Quarterly reports bring calm to stock markets

The stock markets seem to have regained some calm after last Monday’s storm. Quarterly reports on the one hand and good macro data on the other are prompting optimism. But there is no shortage of pitfalls, as shown by the reaction to Trump’s new threat of tariffs on Canada and Mexico.

Positive results from Apple and indications that the US economy continues to grow at a robust pace brought optimism back to the equity markets. At the end of the session, however, Trump’s new threats of tariffs on Canada and Mexico sent the main US index to its lowest point of the day and strengthened the dollar. The effect was short-lived, but it is yet another reminder of how sudden volatility continues to dominate the markets.

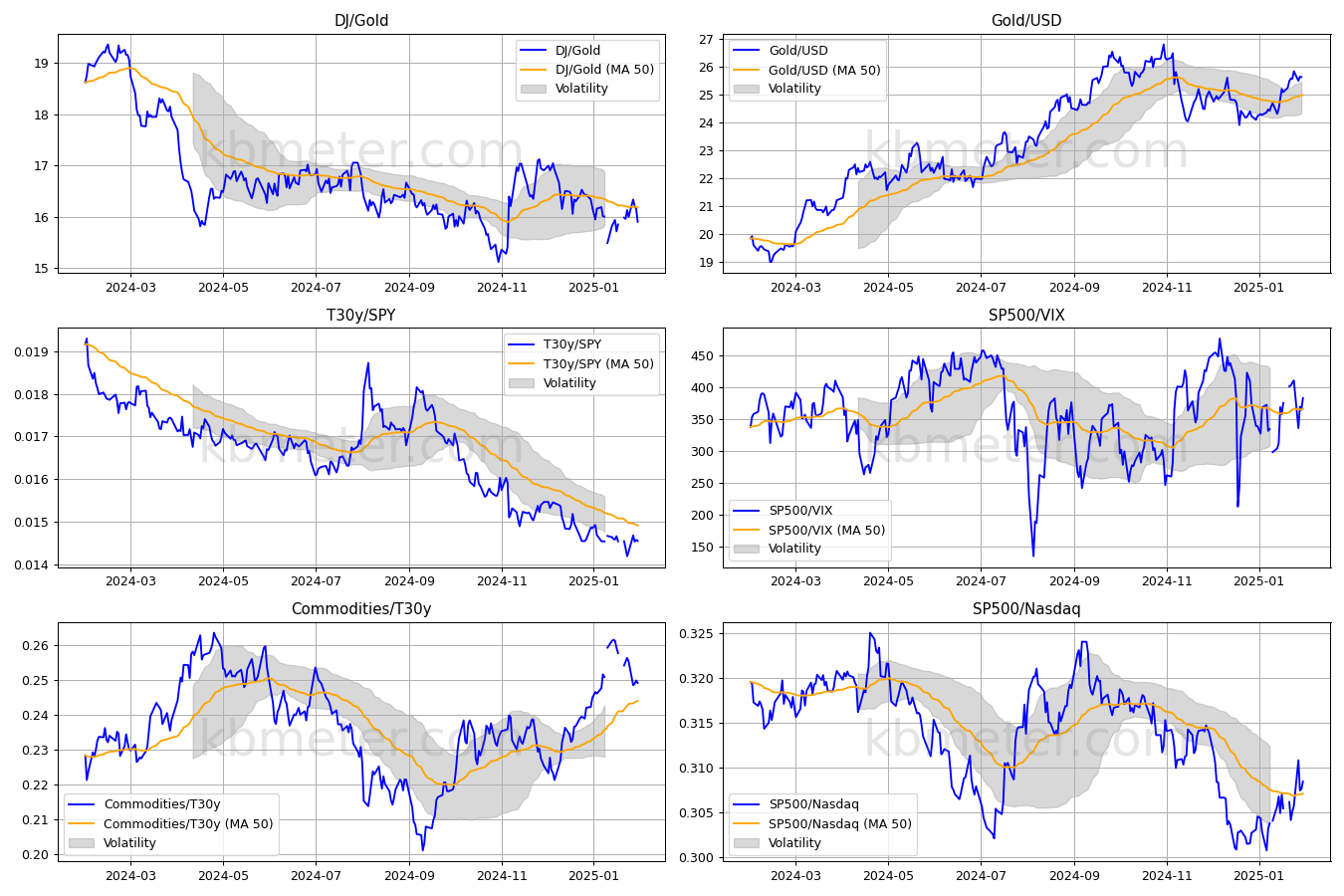

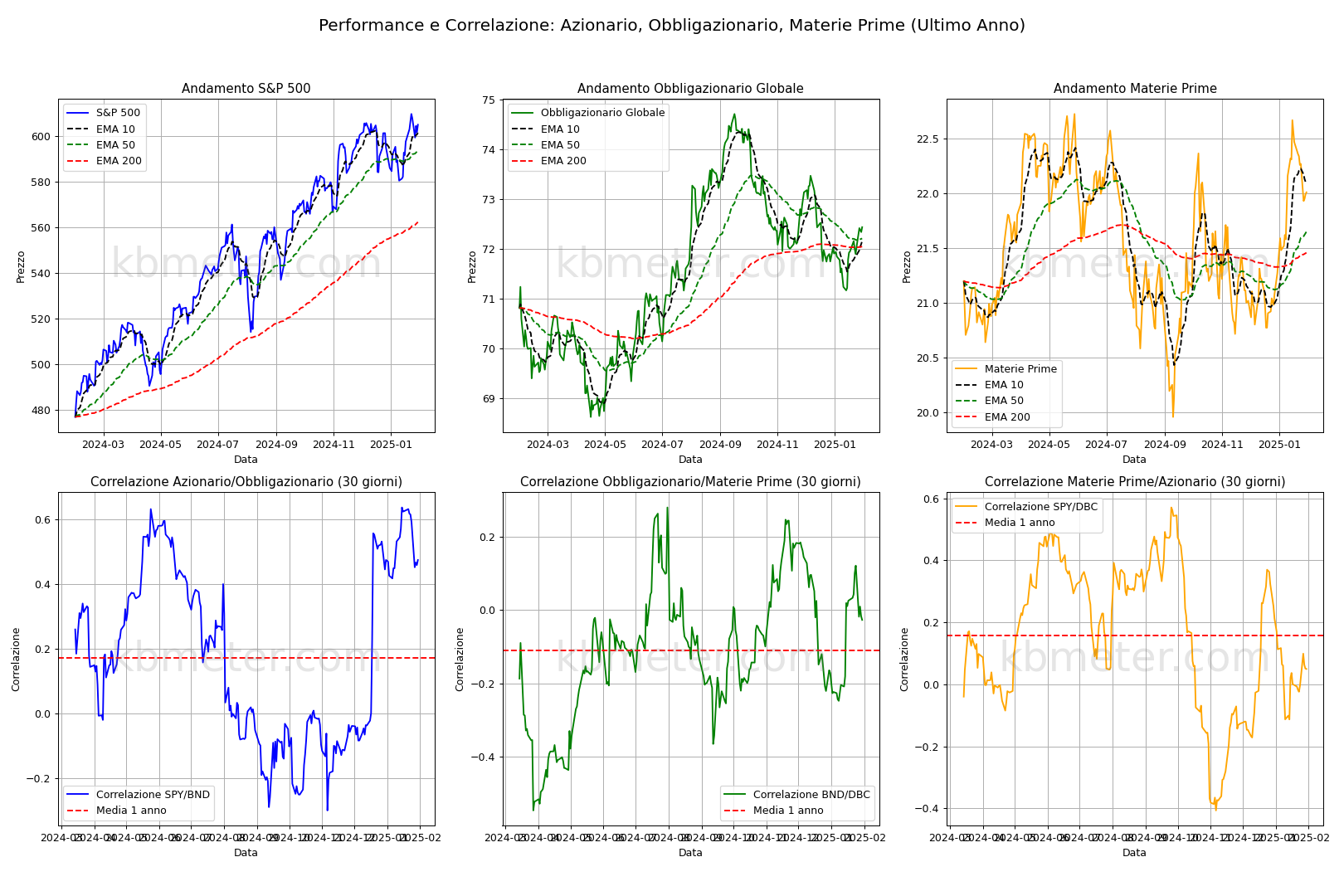

Looking at our intermarket dashboards we observe two things: the cooling of the ratio of commodities to 30-year Treasuries, signalling somewhat more moderate inflation and growth expectations, and the strength of gold. If we look at the first month of the year, bullion proved stronger than both equities and the dollar. Another technical consideration concerns the bond market, which has reached an important resistance area. The coming weeks may tell us something more about the trend in bond prices.

And a first element may already arrive today with the release of the PCE price index, the price indicator most considered by the FED. The data released yesterday suggest a slight acceleration. Expected today, again from the US, are data on personal spending and incomes for December. In the Eurozone, watch out for inflation data from Germany and France.

On the earnings front, data from two energy biggies – Exxon and Chevron – are expected today.

Our forecast analysis indicates a positive day for equity markets, with buying signals also increasing. Uncertainty on the bond front, while on the commodities front the situation remains positive for precious metals. Volatility expected stable.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 31 January 2025 - 7:36 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.