Markets hope to breathe after turbulent day

After a tumultuous day, financial markets may breathe a little easier, especially if the White House follows through with the opening on tariffs with Canada and Mexico that Commerce Secretary Howard Lutnick announced yesterday. Bonds have been weighed down by two opposing forces: inflation expectations outside the US and risks to US growth.

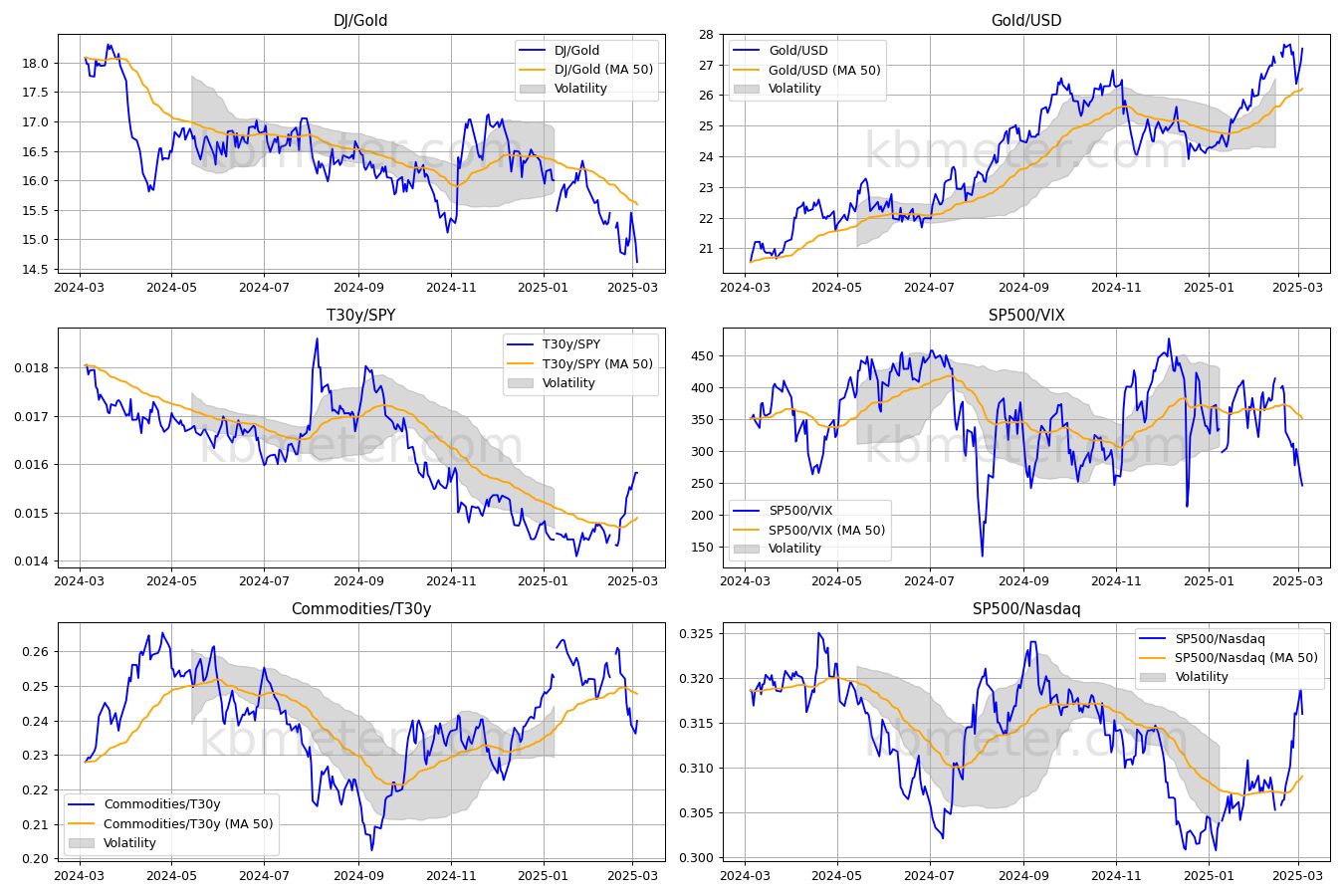

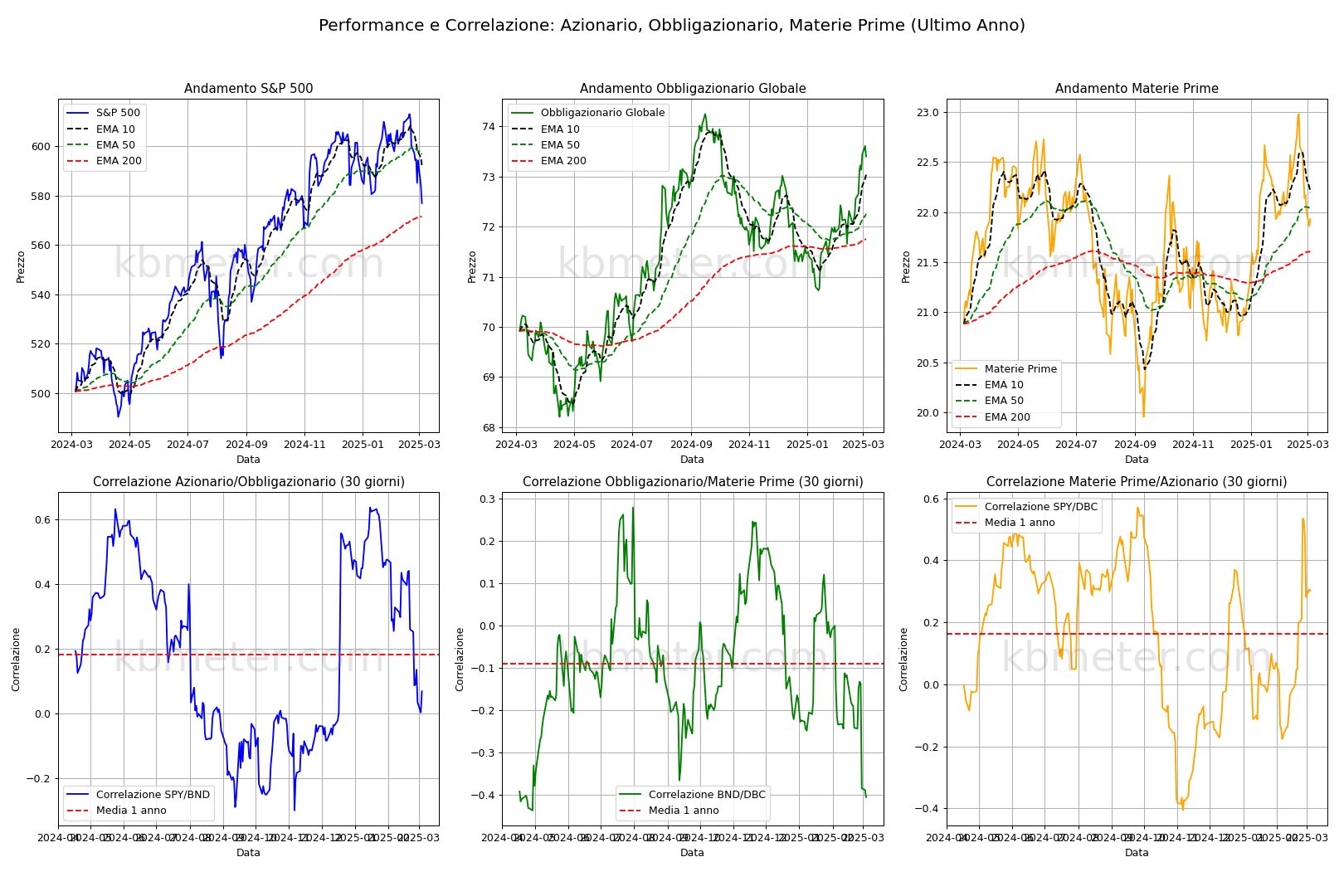

Our intermarket dashboards confirm the risk-on nature of the markets. Of particular note are the S&P500 and global bond trends (charts on the right). The former is falling below the lows of early 2025 and is approaching 200-day average support, while the latter is slowing on renewed inflation fears. Fears that are simultaneously pushing up commodity prices (in a sideways movement).

On the macroeconomic front, US ADP employment data for February and ISM services data for February are expected. From the Eurozone, producer prices data for January is due. Other interesting data will come from China (services PMI) and Australia (Q4 GDP 2024).

Our forecast analysis points to an intermediate day for equities. US equities are slipping into oversold territory, but there are no clear buy signals. Gold is on hold, while on the bond front, European yields are decelerating, probably discounting the risk of a re-acceleration of inflation due to tariffs. The dollar remains on standby, with sterling and the Swiss franc on the rise. Volatility has increased in both equities and bonds.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 5 March 2025 - 7:22 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.