Volatility stable.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 26 March 2025 - 7:15 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.