Markets Hold Neutral Bias Ahead of Eurozone Inflation, U.S. Labor Data

Despite the early-week rebound led by technology stocks, uncertainty continues to weigh on financial markets. Market sentiment remains in neutral territory, although our proprietary barometer has slipped into risk-off territory. Investors are awaiting further clarity from today’s scheduled meeting between the United States and Iran, while the macroeconomic calendar features the first June inflation readings for the Eurozone and the May U.S. Job Openings report. Inflation and employment will be the key drivers of this week’s macro agenda, although markets have yet to show strong conviction. Equity futures point to a modestly positive open in both the United States and Europe.

Market Weather Map

June 30, 2026

US Equities

Eu Equities

Asia Equities

Commodities

Bonds

Dollar Index

Technology

Gold

Oil

Crypto

Market Summary

Do you want to see the score details for all assets monitored by KBMeter?

Try free for 14 days →Financial markets sentiment

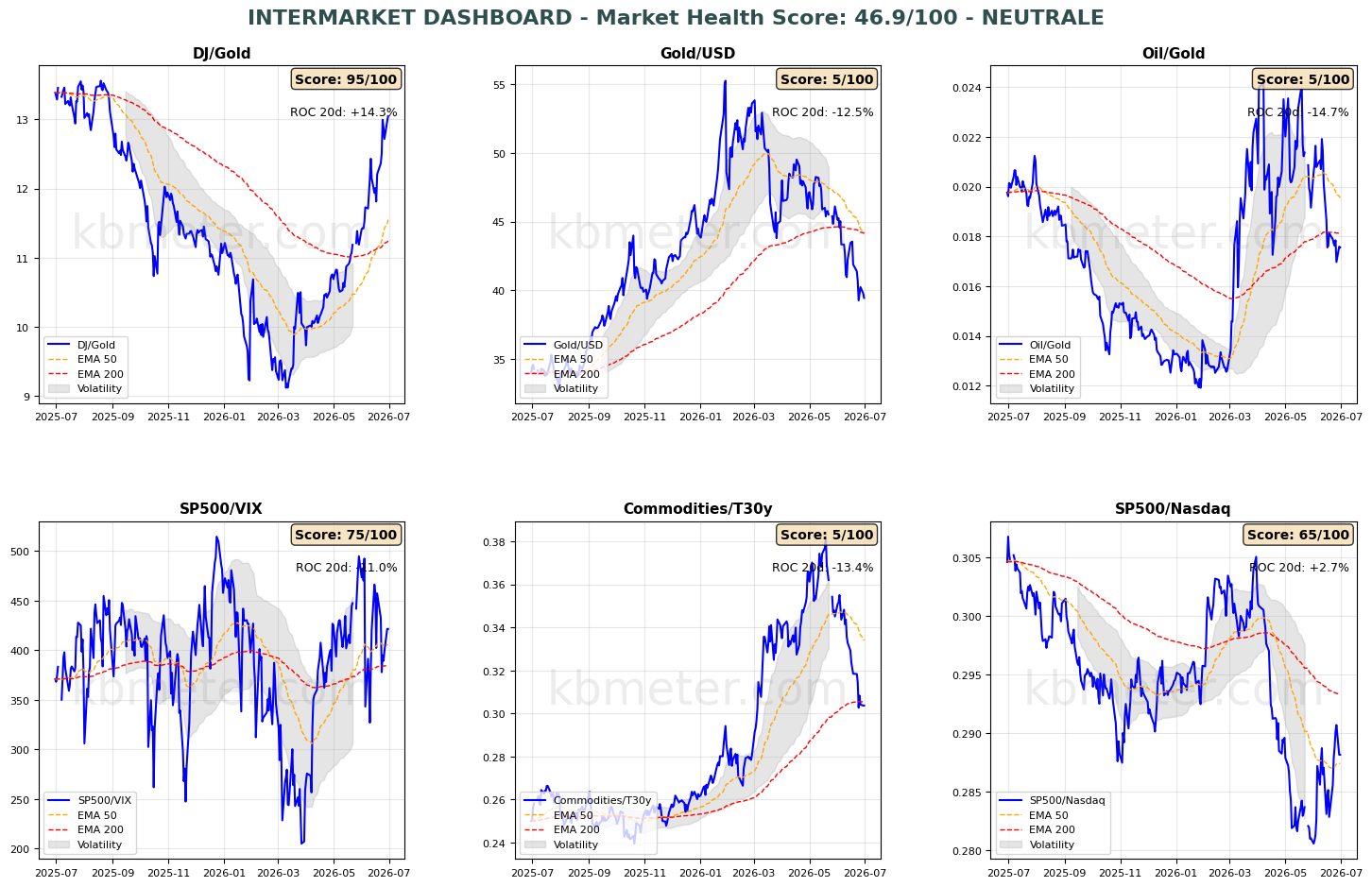

Financial markets are currently displaying a neutral sentiment. Our intermarket analysis shows a Market Health Score of 47/100, consistent with a neutral outlook. Our intermarket dashboards continue to indicate an environment where risk appetite remains positive but lacks momentum. Meanwhile, gold remains under pressure, while the decline in oil prices appears to have found a solid floor. The Dow/Gold ratio has climbed to its highest level since last September, while the Gold/U.S. Dollar ratio has fallen to its lowest point since last November. It is also worth noting that the Commodities/Bonds ratio has settled almost exactly on its long-term moving average, suggesting that inflation expectations may be stabilizing.

