US tariffs and economic stimulus in China

Tensions between the US and Europe, but also the threat of tariffs on Canada and Mexico. In other words, it is still the White House that will shape the mood of the financial markets at the start of this week. China is expected to provide fresh stimulus to the economy.

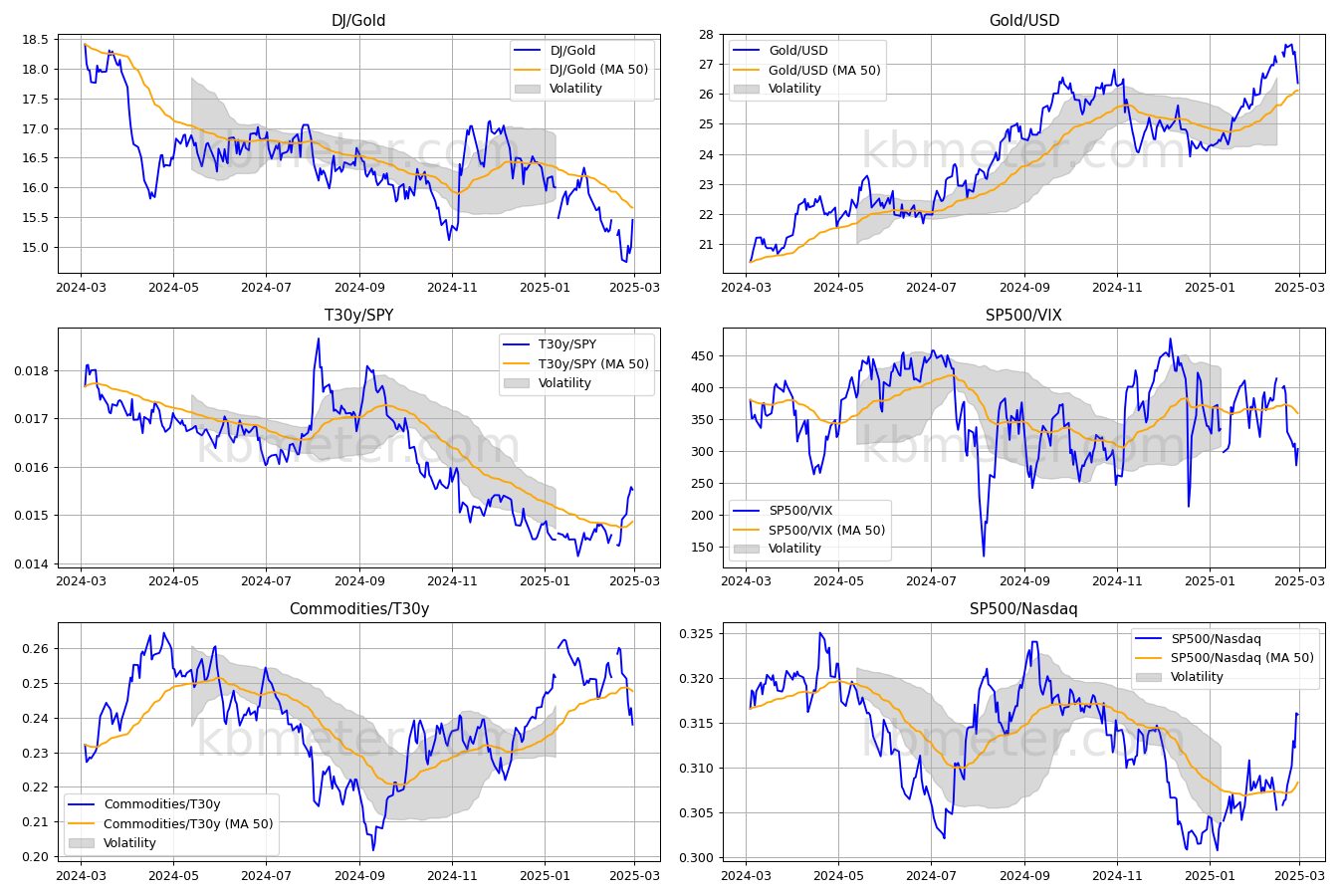

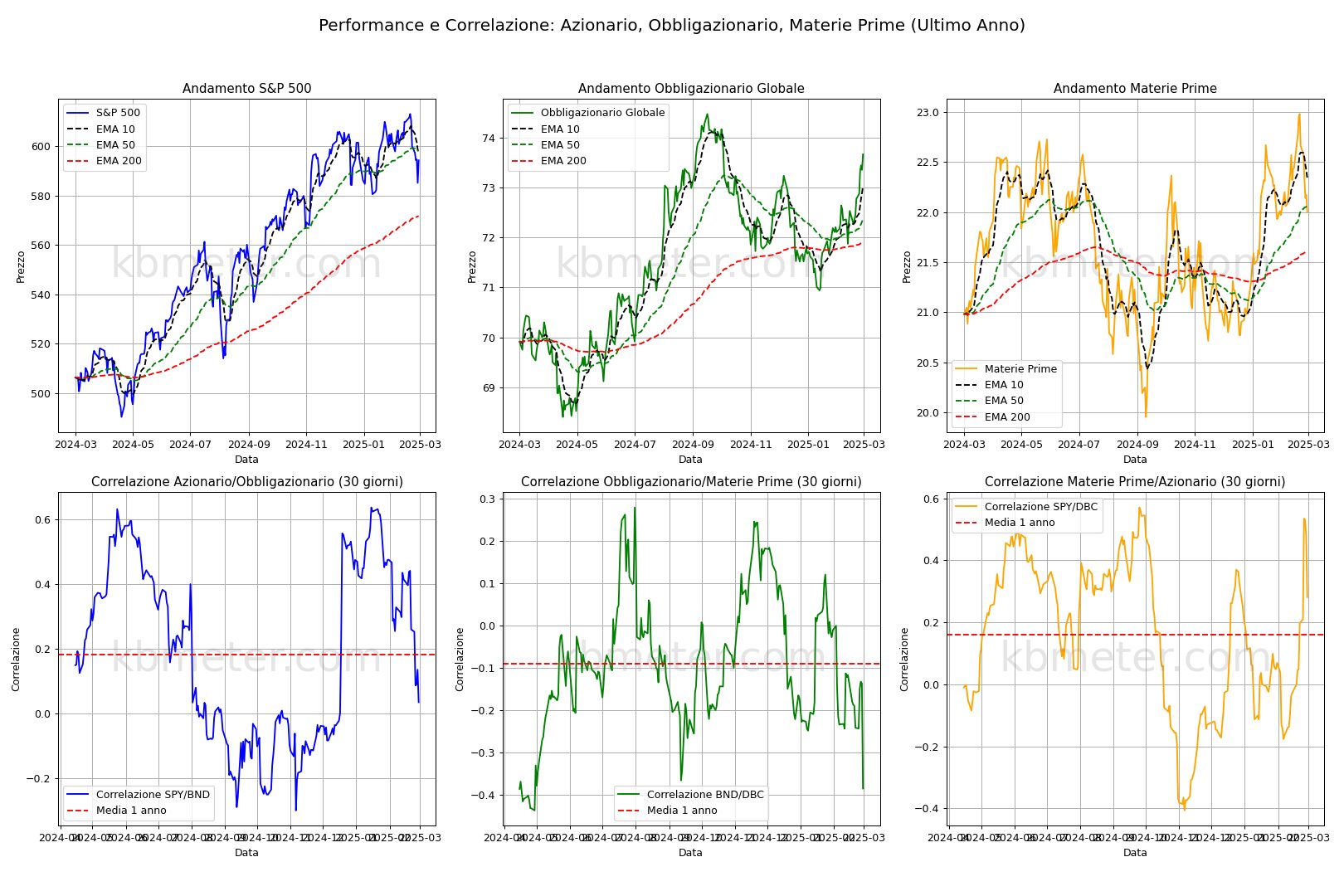

Our intermarket dashboards continue to show signs that investors are de-risking. Of note is the halting rally in gold and the recovery in the S&P500 versus the Nasdaq. In terms of trends in the major asset classes, bonds continue to rally, reaching the highs of early autumn 2024, while commodities continue to move broadly sideways.

On the macroeconomic front, the week will be dominated by US employment data (Wednesday and Friday), while in the eurozone we await the ECB decision and new growth estimates for the end of 2024.

Our forecast analysis continues to point to a wait-and-see approach for the equity markets, with a few more clues on the European front. Bonds remain moderately positive, while gold remains on hold. Volatility stable or slightly rising.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 3 March 2025 - 7:29 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.