U.S. Consumer Sentiment Signal Strengthens in may 2026 as Discretionary Spending Regains Leadership

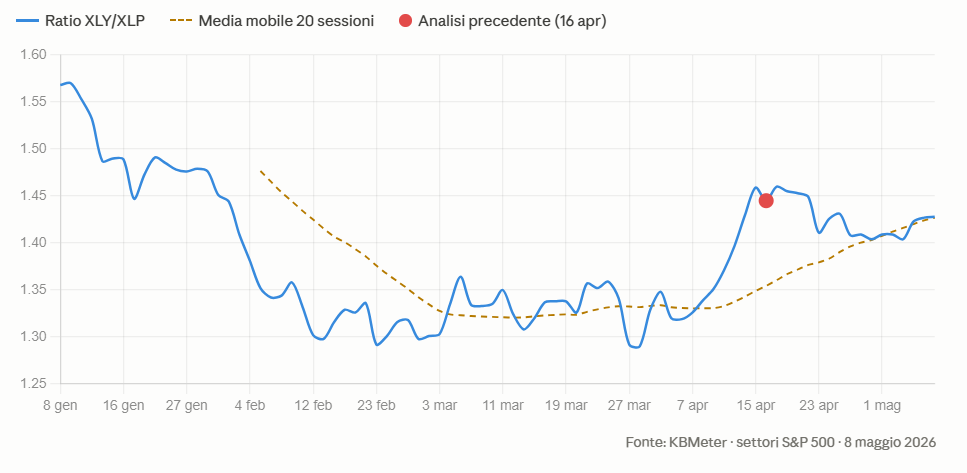

The intermarket analysis of U.S. consumer confidence shows an interesting development in May 2026 compared to the signal observed in April. The ratio between discretionary and defensive consumer sectors (ETFs XLY and XLP) has remained above its long-term moving average for the second consecutive month, confirming the resilience of the moderate improvement highlighted in April. However, the internal structure of the ratio has changed significantly: it is no longer driven by weakness in defensive sectors, but rather by renewed intrinsic strength in discretionary sectors.

The XLY/XLP ratio stands at 1.43 — the same level as in April, but with a different composition. A month ago, the ratio had risen because defensive consumer staples (XLP) were losing ground from their late January–February highs, while discretionary consumption (XLY) was rebounding from late March lows. Today, defensive sectors have regained their own technical strength — momentum rising from 47 to 67, RSI from 42 to 57 — while discretionary sectors are consolidating without giving up significant ground. It is no longer a retreat in defensive sectors pushing the ratio higher: the recovery is now more balanced.

The most noteworthy element is the divergence in the expected trajectory of the two sectors. The KBMeter system indicates a declining expectation for XLP — from 77.9 in April to 60.0 in May — signaling that the recent momentum in consumer staples is normalizing. At the same time, expectations for XLY improved from 57.3 to 67.1, the highest reading of the past four months, with indicators moving back into positive territory. In simple terms, the system points to the potential for further relative strength in discretionary consumption versus defensive sectors in the coming weeks.

The upward pressure accumulated in both sectors has also normalized. In mid-April, XLY still showed signals consistent with a fragile rebound vulnerable to reversal. Today, those signals are almost entirely absent in both sectors: the recent advance does not appear speculative in nature, but instead reflects a more gradual and sustainable recovery.

Overall, the picture suggests a moderate but more fundamentally grounded improvement compared to April. A month ago, the signal was encouraging but ambiguous — it could simply have been a technical rebound from the lows. Today, with the two sectors converging technically and with discretionary-sector expectations clearly improving, the signal appears more robust. The American consumer seems to be stabilizing around a less defensive sentiment, even though the broader macroeconomic uncertainty has not yet been fully resolved.