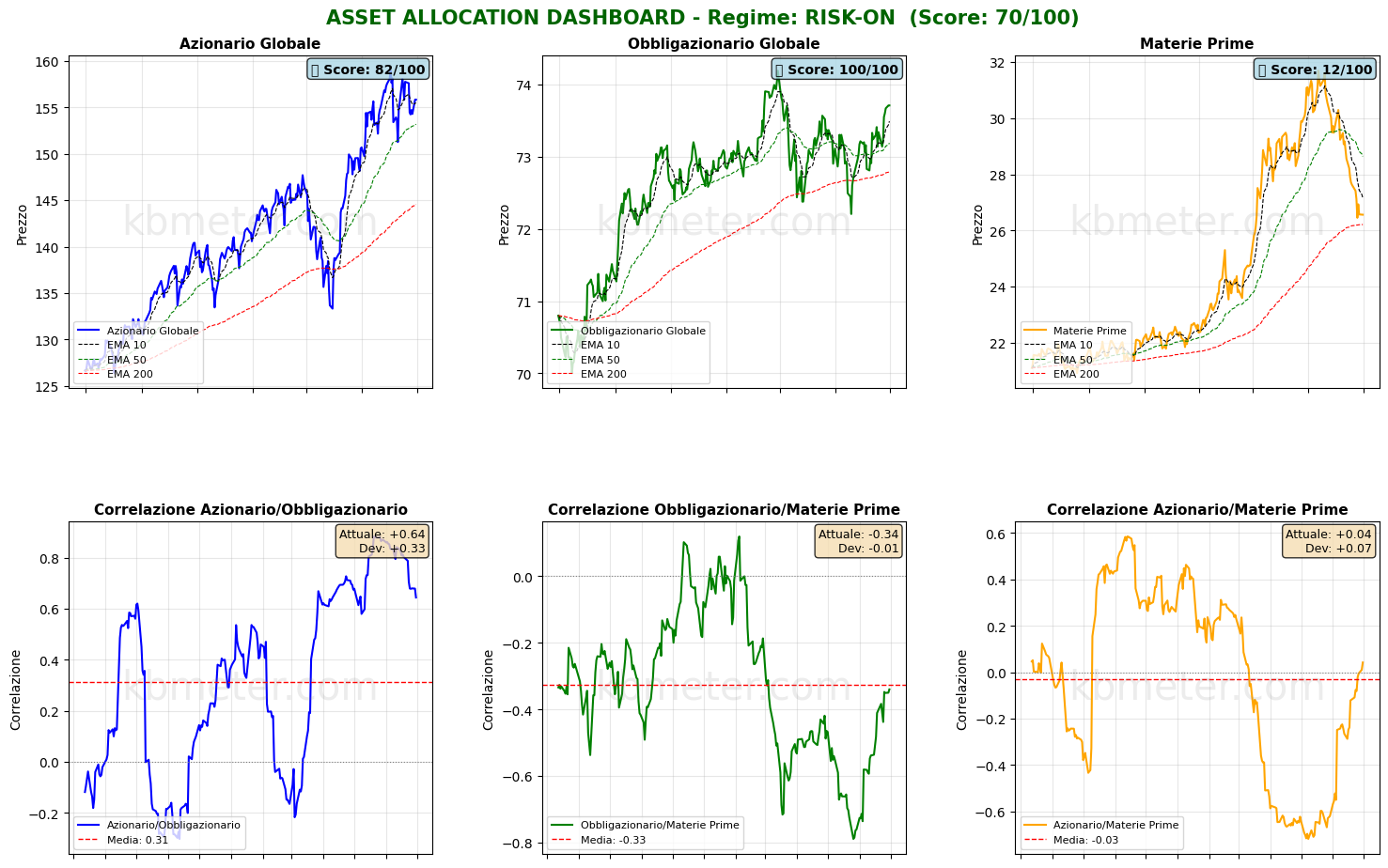

Looking across the major asset classes, there are no significant changes to report, although a few developments deserve attention. Commodities continue to hold above their long-term moving average, providing further evidence that the recent decline in oil prices may have reached its bottom. Equities and bonds have resumed moving higher together, although the positive correlation between the two asset classes has weakened.

Our market weather map continues to identify the U.S. dollar as the strongest asset we monitor, with the highest score across our dashboard. U.S. equities continue to outperform the technology sector, while oil, gold, and cryptocurrencies remain relatively weak.

Global Futures – Pre-Market Sentiment

Pre-Market Futures: Global equity futures point to a moderately risk-on tone, with an average gain of +0.21%. U.S. futures are modestly higher (+0.19%), European futures are slightly stronger (+0.34%), while Asian futures are marginally lower (-0.17%).

📊 Global Futures – Pre-Market Sentiment

- TecDAX derived: +1.09%

- CSI 300: +0.63%

- DAX derived: +0.60%

- Hang Seng derived: -1.19%

- FTSE MIB derived: -0.21%

- FTSE 100 derived: +0.00%

Macroeconomic calendar

On the macroeconomic front, today’s agenda includes Japan’s May employment data and the latest private-sector PMI survey from China. The Eurozone will release several important indicators, including German retail sales and, more importantly, the preliminary June inflation estimates for France, Italy, and Germany. In the United States, investors will focus on the May 2026 Job Openings report, the Conference Board Consumer Confidence Index, and the latest U.S. house price data. On the corporate front, attention will be on Nike’s quarterly earnings release.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 30 June 2026 - 7:49 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.