Beyond tariffs, financial markets eye ECB

Financial markets are trying to look beyond US tariffs for clues and are looking to the ECB, which is expected to cut interest rates again today. Investors remain cautious, with equities trying to maintain their long bullish stance as the bond rally takes a breather.

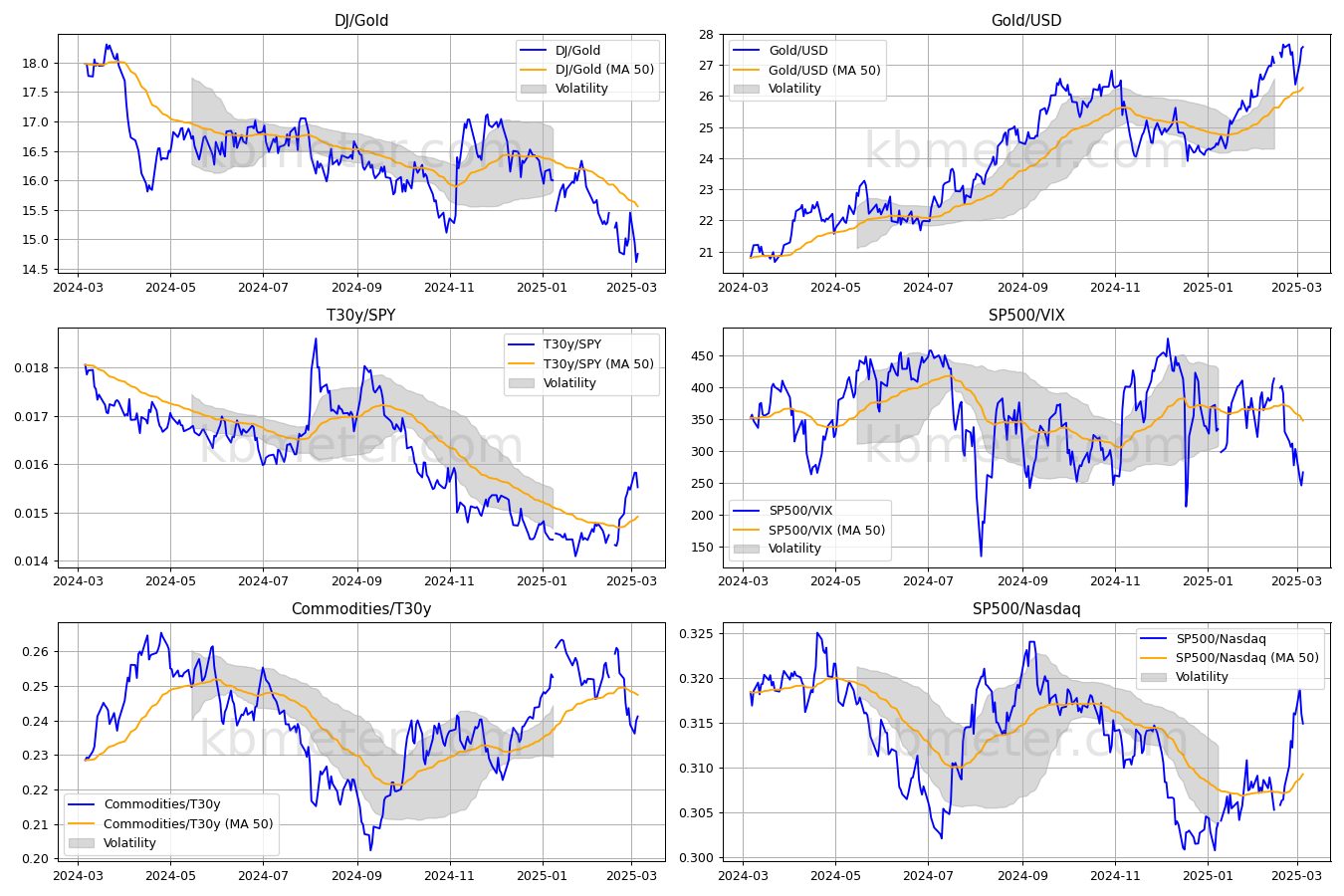

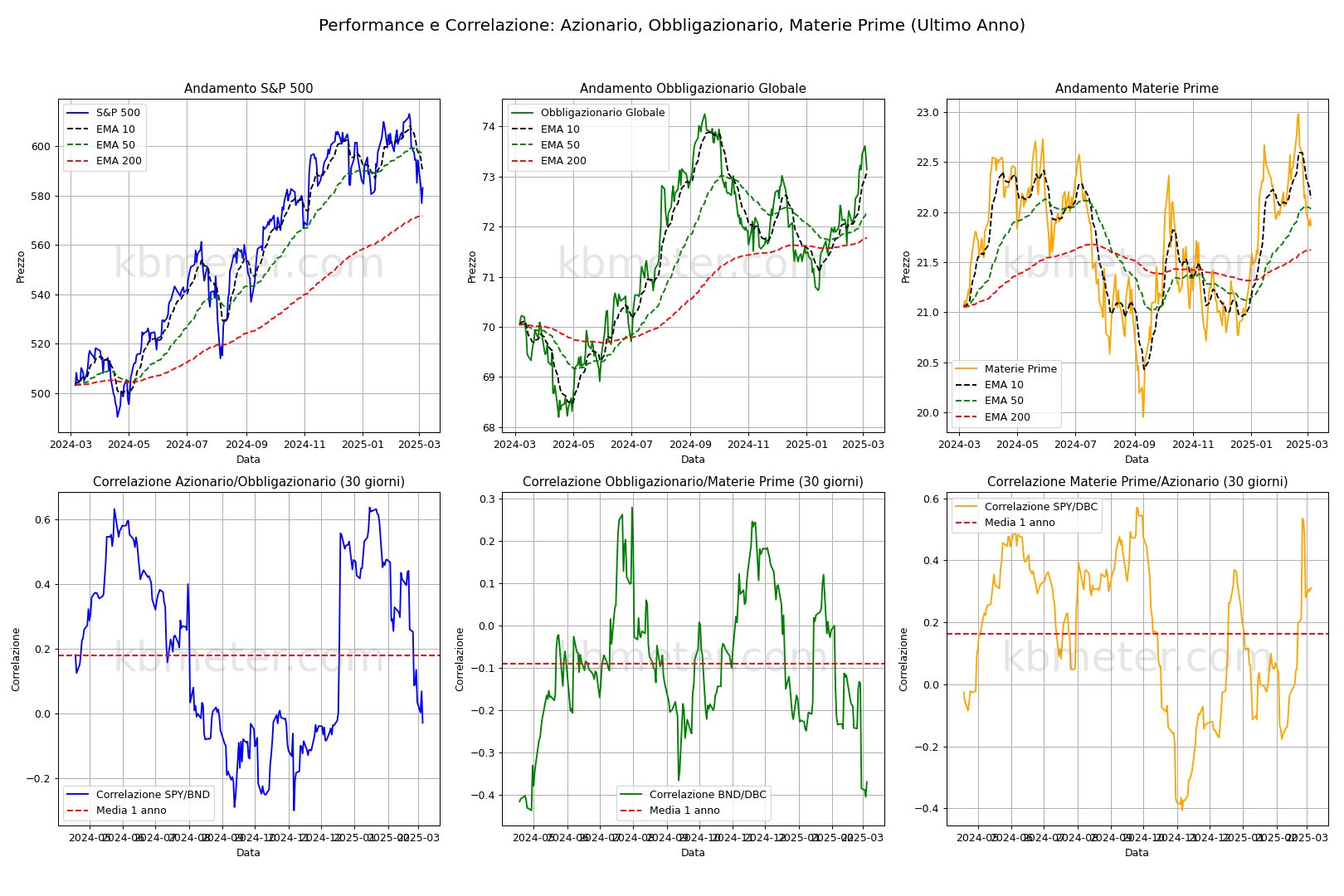

Our intermarket dashboards show a situation that is tending to stabilise after the falls of recent days. However, investor sentiment remains cautious. The S&P500 remains in the danger zone but is currently maintaining its long-term bullish stance. Bonds are pulling back, signalling a pause in the rally.

On the macroeconomic front, it is the day of the ECB, which is called upon to provide clues on the next monetary policy steps in the light of international trade tensions. Expectations are for another 25bp cut, which seems almost a foregone conclusion. Also of interest will be Eurozone retail sales, imports and US initial jobless claims.

As far as quarterly reports are concerned, the big names in the retail sector continue to publish their accounts, with Macy’s and Costco due today.

Our forecast analysis points to an intermediate day for equities, but with much less gloom than in recent days. More positive signs for Europe. On the bond front, there seems to be a pause in the bond rally, while on the currency front, the Swiss franc and the pound sterling are maintaining their good momentum, while the dollar is on hold. Volatility is stable or rising moderately.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 6 March 2025 - 7:26 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.