Awaiting tariffs, investors look to macroeconomic data

Financial markets remain at the mercy of tariffs, the end of Q1 brings some technical rebounds, but the underlying situation remains fragile. Investors are hoping for some positive signals from US payrolls, ISM manufacturing and Eurozone inflation data.

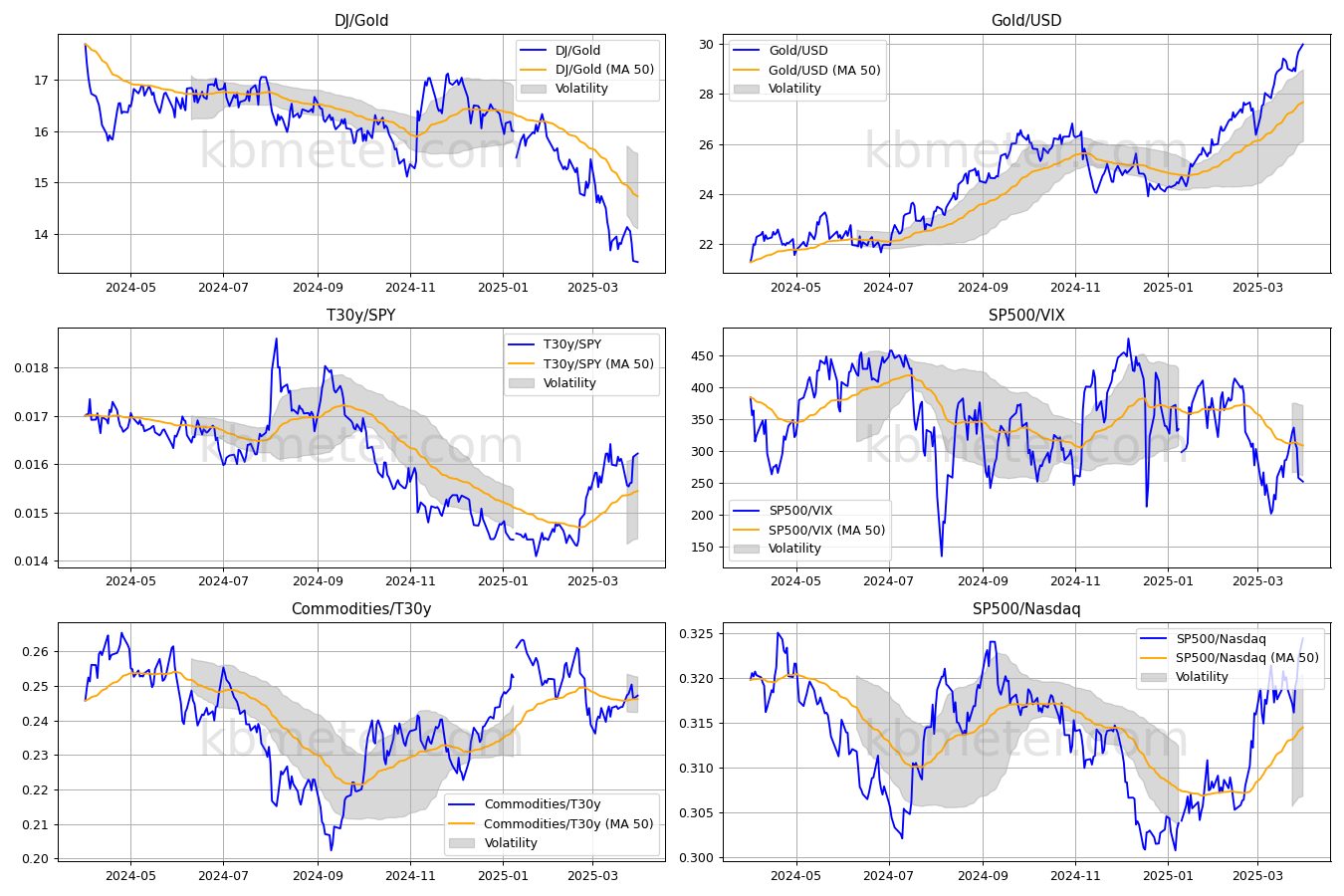

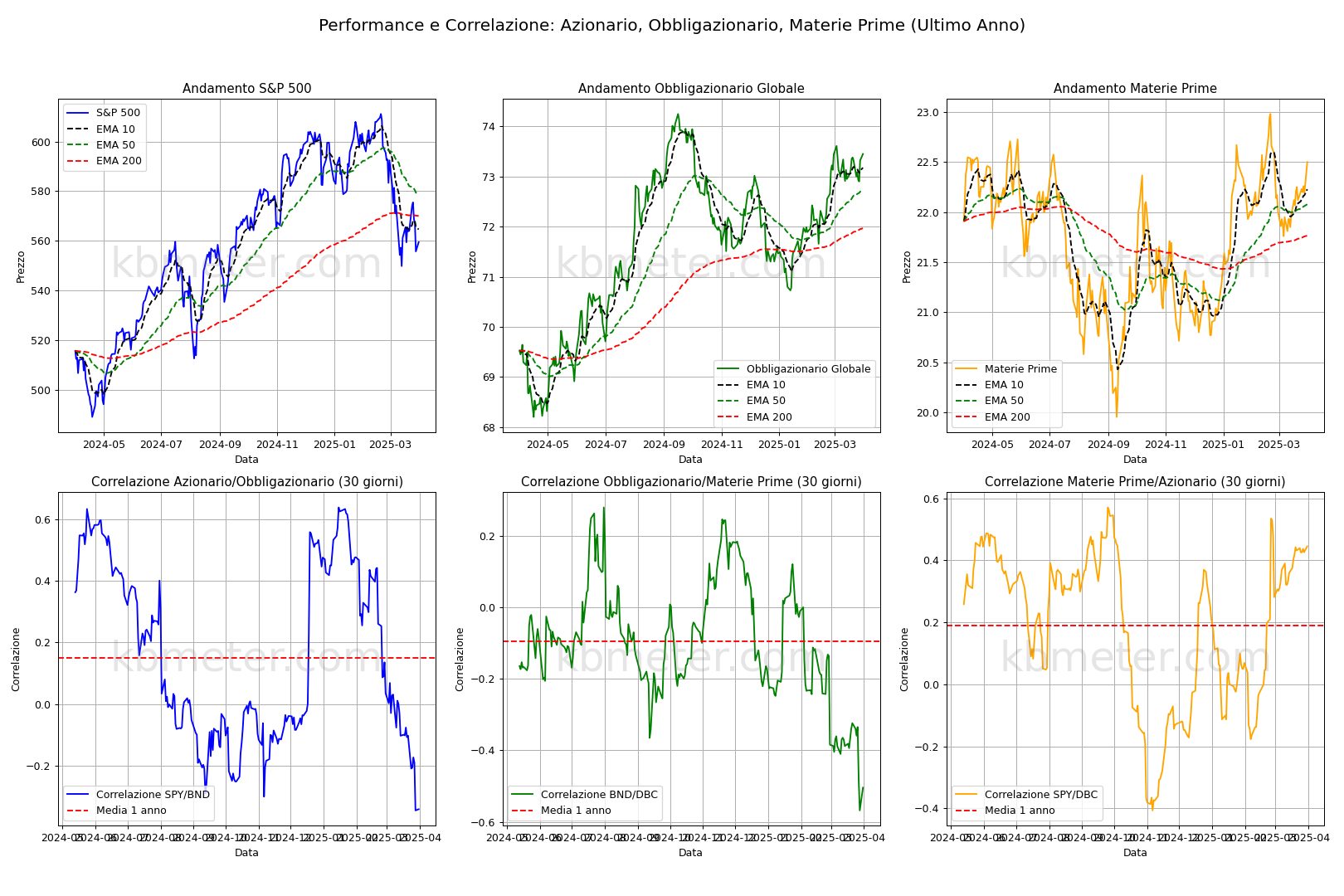

Our intermarket dashboards continue to indicate a risk-averse scenario. The recovery in the second half of yesterday’s session by the US equity indices seems to have more technical reasons than anything else, given that it was still the close of the first quarter of 2025. We continue to monitor the trend in commodities, the movement of which is currently very much linked to gold prices. For the S&P500, the situation remains stable at the moment, with the index remaining below the 200-day average and the 50-day average remaining below the 200-day average.

On the macroeconomic front, final data from the March PMI surveys, the US ISM manufacturing index, February US jobless claims and March Eurozone inflation are awaited. Meanwhile, Australia’s central bank left rates unchanged, underlining the high uncertainty in the international scenario.

Our forecast analysis indicates another difficult day for equities, with more negative signals in Europe. On the bond front, a wait-and-see situation, with US yields seen little movement and still positive signals on corporate. Among commodities, gold continues to report positive momentum; positive signals also for natural gas and oil. Volatility seen rising slightly further.

Already a subscriber? Login here

NOTES AND WARNINGS

Data compiled by kbmeter.com. Analysis date: 1 April 2025 - 7:25 AM GMT+1

This content is provided for informational purposes only and should not be considered financial advice. All scores and assessments are based on the previous trading day’s closing prices. Futures indications refer to the date and time of the analysis.