US Jobs Data in Focus; Mild Risk-On Mood, Dollar Holds Firm

Today, financial markets are focused on the release of the U.S. June 2026 employment report. Following the ADP figures—which showed continued job growth, albeit at a slower pace than in May—expectations remain for a labor market that is fundamentally healthy and broadly stable.

The remarks made yesterday by Warsh at the ECB Forum in Sintra offered little guidance on interest rates, but enough to suggest that the Federal Reserve is likely to remain on hold until after the summer, with a bias toward further tightening rather than easing. This backdrop continues to support a strong U.S. dollar, while bond markets are experiencing a modest pullback.

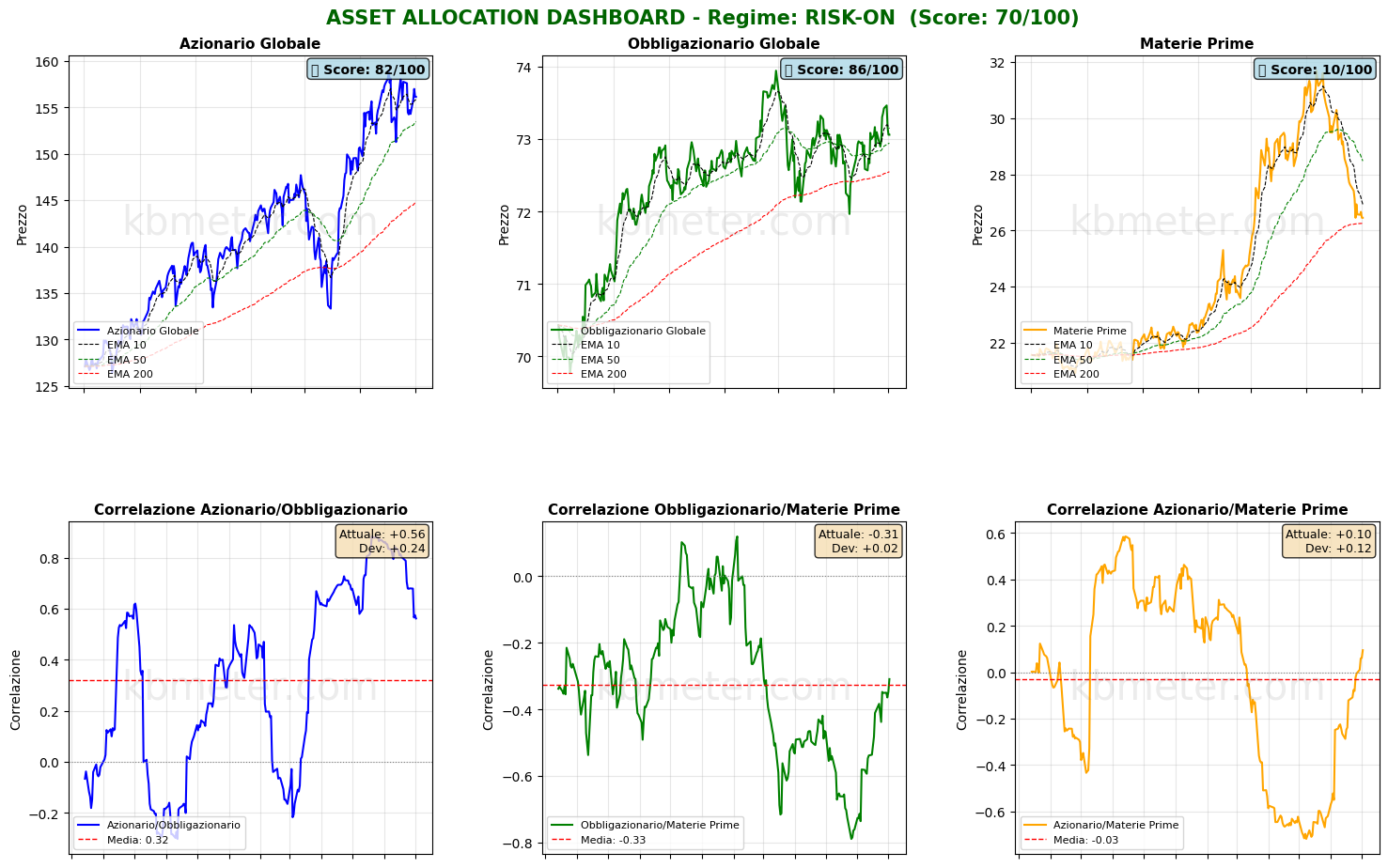

Investors remain in a mildly risk-on positioning, with the technology sector continuing to outperform. Meanwhile, commodities are holding above a key support area. Equity futures point to a flat opening in both Europe and the United States.

Market Weather Map

July 2, 2026

US Equities

Eu Equities

Asia Equities

Commodities

Bonds

Dollar Index

Technology

Gold

Oil

Crypto

Market Summary

Do you want to see the score details for all assets monitored by KBMeter?

