Financial markets return their focus to the macroeconomic data

Having digested last weekend’s news, the financial markets are once again focusing on macroeconomic data. Today, there will be some interesting ones, ranging from the new Eurozone GDP estimate to producer price trends in the US. Investors are trying to identify the initial effects of tariffs on the economy. Equities and bonds are slowing, but commodities are recovering, with the exception of precious metals.

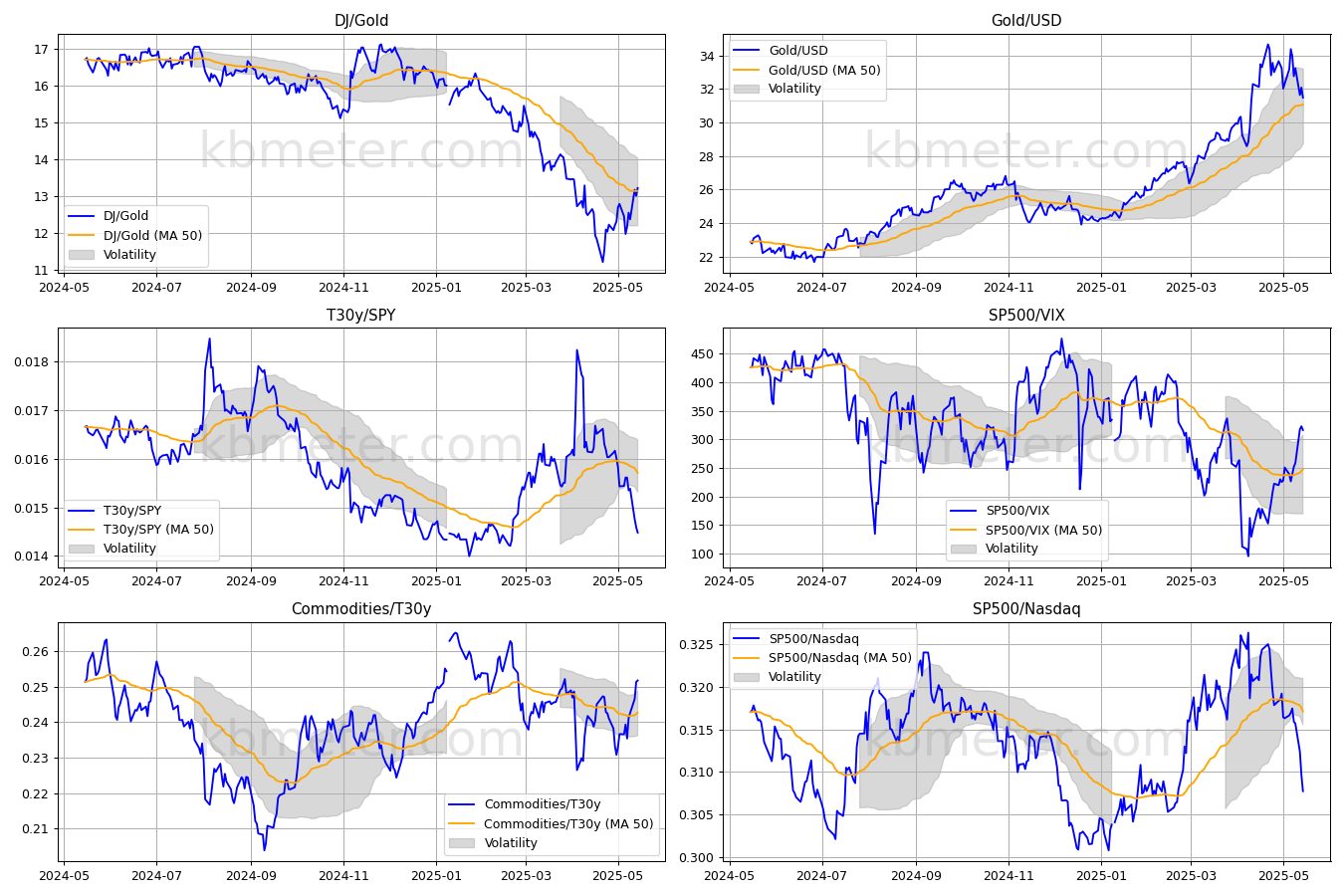

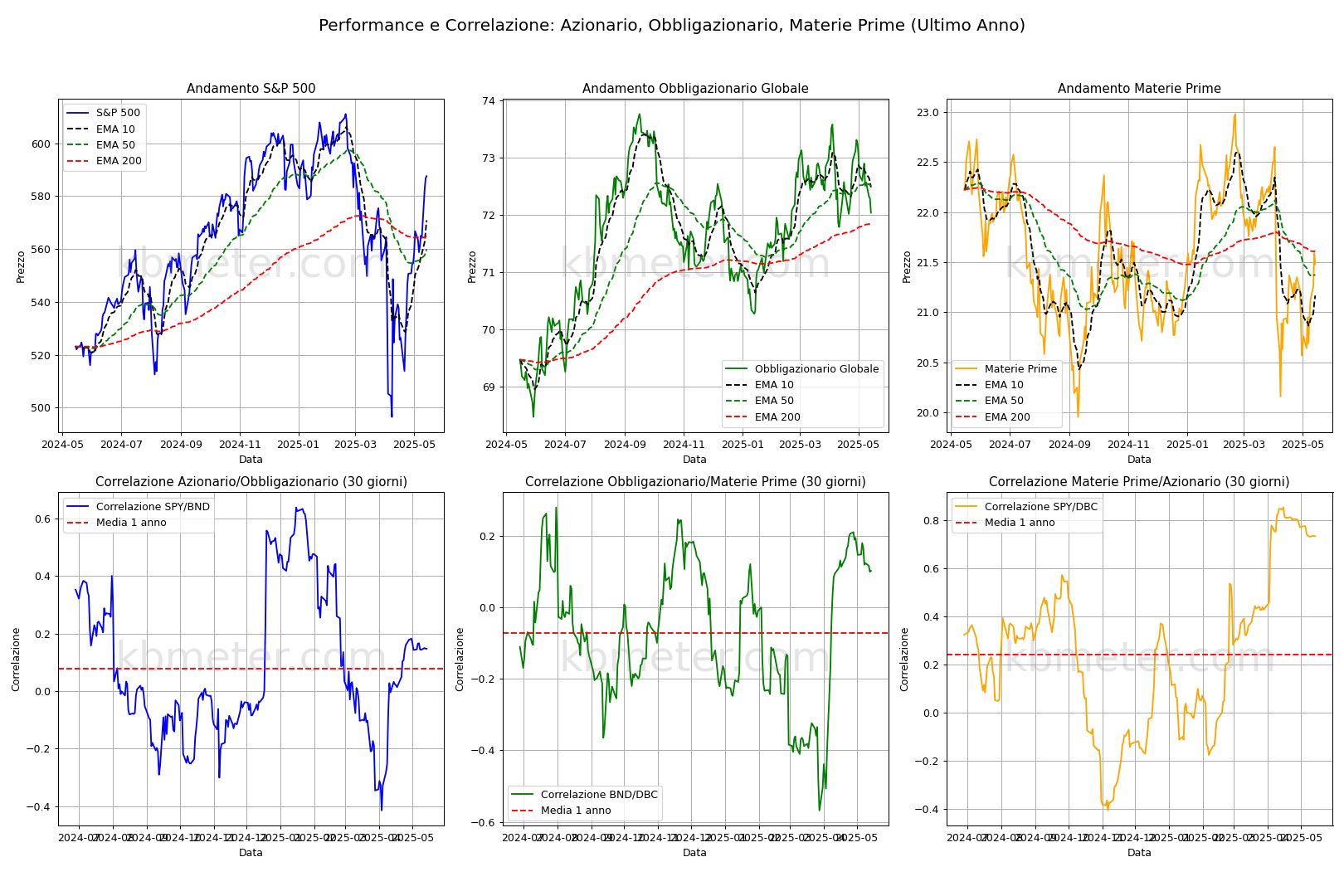

Our macro dashboards indicate that the situation on the sentiment front is broadly stable. The Dow/Gold and Gold/Dollar ratios have returned to their annual averages. The recent downtrend in bullion has had a significant impact. Another thing to keep an eye on is the performance of global bonds, which have broken through the 50-day average and are supported by the 200-day moving average.

It’s an interesting day for macroeconomics. New GDP data is coming in from the Eurozone and the UK, and there are also expectations regarding the employment situation and industrial production trends in the Eurozone. From the US, we will see the April retail sales figures, the Philly Fed index, industrial production and producer prices (the latter of which will be very interesting in terms of understanding the initial effects of tariffs).

Our forecast analysis indicates that the rally in equities is cooling, with signs of a wait-and-see approach in both the US and Europe. In terms of bonds, yields are still rising, while commodities are showing positive signs, excluding precious metals. The dollar is improving and volatility is broadly stable.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 15 May 2025 - 7:33 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.