Gold, copper, and semiconductors: when markets tell two different stories

The relative-strength ratios between copper, gold, and semiconductors over the past 24 months highlight a significant divergence between financial markets and the real economy, with important implications for global growth prospects.

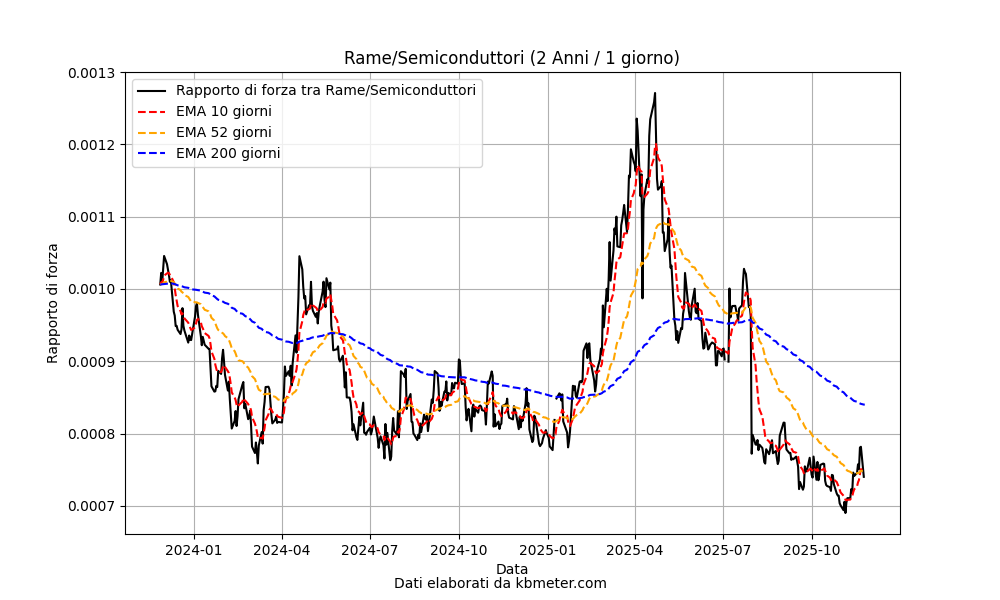

The copper/semiconductors ratio has shown pronounced deterioration since April 2025, with all moving averages (10, 52, and 200 days) aligning in a downward convergence. The ratio is hovering near two-year lows (around 0.0007), indicating a clear underperformance of the industrial metal relative to the technology sector.

This dynamic reflects weak expectations for traditional industrial demand, consistent with pressures stemming from trade uncertainty and tariffs. The market is favoring exposure to the tech/AI sector over cyclical assets linked to manufacturing and infrastructure, suggesting skepticism regarding a recovery in the real economy.

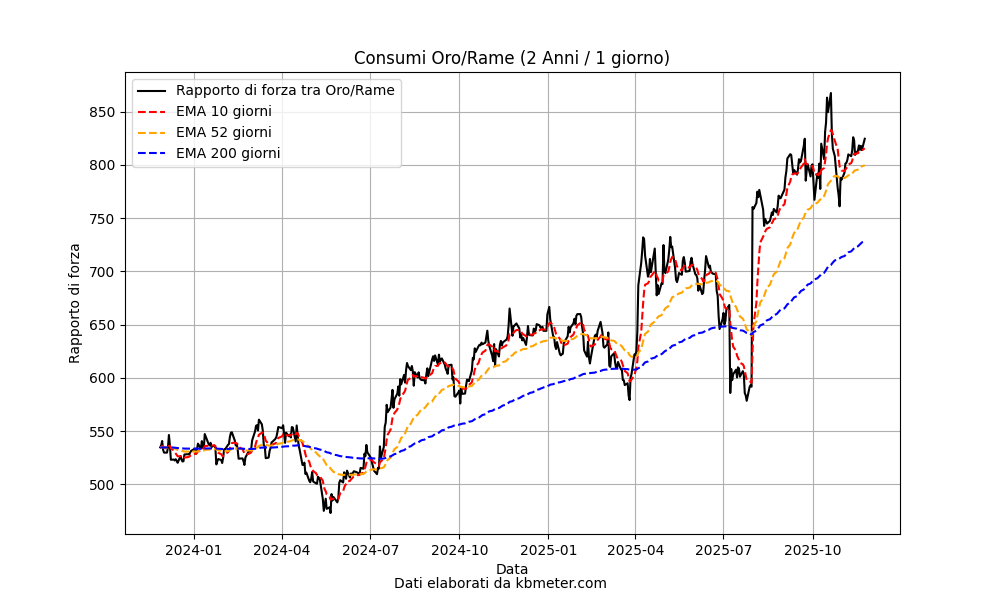

The gold/copper ratio has exhibited a sustained upward trend since mid-2024, peaking in October 2025 (around 860) and remaining elevated at current levels (820). All moving averages maintain a positive slope, with the ratio consistently above the 200-day average.

This pattern signals a persistent risk-off sentiment, with investors preferring the safety of the haven asset over cyclical exposure. Gold’s relative strength reflects structural concerns tied to geopolitical uncertainty, fiscal risks, and modest growth prospects.

Implications

The combined analysis reveals a bifurcated market: on one side, enthusiasm for the technology and AI sectors is supporting equity valuations; on the other, copper’s weakness and gold’s strength point to caution regarding the industrial economy and a search for protection.

This configuration aligns with the scenario outlined by the ECB in its Financial Stability Review: financial markets appear resilient yet are characterized by elevated valuations and latent vulnerabilities, within a context of weak economic growth and heightened structural uncertainty. The disconnect between financial-asset performance and real-economy indicators represents a source of fragility, particularly if multiple shocks were to materialize simultaneously.