Central banks’ week for financial markets

First the Fed, then the Bank of England and the BoJ. Today marks the start of a central bank-focused week. The financial markets are waiting for the central institutions’ moves and, above all, for some indication of the impact of tariffs on future monetary policy decisions. Equity markets remain weak despite some improvement; bonds are still on hold.

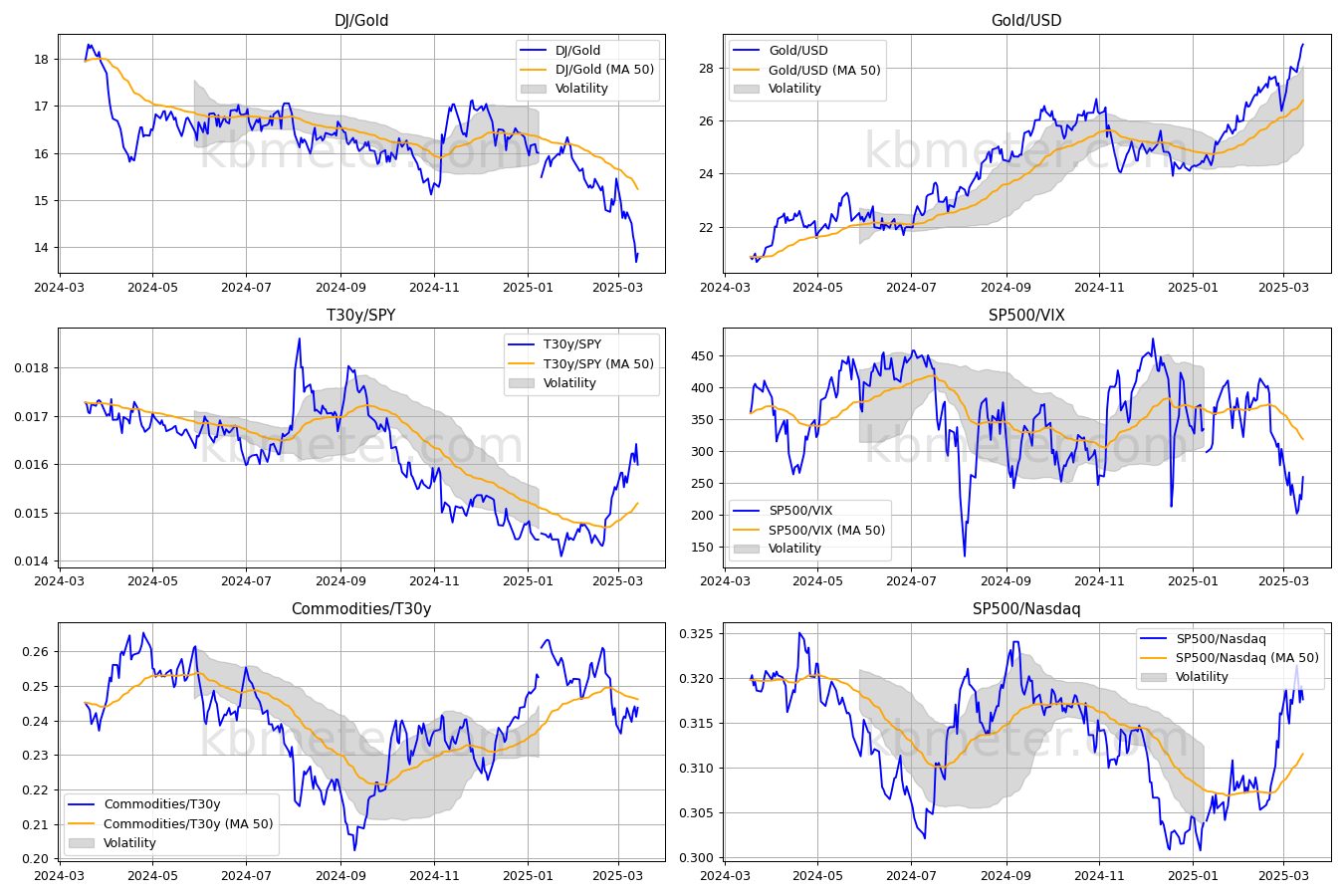

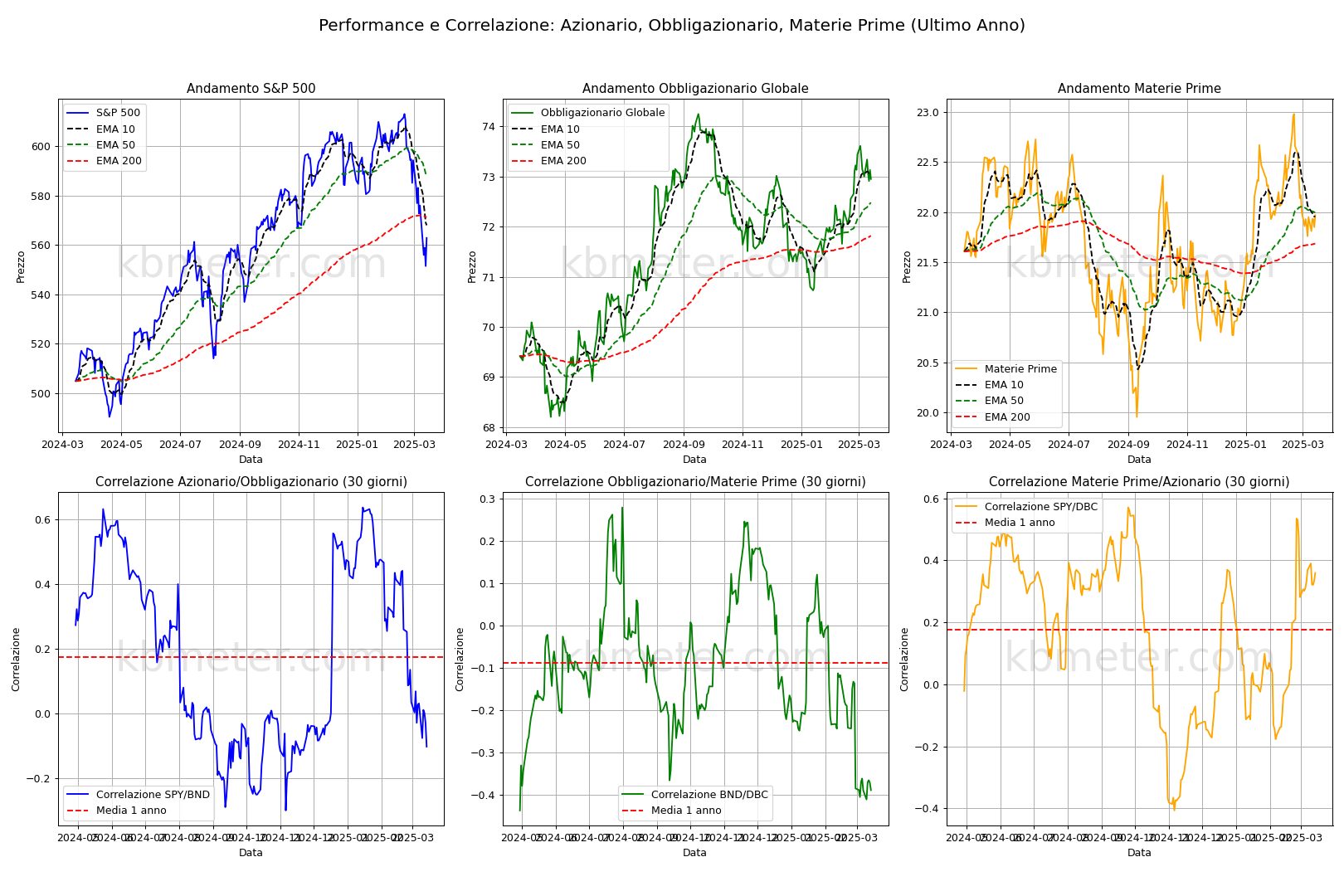

Last week’s positive close is reflected in our intermarket dashboards, although the situation remains more risk-off than risk-on. Gold continues to fly against the Dow and the dollar, while the rise in the strength ratio between long Treasury yields and the S&P500 has come to a halt. The main US index is attempting to recover from the 5500 level, and holding this area could reassure the continuation of the long term bullish trend. Bonds also remain bullish in the medium term, with the fall in prices currently halted at the 73 resistance level (right-hand chart). Commodities remain sideways.

On the macroeconomic front, while we wait for the FED, today we will see the US retail sales data for February and the Empire State index for March. These are useful indicators for understanding how consumers and businesses are coping with this new phase of uncertainty about the future of the US economy.

Our Forecast Analysis notes the slight improvement from last Friday and still points to an intermediate day for equities. Several buying signals in both the US and Europe. Metals remain positive, while on the currency front only the pound is showing positive signs. Bond yields broadly stable, volatility little moved.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 17 March 2025 - 7:26 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.