Try free for 14 days →Financial markets sentiment

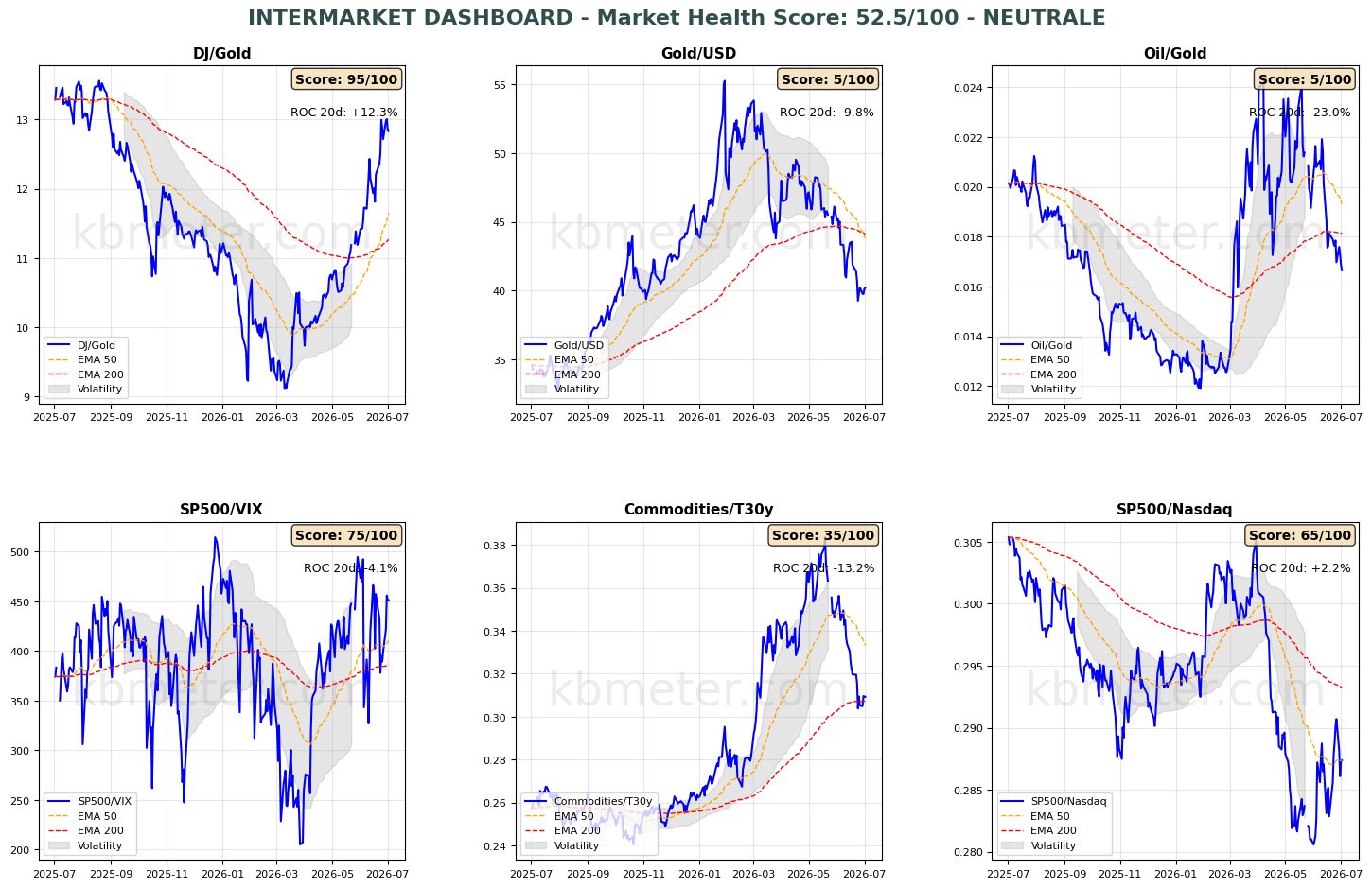

Overall, financial markets are displaying a neutral to slightly positive sentiment today. Our intermarket analysis shows a Market Health Score of 52/100, indicating a broadly neutral environment.

There have been few meaningful changes across our intermarket dashboards. Markets remain in a mildly risk-on mode while inflation expectations continue to consolidate. Notably, the Oil/Gold ratio has now returned to levels last seen in early March, effectively erasing almost all of the acceleration recorded over the past three months.

Across asset classes, the latest moves in global fixed income and commodities remain worth monitoring. Bond markets have lost momentum in recent sessions, with fading expectations for near-term interest rate cuts. At the same time, commodities continue to trade around the support provided by their long-term moving average.

Our Market Weather Map confirms this overall picture. Among the key developments, the U.S. technology sector has recovered to the 50-point threshold, while the U.S. dollar continues to display persistent strength, remaining comfortably above the 65-point mark.

Global Futures – Pre-Market Sentiment

Pre-Market Futures: Global equity futures indicate a moderately risk-on tone, with an average gain of +0.02%. U.S. futures are slightly negative (-0.02%), European futures are modestly positive (+0.08%), while Asian futures are marginally lower (-0.10%).

📊 Global Futures – Pre-Market Sentiment

- Hang Seng derived: +0.70%

- TecDAX derived: +0.62%

- Mini DAX: +0.19%

- Nikkei 225 derived: -0.50%

- CSI 300: -0.49%

- IBEX 35 derived: -0.22%

Macroeconomic calendar

On the macroeconomic front, today’s attention is centered on the June 2026 U.S. labor market data. Consensus expectations call for employment growth of more than 100,000 jobs, representing a moderation from the previous month. Investors will also be watching the release of U.S. May factory orders, Eurozone unemployment data, and the latest update on Australia’s trade balance.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 2 July 2026 - 7:40 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.