Markets turn risk-on as Middle East tensions ease and Fed signals rate cut openness

Markets are once again feeling the wind of risk-on sentiment, as investors acknowledge the truce in the Middle East and listen closely to the potential signals from the Federal Reserve for a possible rate cut as early as July. Equities are expected to rise (more so in the U.S. than in Europe), while bond yields are declining.

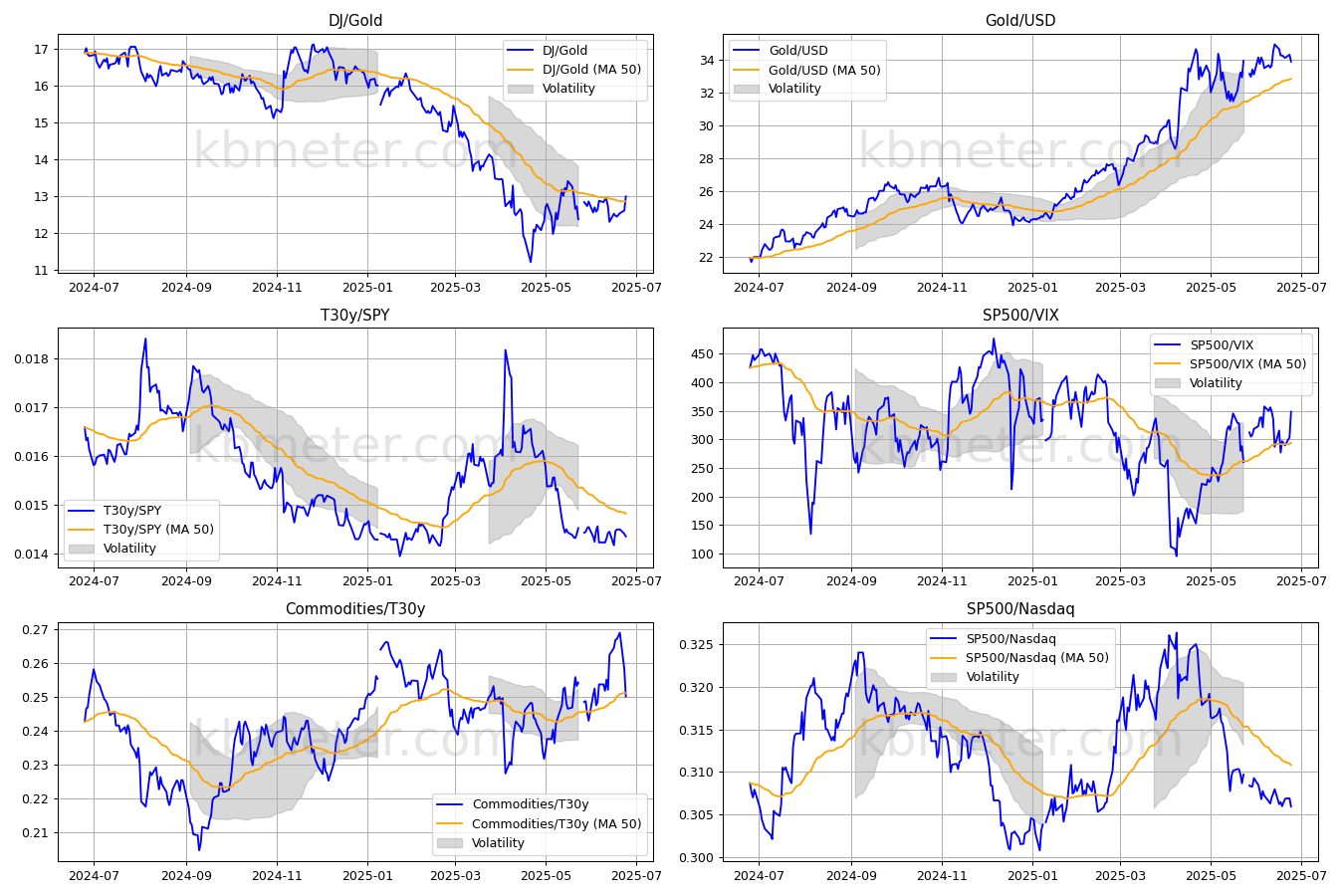

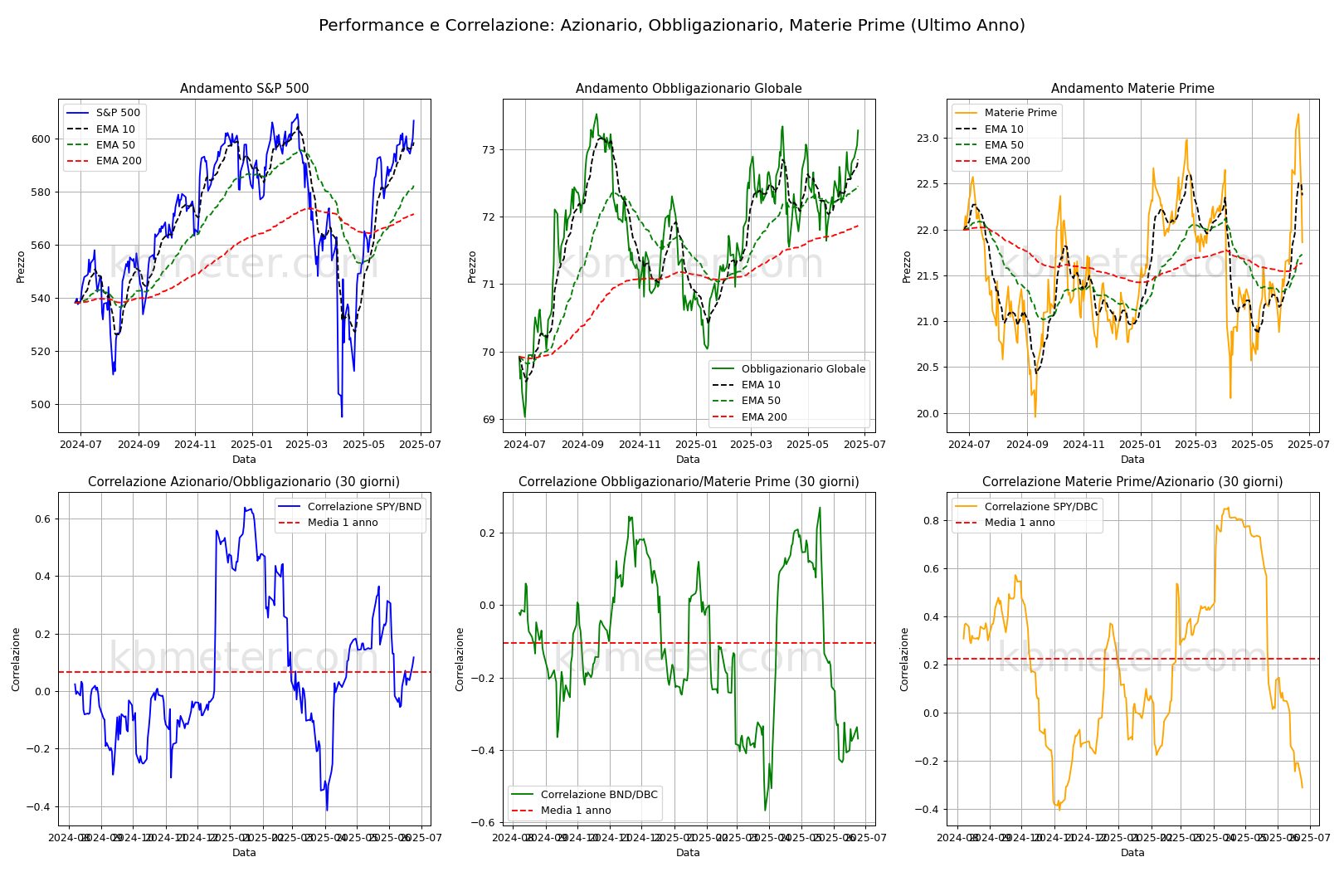

Our intermarket dashboards indicate a return to risk-on conditions. The S&P500/VIX ratio has risen above the one-year average, and the same goes for the Dow/Gold ratio. Technology stocks are leading this move, with the S&P500/Nasdaq ratio falling to its lowest levels since last February. After all, the medium-term trend setup had not been disrupted by recent international tensions. The S&P500 has reclaimed its early-year highs, while the bond market has reached levels last seen in March. The correlation between these two asset classes has turned positive again.

On the macroeconomic front, it’s a day with no particularly market-moving data. U.S. new home sales figures are expected, along with labor market data from France. Powell’s testimony in Congress will also be of interest.

Our forecasting models suggest another positive day for equities, with signals once again much stronger for U.S. stocks compared to European ones. Positive signs are also emerging from Asia. In the bond market, yields are falling and corporate bonds remain in the green. Volatility is expected to decline.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 25 June 2025 - 7:09 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.